{kind=link}

“Don’t put all of your eggs in a single basket” is likely one of the easiest methods to elucidate the idea of diversification.

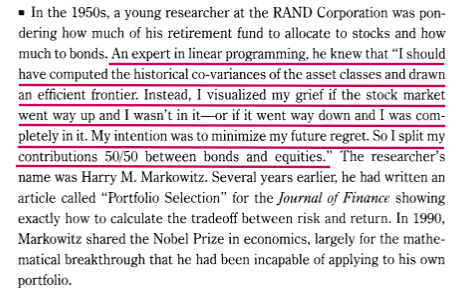

Whereas the above assertion places throughout the purpose very fantastically, in Nineteen Fifties an individual by the title of Harry Markowitz went on to construct a mathematical mannequin. He even submitted a paper on his analysis to the Journal of Finance. Lastly, he went on to share the Nobel Prize in Economics in 1990.

On account of his effort emerged the Imply-Variance Evaluation, which grew to become the bedrock of the Fashionable Portfolio Concept. Through the years, the vast majority of the funding administration chaps use the mannequin to pick out and construct portfolios for his or her purchasers.

What Harry Markowitz put throughout was this:

- There are completely different funding securities with low correlation to one another. They show completely different behaviour at completely different occasions by way of outcomes or efficiency as additionally the timing of such returns.

- One can use the previous information on danger and returns and the long run anticipated returns together with consumer preferences to construct an optimised and environment friendly portfolio that delivers the utmost attainable returns on the minimal attainable danger.

The straightforward postulation of the paper was that diversification is sweet and could be and ought to be completed scientifically. Here’s a technique to do it.

However did the knowledgeable apply the identical rule to his portfolio?

Apparently not!

When the time got here to use the principles to himself, Markowitz chickened out.

Right here’s an excerpt from Jason Zweig’s, a well-known monetary journalist, e-book Your Cash and Your Brains.

The founding father of the Fashionable Portfolio Concept himself went for an equal weightage allocation.

Why did that occur? Whey couldn’t he apply the identical guidelines to himself for which he even went on to win a Nobel Prize?

Easy trumps Complicated.

The mathematical mannequin that received the Nobel Prize was simply too advanced. It calls for inputs of previous information (for a number of years) about danger (or variance) and returns as additionally anticipated future returns which may then be plotted in a number of combos to determine which of the combos of varied belongings are seemingly to offer probably the most optimum outcomes.

Phew!

The issue begins with the info and it compounds with the truth that the previous can by no means be equal to the current or the long run.

This makes the mannequin impractical.

Our thoughts fails to just accept this complexity.

What we observe and like to observe is the easy. Complicated freezes us whereas easy triggers motion.

Therefore, Markowitz took the easy method for his personal portfolio. A 50:50 allocation to equities and bond, periodically rebalanced.

Is that this excellent? No.

Is that this straightforward to grasp, implement and monitor? Sure.

At any given level in time, easy will all the time trump advanced in your thoughts.

Isn’t that true?

The consultants don’t have all of the solutions. Even when they are saying there may be a solution, it might not be sensible.

Discover what works for you and implement it.