{kind=link}

Prince Pipes & Fittings Ltd. – Pure Play Plastic Pipe Firm

Prince Pipes and Fittings Restricted (PPFL) is one in every of India’s largest producers of built-in piping options & multi polymers, primarily based in Mumbai, Maharashtra. Integrated in 1987, Prince is without doubt one of the quickest rising firms within the Indian pipes and fittings trade. For over 3 a long time, the corporate has been engaged within the manufacturing of polymer piping options in 4 forms of polymers – CPVC, UPVC, HDPE, PPR. With a community of greater than 1,500 distributors, PPFL is steadily growing its pan-India distributor base to make sure stronger buyer proximity and reply sooner to their wants. Prince Pipes and Fittings Restricted has 7 state-of-the–artwork manufacturing items situated throughout the nation at Haridwar (Uttarakhand), Athal & Dadra (Dadra and Nagar Haveli), Kolhapur (Maharashtra), Chennai (Tamil Nadu), Jaipur (Rajasthan) and Sangareddy (Telangana).

Merchandise & Companies:

It has a number of merchandise unfold throughout a number of segments.

- Plumbing – FLOWGUARD PLUS, EASYFIT AND EASYFIT RE.

- Industrial – GREENFIT, GREENFIT BLUE, And many others.

- Sewage – SILENTFIT, ULTRAFIT and RAINFIT

- Underground – FOAMFIT, DRAINFIT, CORFIT and DURAFIT.

- Agri – AQUAFIT, SAFEFIT and PEFit Aqua

- Others – STOREFIT in Water storage phase and CABLEFIT in Cable ducting phase.

Subsidiaries: As on FY23, the corporate doesn’t have any subsidiaries.

Key Rationale:

- Management Place – PPFL is without doubt one of the high six gamers within the pipes & fittings market in India. The rising market place is supported by well-known manufacturers ‘Prince’ and ‘Trubore’ and the varied product choices with presence in un-plasticized polyvinyl chloride (UPVC), Chlorinated polyvinyl chloride (CPVC), Polypropylene random (PPR) and Excessive-density polyethylene (HDPE) segments. Prince has ~10% market share in total CPVC market and CPVC contributes ~20-25% in Prince’s total portfolio (quantity and worth). Within the total piping trade, Prince at present has 6.5-7.5% market share. Over the previous 5 years, PPFL has made strategic strikes to bolster its capability for increased margin merchandise, showcasing its dedication to progress and profitability. Notably, the corporate’s tie-up with Lubrizol has additional enhanced its CPVC pipe portfolio, signifying a give attention to product innovation and high quality. The corporate can be introducing worth added merchandise to make sure price effectivity and improve market share.

- New Launches – In Q1FY24, the corporate launched and unveiled its new assortment of luxurious taps and sanitaryware. Impressed by European bathware developments, the brand new vary entails a whole portfolio of world class taps. The vary goes by the names Aurum, Titanio, Platina, Tiara, Marquise. Matchless in model and design they’ve been rigorously curated following exhaustive trade analysis. Argento, Meta, Kristal and Palladium full the Prince Bathware line. Throughout Q4FY23, the corporate launched 2-new merchandise corresponding to WireFIT & OneFit (with Lubrizol).

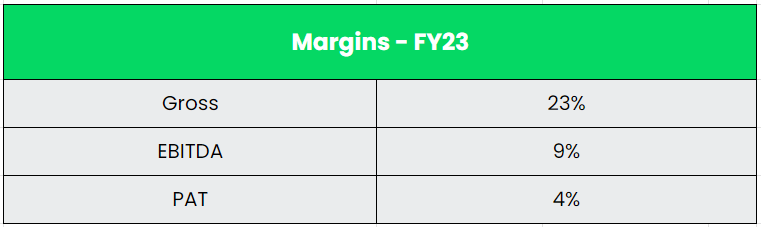

- Q4FY23 – The corporate’s income declined by 15.2% YoY to Rs.764 crore, impacted by 2.1% quantity decline (as a consequence of increased base of Q4FY22) and 13.3% fall in realizations (as a consequence of decrease PVC costs). Nonetheless, QoQ progress was wholesome at 8.3% (quantity progress of 1.4%) on account of improved demand throughout Agri and Plumbing /SWR (Soil, Waste and Rainwater) pipes portfolio. EBITDA rose 5.6% YoY and 113.5% QoQ, whereas EBITDA margins improved by 381bps YoY and 956bps QoQ to 19.4%, pushed by higher product combine (increased share from fittings). PAT elevated by 6.7% YoY and 165.9% QoQ to Rs.94 crore.

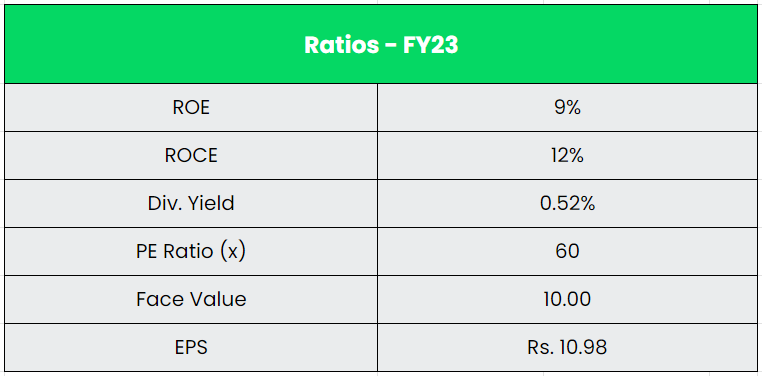

- Monetary Efficiency – The income and PAT CAGR have grown at 16% and 11% between FY18-23. Additionally, the corporate maintained a median ROCE of ~22% and a median ROE of ~18% for the previous 5 years. The Piping Volumes of the corporate have grown at a CAGR of 6% between FY20-23. The corporate stays long run debt free, whereas brief time period debt diminished from Rs.150 crore in FY22 to Rs.58 crore in FY23. Working capital days additionally fell from 68 in Mar’22 to 57 in Mar’23 as each debtor and stock days improved.

Business:

India’s excessive progress crucial in 2023 and past will considerably be pushed by main strides in key sectors with infrastructure improvement being a important drive aiding the progress. Infrastructure is a key enabler in serving to India grow to be a US$ 26 trillion economic system. Infrastructure improvement is at all times the important thing progress driver for Piping Business. Indian plastic pipes trade has traditionally grown sooner than the GDP led by a number of components like actual property, irrigation, city infrastructure and sanitation initiatives. At the moment, plastic pipes market is valued at ~Rs.400 bn with organized gamers accounting for ~67% of the market. By finish use, 50-55% of the trade’s demand is accounted by plumbing pipes utilized in residential & business actual property, 35% by agriculture and 5-10% by infrastructure and industrial initiatives. Between FY09-21 trade grew at 10%-12% CAGR, whereas demand is anticipated to increase at 12%-14% CAGR between FY21-25 and greater than Rs 600bn by FY25E led by a pointy enhance in authorities spending on irrigation, WSS initiatives (water provide and sanitation), city infrastructure and alternative demand.

Development Drivers:

- Underneath Finances 2023-24, capital funding outlay for infrastructure is being elevated by 33% to Rs.10 lakh crore (US$ 122 billion), which might be 3.3% of GDP and nearly thrice the outlay in 2019-20.

- Underneath the Nationwide Infrastructure Pipeline (NIP), initiatives value Rs.108 trillion (US$ 1.3 trillion) are at present at totally different phases of implementation.

- Underneath Finances 2023-24, the Authorities has allotted a large Rs.70,000 Crore for the implementation of the Jal Jeevan Mission. It’s nearly 12x enhance in outlay since 2018-19.

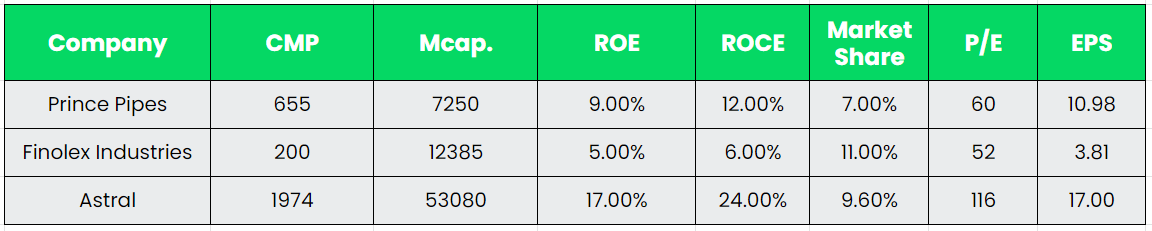

Opponents: Finolex Industries, Astral, and so on.

Peer Evaluation:

From the beneath comparability, it’s evident that Prince Pipes has much less penetrated and has an enormous market share hole to seize. By way of Fundamentals, Astral Pipes stays strongest because it has a diversified enterprise aside from Piping. So, Prince with its full give attention to Piping & Becoming phase will pave method for a robust progress.

Outlook:

The corporate has guided for a 12-14% quantity progress in FY24 (excluding Q1FY24 impression). On EBITDA margins, firm reiterated their steering of 13-15%. On-going Agri demand is strong as a consequence of higher affordability & past-2/3 seasons have been muted. Administration acknowledged that demand from Jal Jeevan Mission can be very wholesome, nonetheless firm doesn’t deal immediately. The corporate has introduced greenfield enlargement in Bihar to cater the demand in East. General Capex in FY24 will incur a price of Rs.150 crore (together with land, plant and gear prices) & the Bihar Plant will probably be operational from Q4FY25. The breakup will probably be Rs.75-80 crore for land and constructing for Bihar plant & Rs.80-85 crore for normal capex. By FY25 finish, firm may have 315k MTPA current capability, 35k MTPA coming in East + brownfield addition in planning phases. Apart from, the corporate plans to proceed including value-added merchandise to its portfolio – corresponding to: floor drainage system and silent drainage system – which had been launched in Q3FY23.

Valuation:

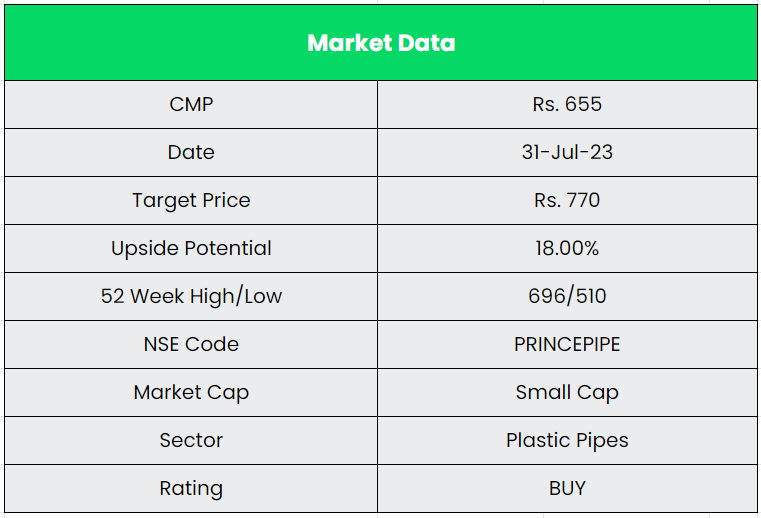

We stay optimistic on the corporate’s long run progress prospects, given its fixed portfolio enhancement and model constructing, widening attain and wholesome trade outlook. We suggest a BUY ranking within the inventory with the goal value (TP) of Rs.770, 30x FY25E EPS.

Dangers:

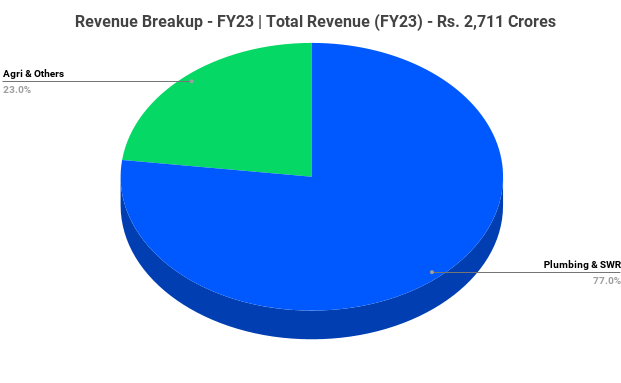

- Economical Threat – Any slowdown in actual property and infrastructure will immediately impression the demand for plumbing and sewerage infrastructure piping system which contributes ~77% of Firm’s income.

- Uncooked Materials Threat – Any fluctuations in uncooked materials costs like PVC or CPVC resins or foreign exchange will negatively impression profitability of the corporate.

- Aggressive Threat – The pipes and fittings trade are extremely aggressive, particularly within the commoditized merchandise phase, which has low differentiation, thus ensuing within the model dealing with competitors from each organized and un-organized segments. Any enhance in aggressive depth might negatively impression enterprise and financials.

Different articles you could like

Put up Views:

5,346