{kind=link}

In 2018, revenues for the net gross sales web site, Craigslist, peaked at $1.03 billion after which started a fast descent. It’s nonetheless a viable firm (2022 revenues had been $694m) however it suffers from a case of channel calcification. Craigslist hasn’t modified a lot of its performance because it began, and customers discover that different choices supply a significantly better expertise.

On October 4, 2016 (observe the timing), Fb Market hit the scene. Although Fb itself is in decline, its offshoots similar to Market and Instagram are thriving. Market is maybe Craigslist’s most related competitor because it permits customers to go looking and purchase domestically with ease. eBay, one other competitor, does much less native enterprise, however eBay sellers profit from built-in delivery choices that make it simpler for patrons and sellers. And most not too long ago is Etsy, the place sellers can supply high-quality, artisanal merchandise and developed an incredible loyal buyer base with an estimated 40% are gross sales from repeat patrons. I do know I’ve purchased from all of those relying on what I’m on the lookout for – I’m a multi-channel purchaser.

Fb Market has some clear benefits over Craigslist, most having to do with the client expertise. First, there’s safety. Consumers and sellers can see one another and work together much more simply, eradicating among the buy’s uncertainty. They will touch upon one another on the platform, which makes each events liable for finishing a great and honest transaction. The vendor dashboard is straightforward to make use of. Cost will be made by means of the platform if each events conform to it with a number of totally different cost choices. Sellers can even pay a premium to get “pushed” to the highest of the listings.

So, the Craigslist downturn has two elements to it: Lack of buyer expertise enhancements and lack of vendor desire. If sellers discover that they’re promoting extra by means of a greater channel, they’ll transfer. Consumers will then transfer with them as a result of the choice improves by means of the brand new channel.

There are a dozen classes on this state of affairs for insurers, however let’s look carefully at 5.

Lesson 1: Channels aren’t fastened. They’re fluid.

Most insurers grasp that they should create an ecosystem of interconnected channels, utilizing a variety of capabilities that can join with prospects when and the way they need to purchase. Channel improvement and use is a balancing act. Channel effectiveness is at all times in movement. Insurers have to ask themselves, “Are we treating our channels as if they’re fastened in time or are we getting ready to make use of right now’s trending channels right now and tomorrow’s trending channels tomorrow.” Not solely are channels not fastened in place, however an insurer’s channel technique must be constructed to circulation with channel tendencies. The best way to maintain up with buyer demand is to turn into adept at broad distribution strategies and nice experiences. That is the place tech is available in. A lot of Majesco prospects are re-creating their digital distribution setting utilizing our distribution administration options and ecosystem of companions.

In a press launch asserting our expanded capabilities, Karlyn Carnahan, head of Celent’s North American Insurance coverage observe acknowledged, “If a service desires to completely exploit the potential of its numerous channels, they have to suppose very otherwise about distribution administration, compensation, and segmentation. Distribution administration platforms should proceed to evolve to allow insurers to handle their distribution pressure with rising sophistication.”

Lesson 2: It’s essential for insurers to know trending channel preferences.

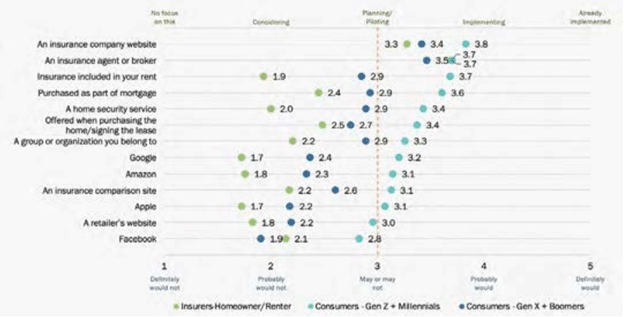

In Majesco’s current thought-leadership report, Bridging the Buyer Expectation Hole: Property Insurance coverage, we glance carefully at buyer buy channel preferences weighed in opposition to insurance coverage for channel improvement. Do they match up? After we visualize the information, the gaps are straightforward to see.

Conventional channels stay the popular technique for buying house owner/renter insurance coverage, together with brokers/brokers and firm web sites, as mirrored in Determine 1. Nevertheless, for all the opposite channels, prospects’ curiosity is almost twice that of insurers’ actions, significantly for the Gen Z and Millennial section.

Determine 1: Buyer-Insurer gaps in distribution channels for private property insurance coverage.

The youthful technology displays the need for entry by means of and all channels. Members of this technology are heavy renters, and they’re starting their transition to homeownership. Insurers who’re providing ease of entry to renters’ insurance coverage have the chance to construct robust buyer relationships that can generate larger income. The digital expectations and ease of entry are prime priorities for this technology.

Insurers that need to seize extra enterprise by means of a broad-channel method will take note of the bigger gaps and tendencies as they search for alternatives. Nevertheless, they may even need to take note of these areas the place insurers appear to be getting nearer, however maybe their firm remains to be within the consideration part. It is a signal that opponents could also be beating them to profitable partnerships. For instance, there’s a lessening hole for the channels, buying property insurance coverage on the level of a house buy or bought as part of a mortgage. These partnerships could also be rising in frequency.

Lesson 3: Life and enterprise occur on the level of buy and vice versa.

Fb Market had one distinct benefit over Craigslist proper from the outset — it was positioned the place individuals had been interacting, even after they weren’t searching for something. When Majesco survey information, it’s clear that SMB industrial property insurance coverage purchases can even occur practically anyplace there’s interplay or engagement. Insurers must be asking themselves, “The place can’t we promote?”

Each generational SMB segments are desirous about all channels as proven in Determine 2. Nevertheless, insurers should not assembly these expectations, except for brokers/brokers, and to some extent, firm web sites. The gaps are important – as much as 2 occasions what insurers do – significantly for the youthful technology of Gen Z and Millennials, according to their expectations for a multi-channel world.

These gaps restrict insurers’ attain and development whereas placing them in a aggressive gap as in comparison with others which might be utilizing a multi-channel technique. Whereas brokers will proceed to be vital, easy accessibility to insurance coverage through different channels, significantly for embedded insurance coverage, can be more and more vital for future viability.

Determine 2: Buyer-insurer gaps in distribution channels for industrial property insurance coverage.

For instance, in Determine 2, take a look at the hole between Gen Z/Millennial SMB’s curiosity inpurchasing property insurance coverage by means of their payroll service and insurers’ curiosity in offering property insurance coverage by means of the payroll channel.

For an SMB proprietor, there’s virtually no enterprise accomplice that’s consulted extra persistently than the payroll firm. Payroll contact occurs weekly or bi-weekly. Industrial property insurers would do nicely to accomplice with payroll firms. It’s a win/win. It makes a wonderful instance of the standards insurers ought to think about when they’re eager to broaden their distribution. Search for locations the place life and enterprise occur and people are the factors the place publicity will be fruitful. Payroll is a degree of buy.

Insurers can search for spots the place life and enterprise are occurring, even when there will not be a particular buy concerned. Examples of those can be commerce associations, neighborhood enterprise associations, authorized companies, upkeep suppliers, or safety companies. Definitely, one of many best relationship synergies must be between property insurers and property safety firms, but this distribution channel additionally has one of many largest gaps.

Lesson #4: Don’t suppose you may wait till tomorrow for channel growth.

The time is now for fast multi-channel growth, enabled by applied sciences that may deal with the rising tempo of change. Some channels could not pan out. Some channels will pull their weight. Some can be profitable. Like investing in mutual funds as an alternative of particular person shares, insurance coverage expertise investments want to permit for a broad method to distribution.

Change is quicker, deeper, wider, and extra highly effective than we’ve ever been used to earlier than. The end result? Rising buyer expectation gaps, significantly for the youthful technology who at the moment are the dominant patrons put insurers prone to dropping loyalty and stifling development.

Ahead-thinking leaders are making daring, warp-speed strikes to shut buyer expectation gaps and place themselves for market management and development. They’re specializing in prolonged market and buyer attain for individuals and companies by means of new distribution channel choices, together with embedded insurance coverage. These choices meet individuals the place they’re right now, not the place they are going to be subsequent yr.

For insurers, adopting a brand new distribution channel philosophy will give them a stronger, extra aggressive market place by means of a rising channel ecosystem that performs to their strengths and closes gaps or weaknesses.

Lesson #5: It isn’t sufficient to offer a brand new channel. It’s best to lend one thing new and improved to the expertise.

Partnerships and trendy distribution expertise are two items of the identical puzzle. In right now’s insurance coverage, you may’t have one with out the opposite. Trendy distribution administration isn’t nearly connections — it’s about utilizing information, channel expertise, and channel efficiency to tweak, flex, and generate gross sales. Good digital experiences occur when the appropriate applied sciences are used creatively.

Majesco’s Distribution Administration and Digital360[DG1] options assist insurers fast-forward their channel growth plans, whereas immediately giving them the cutting-edge AI and machine studying instruments to adapt and develop. Insurers ought to ask themselves questions like, “Can we use our information to anticipate subsequent steps or anticipate extra wants? Is our distribution administration feeding us insights that can assist us shift in a well timed method?”

Staying on the entrance of the aggressive pack takes an open angle and a willingness to repeatedly adapt. “The place can’t we promote?” The reply is, “Solely the place we aren’t ready to.”

It might be exhausting to consider, however Craigslist was as soon as “cutting-edge” and disruptive. It actually shares among the credit score for hastening the demise of some each day print newspapers. But, plainly it was by no means Craigslist’s aim to turn into far more than it already was.

Insurers should be totally different. Leaders that want to stay on prime of the competitors will hold distribution expertise on the forefront of their priorities. They may even return often to their distribution technique and assess its alignment with particular person and enterprise buyer channel tendencies.

For a better take a look at how some insurers are aligning themselves to P&C prospects, make sure to learn Majesco’s thought-leadership report, Bridging the Buyer Expectation Hole: Property Insurance coverage. For extra data on how right now’s tech can assist to increase your organization’s distribution channels, contact Majesco right now.

[DG1]hyperlink