{kind=link}

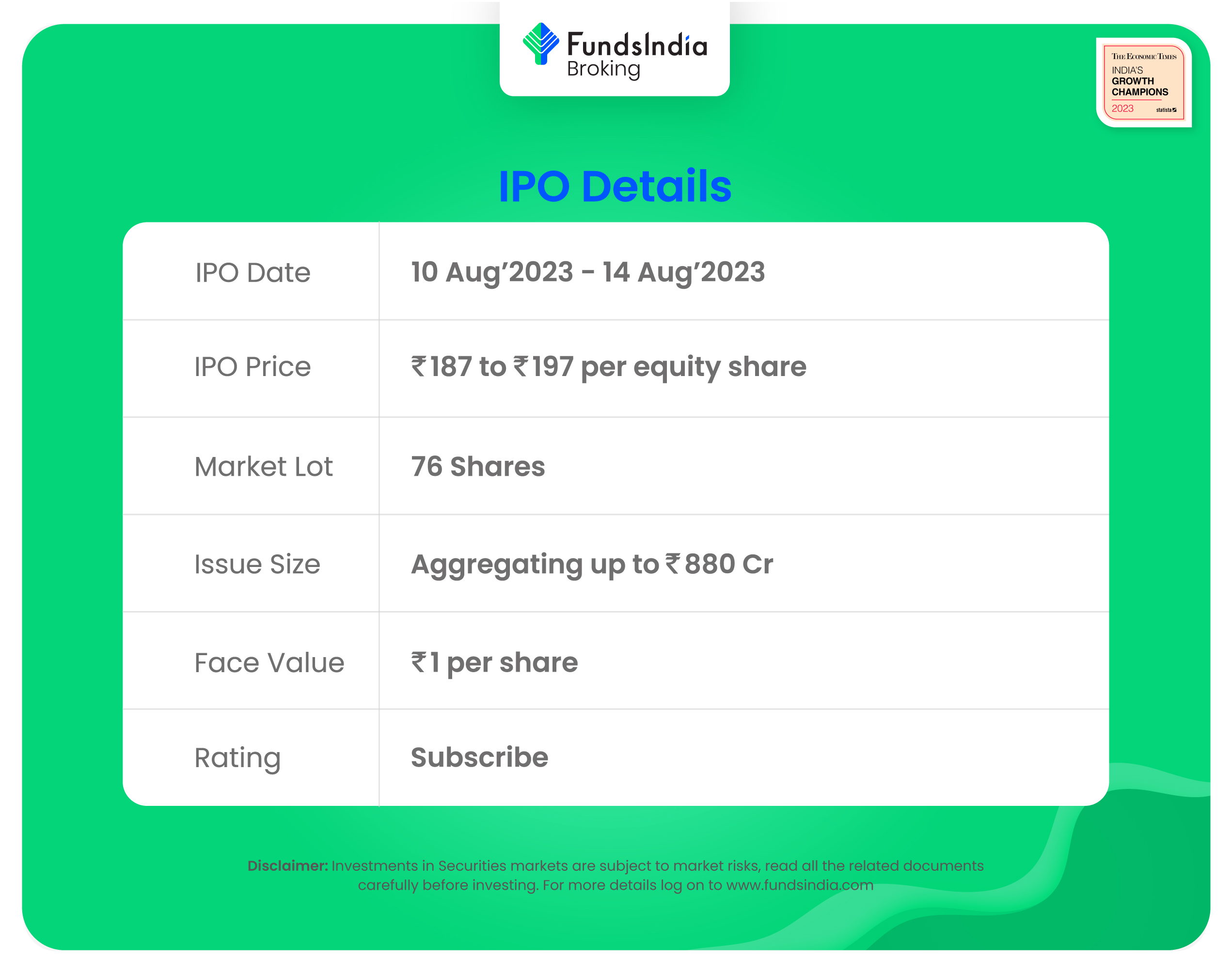

Firm Overview:

TVS Provide Chain Options Restricted (TSCSL) stands as India’s largest and one of many quickest increasing built-in suppliers of provide chain options among the many listed Indian corporations on this sector, each by way of income and income progress. The Firm is an India-based multinational firm that pioneered the event of the availability chain options market in India in line with Redseer Report. It’s promoted by the erstwhile TVS Group, one of many reputed enterprise teams in India (Supply: Redseer Report), and is now a part of the TVS Mobility Group. TSCSL’s options spanning the complete worth chain from sourcing to consumption could be divided into two segments: (i) built-in provide chain options (“ISCS”); and (ii) community options (“NS”). Its capabilities underneath the ISCS phase embrace sourcing and procurement, built-in transportation, logistics operation centres, in-plant logistics operations, completed items, aftermarket fulfilment and provide chain consulting. Whereas its capabilities underneath the NS phase embrace international forwarding options (“GFS”), which includes managing end-to-end freight forwarding and distribution throughout ocean, air and land, warehousing and at port storage and value-added companies.

Objects of the Supply:

- Prepayment or compensation of all or a portion of sure excellent borrowings availed by the corporate and its subsidiary, TVS LI UK.

- Basic company functions.

Funding Rationale:

- Asset Mild Mannequin: The corporate operates an asset-light enterprise whereby the warehouses (primarily comprising aftermarket warehouses, devoted shopper product and retail warehouses, multi-client amenities and nationwide distribution centres) and automobiles are operated by leases with their community companions. Whereas the corporate don’t have possession of those belongings, they’ve management over the capability and fleet, and the scheduling, routing, storing, and supply of products are managed by them. Furthermore, TVS provide chain additionally handle buyer owned/leased warehouses. Their warehousing enlargement technique includes leasing multi-user amenities in manufacturing and consumption centres in India with applicable infrastructure and know-how enablement that permits them to serve their current prospects and develop their enterprise by encirclement and new buyer acquisition.

- Shopper Base: Globally, the corporate supplied provide chain options to 11,546, 10,531 and eight,788 prospects throughout Fiscals 2021, 2022 and 2023, whereas in India, the corporate supplied options to 1,120, 1,044 and 902 prospects in the identical intervals. It has added an mixture of 1,179, 152 and 177 new prospects in Fiscals 2021, 2022 and 2023, respectively. Its prospects span throughout quite a few industries similar to automotive, industrial, shopper, tech and tech infra, rail and utilities, and healthcare. It has developed long-term relationships with numerous purchasers, which has supplied resilience to its income and profitability. A few of its prospects with whom it had long-term relationships as of FY23, embrace Sony India Non-public Restricted (12 years), Hyundai Motor India Restricted (13 years), Ashok Leyland Restricted (17 years), TVS Motor Firm Restricted (17 years), Diebold Nixdorf (8 years), VARTA Microbattery Pte Ltd (7 years), Hero MotoCorp Restricted (8 years), Torrot Electrical Europa, S.A. (3 years), and so on.

- Monetary Observe Report: The corporate’s income has grown at a CAGR of 16% from Rs.6605 crore in FY20 to Rs.10235 crore in FY23, whereas the web revenue has proven regular progress by lowering the losses and making revenue. Although backside line has a loss-making historical past, EBITDA of the corporate has grown at a CAGR of 39% from Rs.255 crore in FY20 to Rs.684 crore in FY23. Finish person Business sensible, Industrials accounts for 35% of the FY23 income, adopted by Automotive with 23%, Tech & Tech infra with 12%, Client with 12%, Rail and Utilities with 6%, Healthcare with 2% and others with 10%. Geographically, India accounts for 30% of the FY23 income, adopted by UK with 30%, EU with 13%, Australia and New Zealand with 8%, North America with 7% and others with 12%.

Key Dangers:

- Foreign exchange Threat – The corporate is uncovered to international trade dangers, as main portion of its revenues are generated in foreign exchange. Fluctuations in trade charges may have an effect on its monetary efficiency.

- OFS – The IPO is a mixture of provide on the market (OFS) and Contemporary subject with OFS being 32% of the general subject measurement. Within the provide on the market (OFS), Investor promoting shareholders named Omega TC Holdings Pte. Ltd, Tata Capital Monetary Companies Restricted, TVS Motor Firm Restricted and Kotak Particular Conditions Fund will offload as much as 1,19,19,388 fairness shares. Different promoting shareholders will offload as much as 22,93,810 fairness shares.

Outlook:

The corporate has a robust presence within the quickly increasing and fragmented third-party logistics market in India. It additionally has a robust parentage with the administration group with numerous trade expertise. Based on RHP, the listed peer group of the corporate are TCI Categorical Ltd, Mahindra Logistics Ltd, Blue Dart Categorical Ltd, Delhivery Ltd, and so on. On the increased value band, the itemizing market cap will likely be round ~Rs.8615 crs and the corporate is demanding a P/E a number of of 205x based mostly on publish subject diluted FY23 EPS. Since, the corporate has began making revenue in FY23 it isn’t truthful to worth the corporate based mostly on the P/E. So, we took EV/EBITDA ratio for comparability and the corporate’s Enterprise worth based mostly on the itemizing market cap, closing (FY23) debt and shutting (FY23) money is round Rs.9520 crs which is ensuing an EV/EBITDA of ~14x. The friends are buying and selling at a median EV/EBITDA a number of of 19x (excluding Delhivery which is making an working loss). When in comparison with its friends, the problem seems between undervalued to pretty valued class. Primarily based on the above views, we offer a ‘Subscribe’ score for this IPO for a medium to long-term Holding.

If you’re new to FundsIndia, open your FREE funding account with us and revel in lifelong research-backed funding steering.

Different articles it’s possible you’ll like

Put up Views:

4,510