{kind=link}

Mastek Ltd. – Cloud Transformation Associate

Mastek, is a turnkey and trusted digital engineering and Cloud transformation associate that delivers Modern options and enterprise outcomes for purchasers in Healthcare & Life Sciences, Retail, Manufacturing, Monetary Companies, Authorities/Public Sector, and so on. It permits buyer success and decomplex digital for enterprises by enabling them to unlock the facility of knowledge, modernize functions to the Cloud, and speed up digital benefit. A most popular Oracle associate with a robust pool of 2000+ Oracle consultants and 100+ industry-specific options. Mastek’s ~5500 robust workforce operates out of 40+ nations (within the UK, Americas, Europe, Center East, and APAC) to ship enterprise worth with velocity. MST Options, a Mastek firm, is a Summit-level Salesforce consulting associate trusted by a number of Fortune 1000 enterprise purchasers.

Merchandise & Companies:

The corporate’s major companies embrace software growth, software upkeep & assist, ERP and cloud migration, enterprise intelligence & analytics, agile consulting, assurance & testing and digital commerce.

Subsidiaries: As on FY23, the corporate had 22 subsidiaries.

Key Rationale:

- Established Place – Mastek’s established enterprise profile is supported by its robust monitor file within the digital transformation enterprise and wholesome presence in Oracle cloud-based options implementation by way of Evosys. The corporate now additionally has presence within the Salesforce consulting enterprise with the acquisition of MST Options. The corporate’s key service traces embrace digital software engineering, together with software growth work, cloud native growth, DevSecOps work, and cloud and enterprise software, which incorporates implementation of Oracle cloud and enterprise functions. Mastek has a robust monitor file within the Authorities & training, Well being & life Sciences, Retail, Manufacturing and Monetary companies verticals with every producing 45%, 15%, 12%, 17% and 11% respectively, of complete income in Q1FY24.

- Latest Acquisition – Mastek Inc. has knowledgeable that it has authorised to signal the definitive Membership Curiosity Buy Settlement to amass the 100% Membership Curiosity of BizAnalytica LLC. BizAnalytica LLC is an impartial knowledge cloud and modernization specialist within the Americas area. The acquisition consideration contains an upfront cost of $16.72 million and an earn-out of as much as $24.0 million topic to reaching monetary targets. The indicative time interval for completion of the acquisition is anticipated to be, on or earlier than September 30, 2023.

- Q1FY24 – Income from operations stood at Rs.725 crore in Q1FY24, up 2% QoQ/27% YoY. Income development was pushed by demand for Digital Engineering, Expertise, and Cloud Transformation companies. Center East and USA have proven sturdy efficiency, whereas the UK was impacted by fewer working days within the quarter. Geographically, Center East recorded robust development, up 33.5% QoQ/57% YoY. Key market Europe declined, down 1% QoQ whereas US and ROW declined 0.5%/3% QoQ. EBITDA margin stood at 17.5%, down 20 bps QoQ. The 20-bps discount was largely as a consequence of increments which was offset by foreign money and different working levers. Web Revenue stood at Rs.74 crore was flat QoQ and a decline of 12% YoY. The Firm added 22 new purchasers in Q1FY24. Complete energetic purchasers throughout Q1FY24 had been 436 as in comparison with 464 in Q4FY23. As on thirtieth June, 2023, the corporate had a complete of 5,592 workers. Final twelve months attrition at 20.4% in Q1FY24 as compared with 21.0% in Q4FY23.

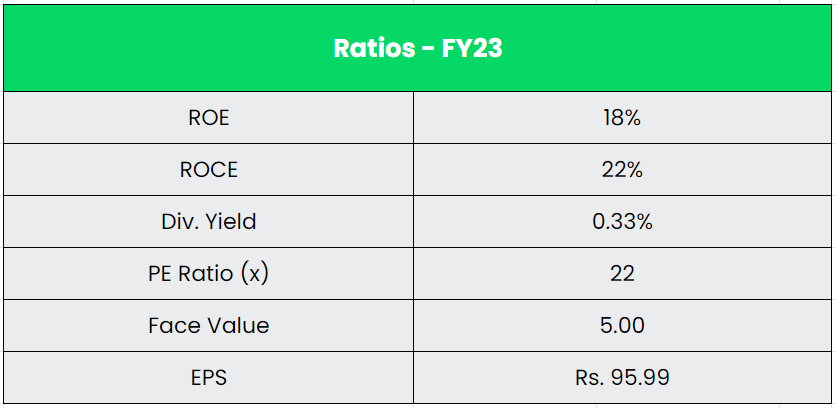

- Monetary Efficiency – The 5 Yr income and revenue CAGR stands at 26% and 33% respectively. The steadiness sheet of the corporate is robust with a debt-to-equity ratio of 0.2x. 12 months order backlog of the corporate is round Rs.1,763.9 crore ($215.0 million) in Q1FY24, as in comparison with Rs.1,509.3 crores ($191.1 million) in Q1FY23, up 16.9% in rupee phrases and 9.7% in fixed foreign money phrases on YoY foundation and Rs.1,794.1 crore ($218.3million) in Q4FY23, down 1.7% in rupee phrases and decline of two.6% in fixed foreign money phrases on QoQ foundation.

Business:

India’s know-how {industry} income is estimated to be $245 Bn in FY23. Know-how exports at $194 Bn, are anticipated to develop at 9.4% in reported foreign money phrases. In FY23, the know-how {industry} is estimated to have 5.4 Mn workers and contribution of 53% in India’s service exports. With 23 new unicorns, India grew to become the 2nd highest nation by way of variety of unicorns added in 2022. 1300+ new tech startups emerged in 2022. Indian software program product {industry} is anticipated to succeed in US$ 100 billion by 2025. By 2026, widespread cloud utilisation can present employment alternatives to 14 million individuals and add US$ 380 billion to India’s GDP. Indian corporations are specializing in investing internationally to develop their international footprint and improve their international supply centres. Indian SaaS corporations noticed 2x development in share of world markets. India has as many as 59 variety of SaaS unicorns and potential unicorns. Web connections rose to 83.69 crore in 2022 from 25.15 crore in 2014.

Development Drivers:

- Within the Union Funds 2023-24, the allocation for IT and telecom sector stood at Rs. 97,579.05 crore (US$ 11.8 billion).

- The pc software program and {hardware} sector in India attracted cumulative overseas direct funding (FDI) inflows value US$ 94.92 billion between April 2000-March 2023.

- Over 45 new knowledge centres to return up in India by 2025. Information centres in India entice funding of $10 Bn since 2020.

Rivals: Cyient, Zensar Applied sciences, and so on.

Peer Evaluation:

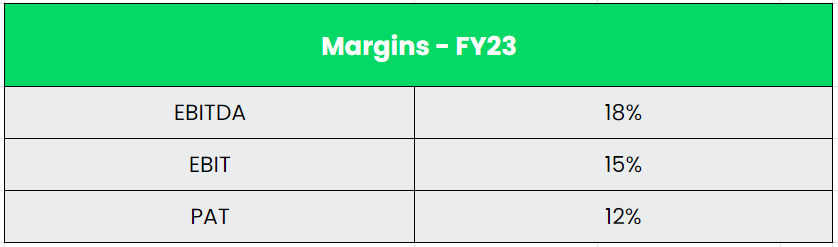

By way of fundamentals, Mastek is means higher than its friends with excessive return ratios and margins. Additionally, Mastek is buying and selling at a reduction (P/E) when in comparison with its rivals.

Outlook:

The administration conveyed their contentment with the order ebook within the US and Americas area, however sure offers requiring prolonged finalization durations. They foresee sturdy income development stemming from consecutive order bookings on this geographical space. Within the UK, substantial offers are within the pipeline, evoking optimism. The administration affirmed that within the ongoing quarter, with incremental progress, minor margin fluctuations would possibly come up, but the corporate goals to revive a margin vary of 17% to 19% by Q3 and This fall. The corporate expressed a sanguine development outlook each quarter on quarter and year-on-year, striving for industry-leading growth. Mastek has cultivated a gradual and foreseeable income stream from the UK’s public sector in recent times, propelled by the UK authorities’s introduction of the Digital Outcomes and Specialists (DoS) framework in 2016 as a successor to the Digital Companies-2 framework. The administration indicated that the momentum of income development within the UK public sector will persist in upcoming quarters as a consequence of amplified expenditures on digital transformation initiatives by the UK authorities and the acquisition of recent purchasers. Moreover, an acceleration of development momentum within the US enterprise is anticipated, attributable to robust demand for built-in digital commerce options, burgeoning deal sizes, and the addition of recent clientele.

Valuation:

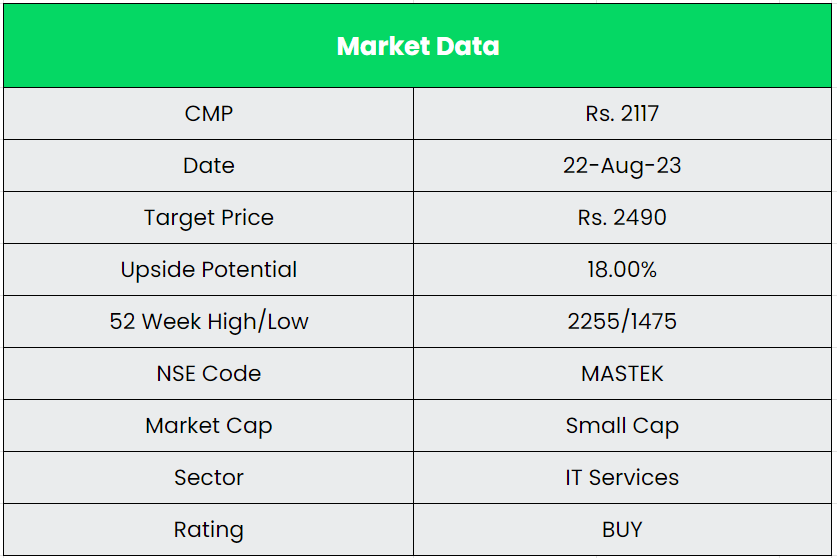

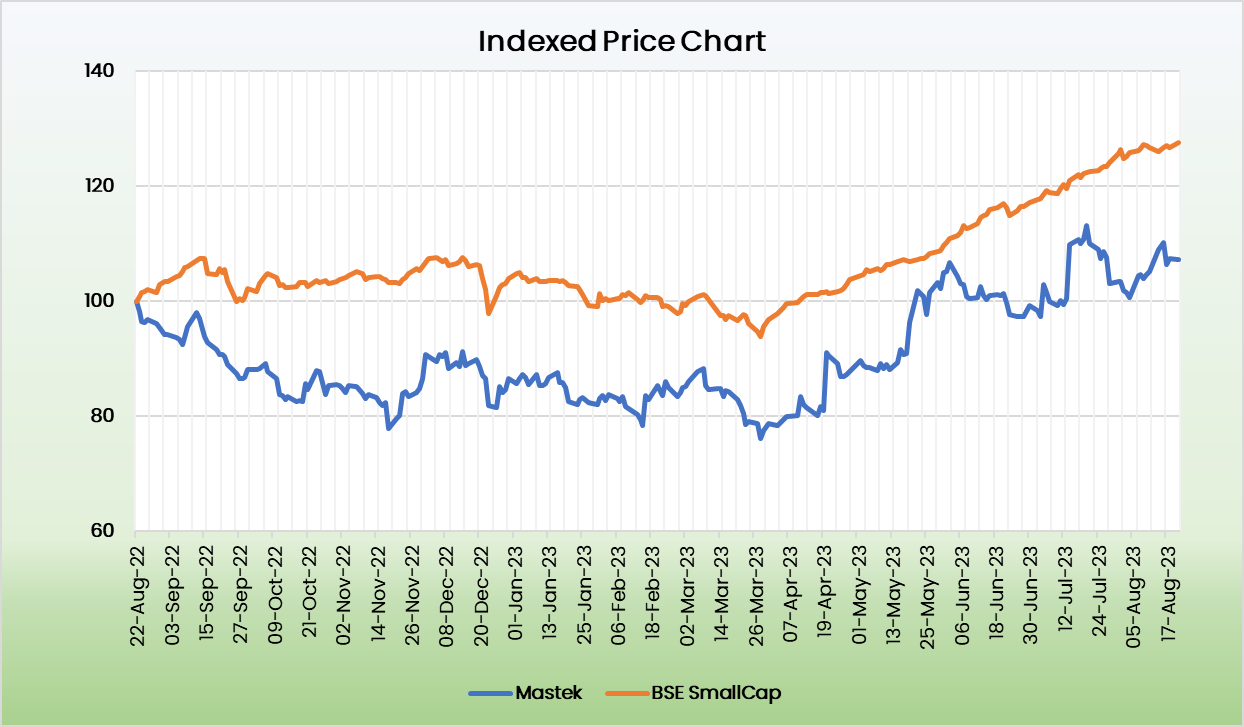

We consider the corporate is effectively positioned because of the full bundle portfolio, the robust tie-up with the UK public sector in addition to the momentum in each Americas and Center East markets which is delivering the robust development. We suggest a BUY ranking within the inventory with the goal worth (TP) of Rs.2490, 18x FY25E EPS.

Dangers:

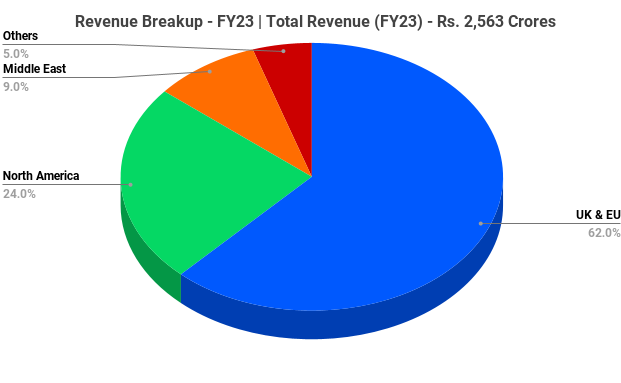

- Focus Danger – Mastek derived 62% of its working income in FY2023 from the UK and EU markets. The corporate continues to generate most of its revenues from the UK’s public and healthcare sectors, which exposes it to danger of any adjustments within the UK Authorities’s coverage on IT spending.

- Aggressive Danger – Given the extreme competitors within the {industry}, Mastek’s revenue margins are inclined to pricing pressures and wage inflation.

- Foreign exchange Danger – A lot of the revenues and margins are uncovered to foreign exchange dangers, though Mastek’s hedging mechanisms mitigate this danger to an extent.

Different articles it’s possible you’ll like

Put up Views:

4,320