{kind=link}

Firm Overview:

Honasa Shopper Restricted is a digital-first home of manufacturers catering to the varied wants of millennial prospects. The corporate is constructing a brand new technology of magnificence and private care manufacturers – pushed by goal, powered by expertise, and targeted on evolving shopper wants. From pure private care to science-backed skincare and a contemporary tackle Ayurveda, every of their manufacturers has a singular proposition, created for millennials. Honasa Shopper’s in-house portfolio of manufacturers includes family favorites like Mamaearth, The Derma Co., Aqualogica and Ayuga. They’ve additionally made strategic acquisitions to strengthen firm portfolio – BBlunt (Services), Dr Sheth’s (dermatologist formulated skincare model).

Objects of the Provide:

- Commercial bills in direction of enhancing the notice and visibility of manufacturers;

- Capital expenditure to be incurred by Firm for organising new EBOs.

- Funding in Subsidiary, Bhabani Blunt Hairdressing Non-public Restricted (“BBlunt”) for organising new salons.

- Basic company functions.

Funding Rationale:

- Expertise and information capabilities: Honasa Shopper Since launching Mamaearth in 2016, the model, Mamaearth, is constructed to service a core buyer want for safe-to-use, pure merchandise, and focuses on growing toxin-free magnificence merchandise made with pure substances. Honasa Shopper Restricted intend to proceed to spend money on expertise and information capabilities to drive enterprise efficiencies, keep related with shoppers and strengthen cross-brand, cross-functional synergies. The corporate intends to additional refine personalization engine to ship a extra tailor-made, contextualized expertise to customers, deepen model join and drive shopper retention and repeat. In June 2022, the corporate launched an built-in sampling platform, YOTO Field, to allow them to generate trials throughout manufacturers in portfolio and drive cross-selling, with the intention of capturing a better share of pockets and buyer lifetime worth at an organization stage sooner or later.

- Sturdy skilled administration: Group is led by visionary founders, Varun Alagh (CEO) and Ghazal Alagh (CIO). Previous to founding Firm, Varun labored throughout marquee firms in India akin to Hindustan Unilever, Diageo India Non-public Restricted and Coca-Cola India Non-public Restricted. Ghazal labored with NIIT and operated dietexpert.in, an impartial industrial operation. Ghazal has been related to Firm as a promoter and director since September 16, 2016. Collectively, their information and understanding of the consumer-packaged items and BPC merchandise house in India has been instrumental in growing and rising enterprise.

- Monetary Monitor Report: The corporate reported a income of Rs. 1493 crore in FY23 as in opposition to Rs. 943 crores in FY22. The income has grown at a CAGR of 80.14% between Monetary Years 2021 and 2023. The EBITDA of the corporate in FY23 is at Rs. 23 crore and EBITDA margin is at 1.52%. The corporate has posted a web lack of (- Rs. 151 crores) in FY23. For Q1FY24, it earned a web revenue of Rs. 24.72 crores, on a income of Rs. 464 crores.

Key Dangers:

- Depending on Third Celebration – Firm outsources the manufacturing of all of the merchandise to third-party producers, primarily below non-exclusive contract manufacturing preparations, and doesn’t personal any manufacturing services. The corporate’s dependence on third-party producers for all of the merchandise topics it to dangers, which, if realized, may adversely have an effect on the enterprise, outcomes of operations, money flows and monetary situation. Depending on a number of third-party service suppliers to promote or distribute its merchandise to shoppers, and on third occasion expertise suppliers for sure elements of its operations. Any disruptions or inefficiencies in these operations might adversely have an effect on the enterprise, monetary situation, money flows, and outcomes of operations.

- OFS – The IPO will see the sale of three,186,300 shares by Honasa promoter Varun Alagh and as much as 100,000 shares by his spouse Ghazal Alagh. Plenty of different shareholders, together with Kunal Bahl 1,193,250 shares, Shilpa Shetty Kundra 1,393,200 shares, Rishabh Harsh Mariwala 5,700,188 shares, Fireplace Ventures Fund 7,972,478 shares, Sofina 9,566,974 shares, Stellaris 10,942,522 shares, and Rohit Kumar Bansal 1,193,250 shares, will likely be promoting their stakes within the OFS.

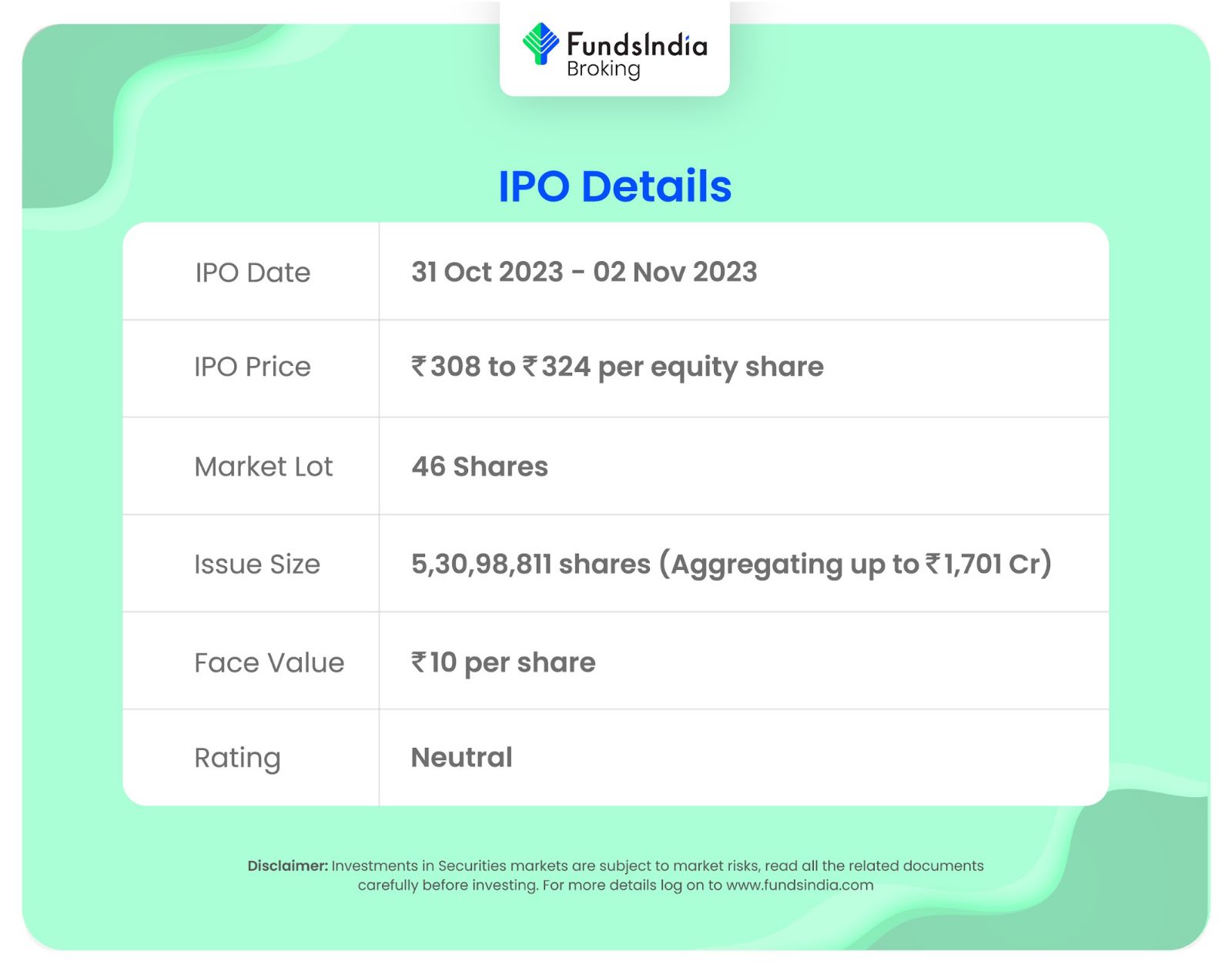

Outlook:

Honasa Shopper Restricted is the most important digital-first magnificence and private care (“BPC”) firm in India when it comes to income from operations for the Monetary 12 months 2023. In response to RHP, the corporate’s listed friends are Hindustan Unilever Restricted, Colgate Palmolive (India) Restricted, Procter & Gamble Hygiene and Well being Care Restricted, Dabur India Restricted, Marico Restricted, Godrej Shopper Merchandise Restricted, Emami Restricted, Bajaj Shopper Care Restricted and Gillette India Restricted. The friends are buying and selling at a mean P/E of 54x with the best P/E of 83x and the bottom being 26x. On the increased worth band, the itemizing market cap of Honasa Shopper will likely be round ~Rs.10425 crore. The corporate is attempting to be worthwhile (Traditionally it has extra loss-making quarters) it’s not efficient to match with the above friends as of now. We must always watch for few extra quarters to see whether or not the corporate begins making stability in profitability. Based mostly on the above views, we offer a ‘Impartial‘ ranking for this IPO for a medium to long-term Holding.

If you’re new to FundsIndia, open your FREE funding account with us and revel in lifelong research-backed funding steering.

Different articles you could like

Submit Views:

113