{kind=link}

The energy of shopper spending up to now this yr has shocked most personal forecasters. On this put up, we study the components behind this energy and the implications for consumption within the coming quarters. First, we revisit the measurement of “extra financial savings” that households have gathered since 2020, discovering that the estimates of remaining extra financial savings are very delicate to assumptions about measurement, estimation interval, and pattern kind, which renders them much less helpful. We thus broaden the dialogue to different elements of the family stability sheet. Utilizing knowledge from the New York Fed’s Shopper Credit score Panel, we calculate the extra money flows made obtainable for consumption because of households’ changes to their debt holdings. To detect indicators of stress in family monetary positions, we study current developments in delinquencies and discover the proof to be combined, suggesting that sure stresses have emerged for some households. In distinction, we discover that the New York Fed’s Survey of Shopper Expectations nonetheless factors to a strong outlook for shopper spending.

Stunning Consumption Power

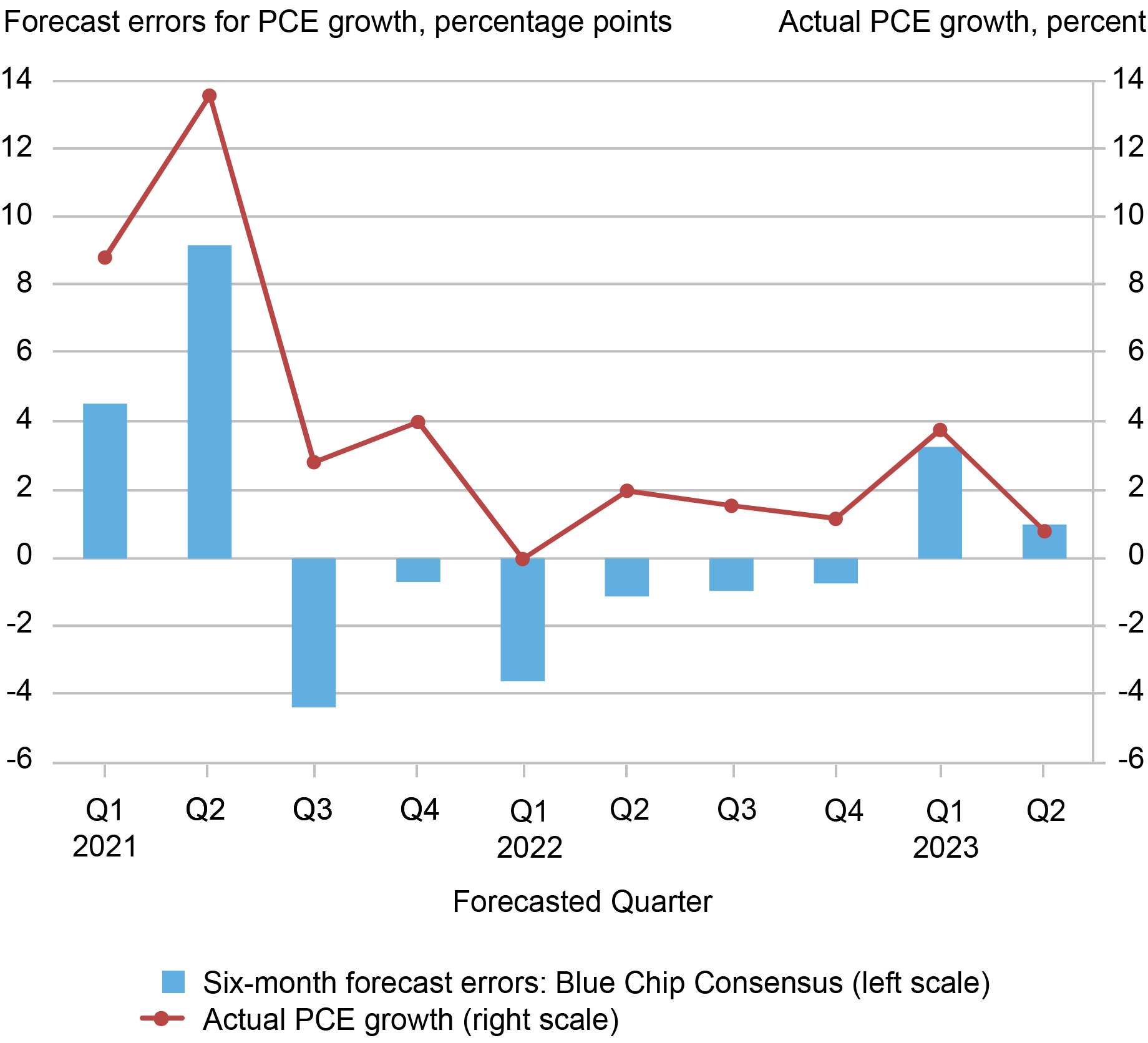

Actual private consumption expenditures (PCE) have been remarkably sturdy for the reason that onset of the pandemic, to the shock of many analysts over a lot of this era. The surprises have been particularly notable over the primary half of this yr, as actual PCE development has held up within the face of ongoing financial coverage tightening and this spring’s banking system stress.

To quantify the extent of those surprises, we chart errors within the six-month-ahead Blue Chip Consensus forecasts of quarterly actual PCE development (measured at an annual price). A constructive forecast error (proven within the blue bars) at time t signifies that the realized development price (proven in crimson) was above the forecasts from six months earlier.

Consumption Has Shocked to the Upside, Particularly in 2023

Sources: Bureau of Financial Evaluation; Blue Chip Financial Indicators.

Notes: The crimson line exhibits the true (inflation-adjusted) quarterly annualized price of development for private consumption expenditures (PCE). The blue bars present the distinction between realized PCE development and the six-month-ahead Blue Chip Consensus forecasts, with constructive values indicating that consumption development was larger than anticipated.

Within the first half of 2021, actual PCE grew a lot sooner than predicted, seemingly as a result of an unexpectedly quick rollout of vaccines and a larger-than-expected fiscal stimulus–when it comes to each magnitude and multiplier impact on consumption. All through 2022, nonetheless, consumption was weaker than forecasted, most likely as a result of a mix of higher-than-expected inflation, a bigger impact on disposable earnings from the unwinding of pandemic-related fiscal assist, and a faster-than-expected tightening of monetary circumstances.

However in 2023, we’ve seen upside surprises as soon as once more, notably for the primary quarter. Furthermore, the latest Blue Chip Consensus forecast for consumption development in 2023:Q3 is larger than what was anticipated six months in the past. This shift has occurred as a result of many forecasters up to now few months have deserted their projections of recession and destructive consumption development. We now try to know these forecast errors.

Extra Financial savings

We start our dialogue with extra financial savings, which has obtained lots of consideration from economists and the enterprise press. The concept is that enormous fiscal transfers and diminished consumption alternatives through the pandemic led households to avoid wasting greater than they in any other case would have performed and now these financial savings could also be obtainable to assist consumption. There’s super uncertainty, nonetheless, about how a lot extra financial savings nonetheless stay within the family sector.

Whereas analysts usually agree that extra financial savings reached excessive ranges over the course of 2021, vital variations about their current stage have developed; for instance, see Aladangady et al., de Soyres et al., and Abdelrahman and Oliveira (Higgins and Klitgaard research extra financial savings within the worldwide context). The variations in estimates for the US are attributable to technical components just like the assumed pre-pandemic pattern, and totally different views about whether or not the financial savings price or gross family saving (in {dollars}) is the suitable approach to consider any extra.

As we transfer additional past the pandemic, measuring extra financial savings turns into more and more fraught, because it depends closely on assumptions about habits within the absence of the pandemic. Consequently, in excited about the current resilience of consumption and the implications for the longer term, a broader evaluation of households’ monetary positions now appears a extra vital consideration than extra financial savings in isolation. Within the the rest of the put up, we concentrate on an vital factor of such an evaluation: the position of debt in supporting households’ capability to maintain consumption.

Family Debt

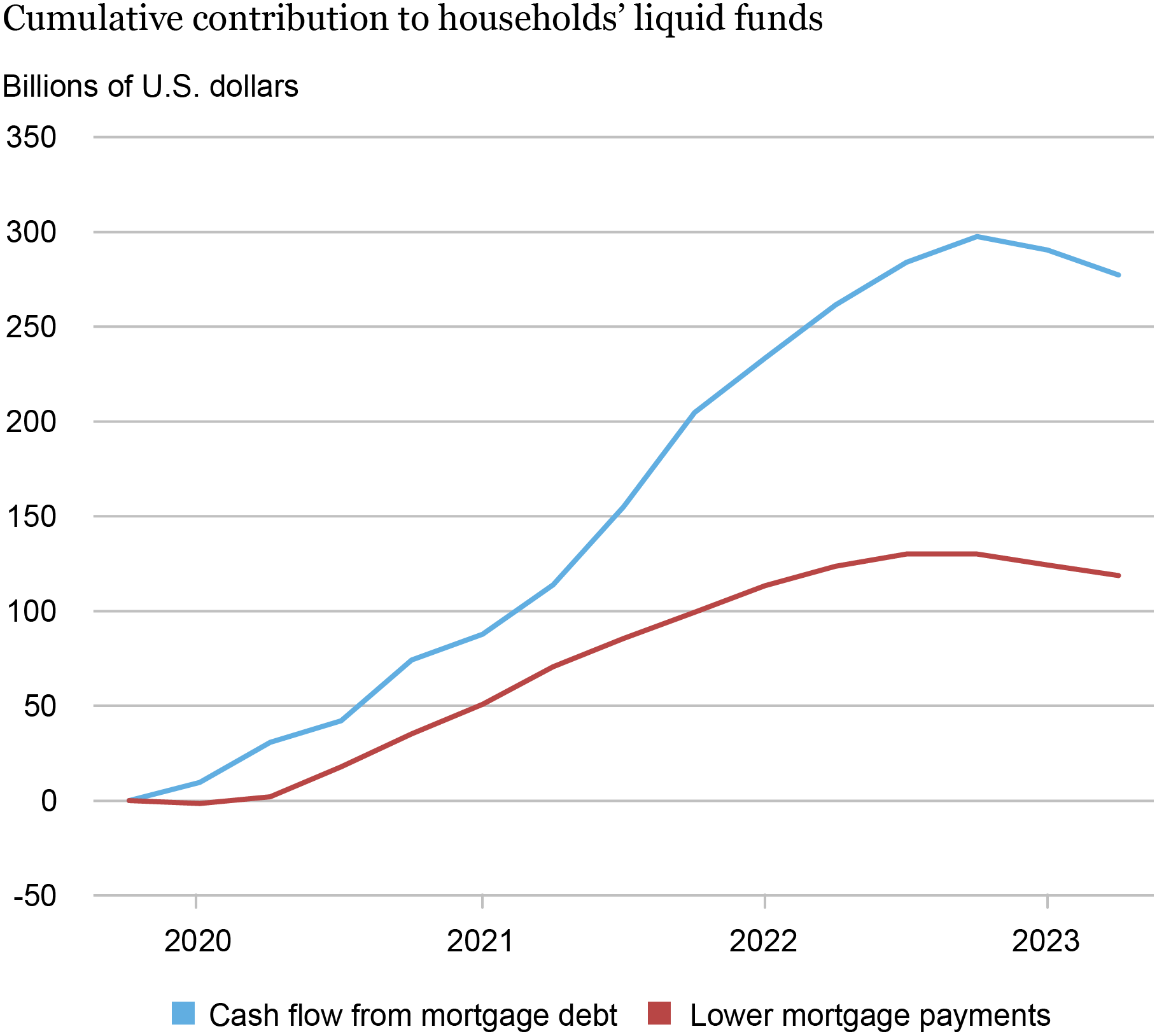

Along with financial savings, households have comparatively illiquid property (like housing) and liabilities (like mortgages and bank card money owed) on their stability sheets. The pandemic interval featured forbearances on a number of forms of debt, together with giant fiscal transfers and really low rates of interest, resulting in vital enhancements in family money flows. For instance, about 14 million households refinanced their mortgages, decreasing their mortgage invoice by $30 billion per yr by 2021. The crimson line within the subsequent chart exhibits that the cumulative financial savings from these decrease funds stood at about $120 billion as of 2023:Q2, with current quarters bringing declines as newer mortgages carry larger balances and better rates of interest.

Along with these financial savings, owners withdrew unusually giant quantities of dwelling fairness, primarily within the type of cash-out refinances through the interval of low charges. These funds, proven within the blue line under, are additionally obtainable for consumption and quantity to $280 billion in 2023:Q2.

Fairness Extraction and Mortgage Refinances Contributed to Liquid Funds Accessible for Consumption

Supply: New York Fed Shopper Credit score Panel / Equifax

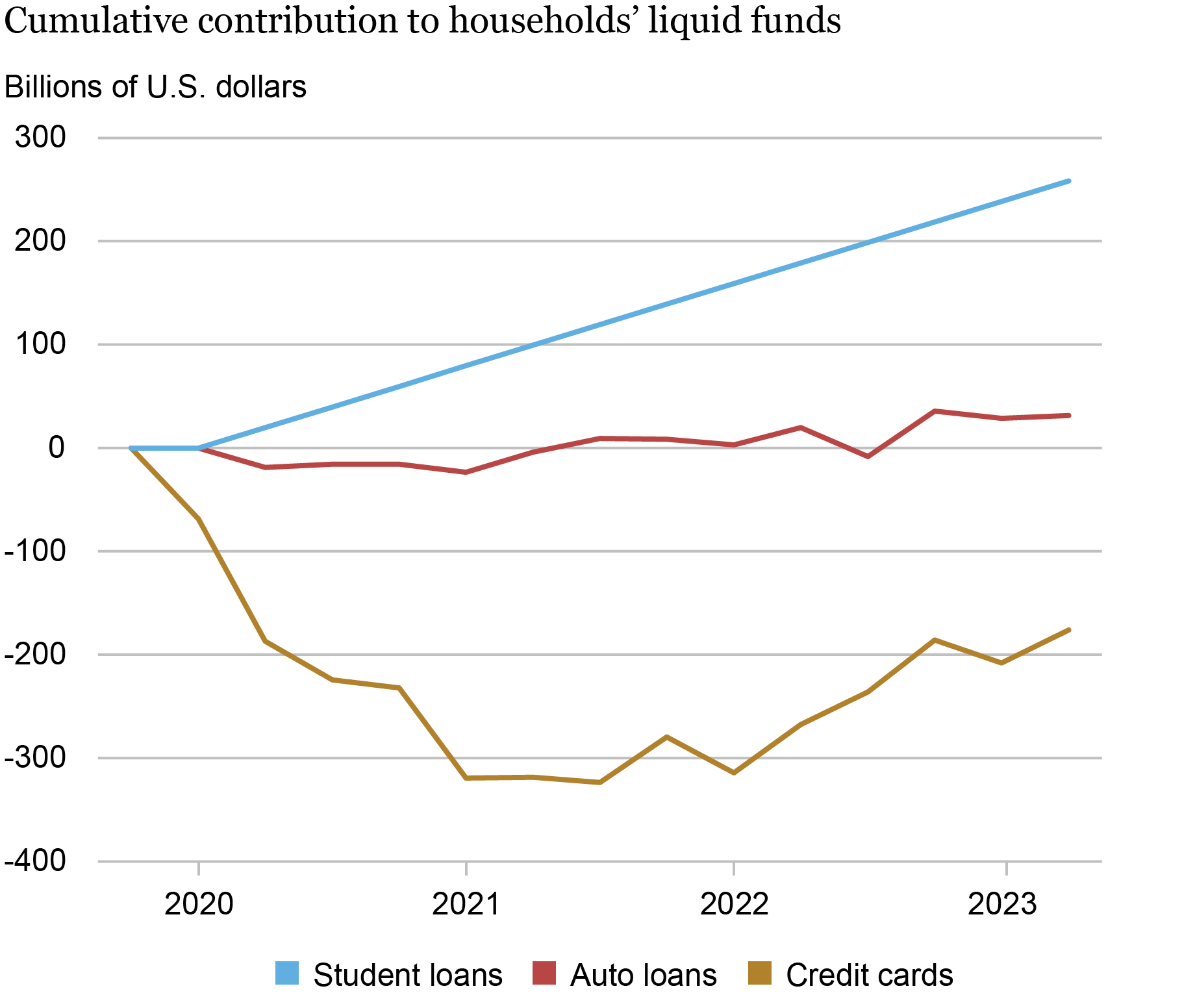

Different types of family debt additionally supported consumption. Funds on scholar debt, which competes with auto loans to be the second largest family sector legal responsibility, have largely been in forbearance for the reason that early levels of the pandemic. Funds on federal scholar loans previous to the cost moratorium totaled about $70 billion per yr, which means that by 2023:Q2 about $260 billion was left within the family sector; see the blue line in our subsequent chart. By comparability, auto loans (crimson line) have made comparatively small contributions to the funds obtainable for consumption, whereas a few of the funds that households saved have been mirrored in diminished bank card balances (gold line).

Credit score Card Paydowns Offset Scholar Mortgage Forbearance

Supply: New York Fed Shopper Credit score Panel / Equifax.

In whole, mortgages—by fairness extraction and decrease curiosity funds—have offered about $400 billion of the surplus financial savings since 2019, and nonmortgage debt has added about $110 billion because the constructive money circulation from scholar loans is partly offset by the destructive money circulation of bank cards. In fact, diminished bank card balances place households properly for future consumption: since diminished balances sometimes imply that extra credit score is offered for future use.

Different Indicators of Households’ Monetary Well being

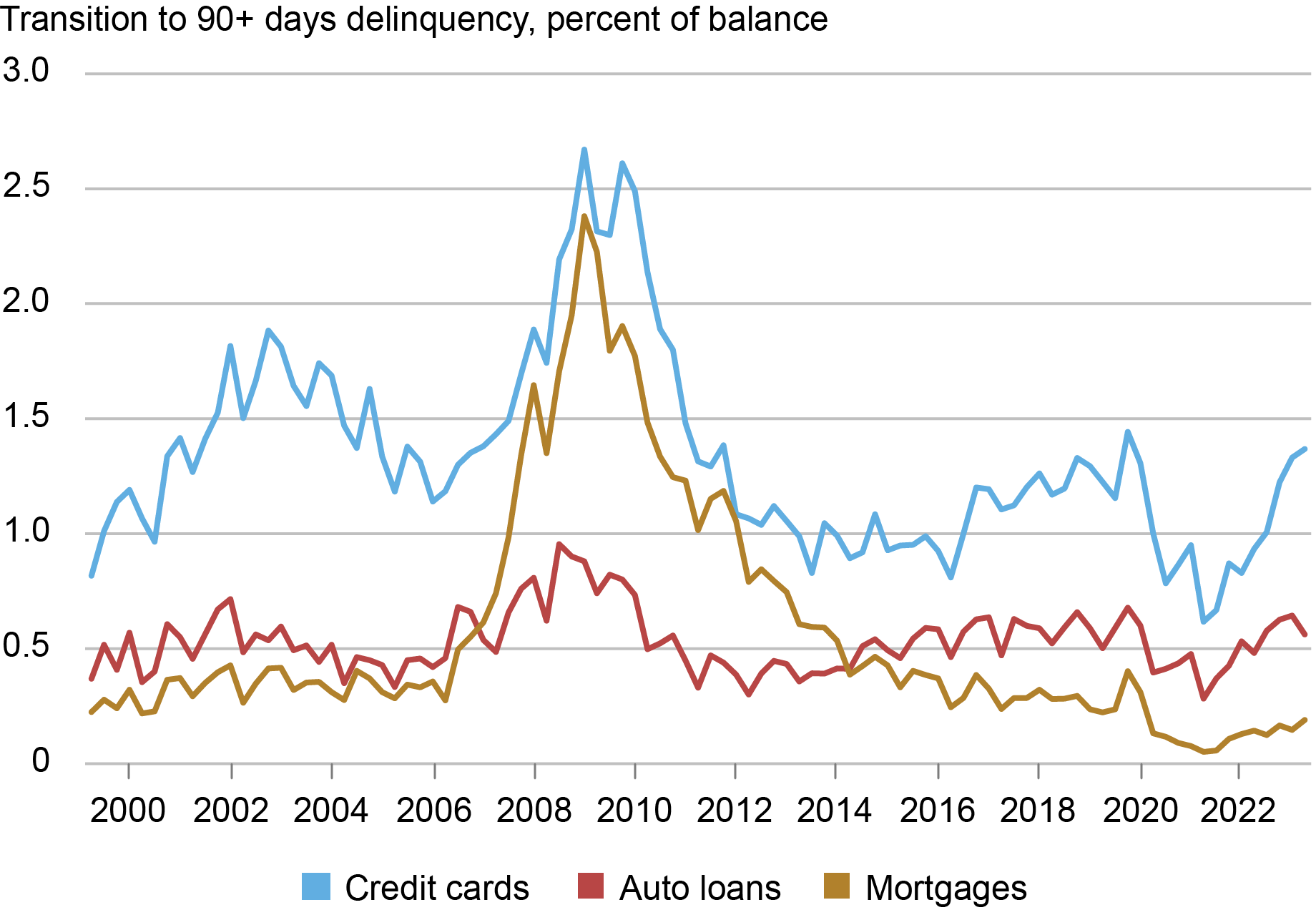

These constructive money flows from debt recommend that the family sector is in a powerful place. Different indicators additionally assist this evaluation. Debt delinquencies are usually low, led by remarkably low mortgage delinquencies (proven in gold within the subsequent chart). Auto mortgage and bank card delinquencies, then again, have risen pretty sharply from their troughs through the pandemic and are actually again to their 2019 ranges. A key query going ahead is whether or not these delinquency charges will stage off or proceed to rise. An extra improve in delinquencies would point out that, for no less than some households, money circulation has turn into inadequate to assist their monetary obligations.

Will Delinquency Charges Proceed to Rise?

Supply: New York Fed Shopper Credit score Panel / Equifax.

As a second set of indicators, we use knowledge from the New York Fed’s Survey of Shopper Expectations to evaluate households’ near-term expectations concerning their spending, debt delinquency, family earnings, and earnings development. Median year-ahead anticipated spending development has retreated considerably from its excessive 2022 ranges, however its present studying of 5.3 % and six-month common of 5.4 % stay properly above its pre-pandemic stage in February 2020 of three.1 %.

The identical sample is true for median anticipated family earnings development and median anticipated earnings development, which have averaged 3.2 % and a couple of.9 %, respectively, in current months—properly above their six-month averages going into the pandemic (2.7 % and a couple of.4 %, respectively). In line with these findings, the median chance of lacking a debt cost over the following three months has been comparatively low and secure over the previous six months at a median of 11.3 %, in comparison with a six-month common of 12.2 % going into the pandemic.

What’s Subsequent?

General, households report strong and secure expectations for spending development, according to our proof on the energy and liquidity of family stability sheets, together with comparatively low delinquencies. In fact, the interval of very low rates of interest that supported many of those developments is decidedly over, no less than for now, suggesting that family funds will seemingly tighten additional within the coming months. Moreover, the resumption of scholar mortgage funds might have substantial destructive results on weak households. We’ll return to this vital subject in our accompanying put up.

Andrew F. Haughwout is the director of Family and Public Coverage Analysis within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Donghoon Lee is an financial analysis advisor in Shopper Conduct Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Daniel Mangrum is a analysis economist in Equitable Development Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Jonathan McCarthy is an financial analysis advisor in Macroeconomic and Financial Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Davide Melcangi is a analysis economist in Labor and Product Market Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Joelle Scally is a regional financial principal within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Wilbert van der Klaauw is the financial analysis advisor for Family and Public Coverage Analysis within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Learn how to cite this put up:

Andrew Haughwout, Donghoon Lee, Daniel Mangrum, Jonathan McCarthy, Davide Melcangi, Joelle Scally, and Wilbert van der Klaauw, “An Replace on the Well being of the U.S. Shopper,” Federal Reserve Financial institution of New York Liberty Avenue Economics, October 18, 2023, https://libertystreeteconomics.newyorkfed.org/2023/10/an-update-on-the-health-of-the-u-s-consumer/.

Disclaimer

The views expressed on this put up are these of the writer(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the writer(s).