{kind=link}

Blue Star Ltd. – Diversified Cooling Options

Blue Star is India’s main air con and industrial refrigeration firm, with an annual income of over Rs.7,000 crore, a community of 32 workplaces, 5 fashionable manufacturing amenities, and 4,040 channel companions. The corporate has over 8,000 shops for room ACs, packaged air conditioners, chillers, chilly rooms in addition to refrigeration merchandise and techniques. Blue Star’s built-in enterprise mannequin of a producer, contractor, and after-sales service supplier permits it to supply an end-to-end answer to its clients, which has proved to be a major differentiator within the market. The corporate fulfils the cooling necessities of a lot of company, industrial in addition to residential clients. Blue Star has additionally forayed into the residential water purifiers enterprise with a classy and differentiated vary, together with India’s first RO+UV scorching and cold-water purifiers in addition to air purifiers and air coolers.

Merchandise & Providers:

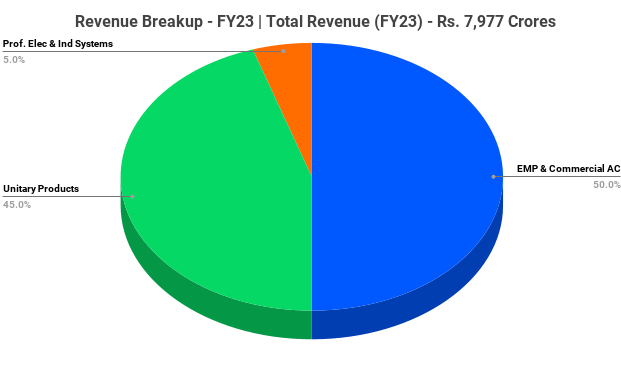

The Firm caters to a few kinds of segments.

- EMP (Electro-Mechanical Tasks) and Business Air Conditioning techniques – This phase covers the design, manufacturing, set up, commissioning and upkeep of central air con vegetation, packaged/ducted techniques and Variable Refrigerant Stream (VRF) techniques to Business Buildings, Retail, Hospitals, Inns, Schooling, Industrial Amenities, and so forth.

- Unitary Merchandise – This phase focuses on a variety of up to date and extremely energy-efficient room air conditioners (RAC) for each residential in addition to industrial functions. It additionally manufactures and markets a complete vary of business refrigeration merchandise and chilly chain gear. The vary of unitary merchandise additional consists of water purifiers, air purifiers and air coolers.

- Skilled Electronics & Industrial Programs – This phase consists of options and system Integration in MedTech, Industrial Programs and Information Safety by the corporate’s subsidiary, Blue Star Engineering & Electronics Restricted.

Subsidiaries: As on FY23, the corporate has 9 subsidiaries and a couple of Joint Ventures.

Key Rationale:

- Robust Market Place – Blue Star is likely one of the sturdy gamers within the shopper sturdy enterprise, significantly in industrial, RAC techniques and throughout mission enterprise in associated segments with a longtime observe file of over six many years and demonstrated capabilities in executing tasks throughout mission companies in home and worldwide markets. It instructions a management place in ducted AC phase, whereas #2 place beneath variant refrigerant move (VRF) and chiller product phase. As on March 31, 2023, the corporate has 13.5% market share in RAC alongside in depth distribution community with over 8,000 shops.

- Diversified Profile – Presence in EMP & Business and Unitary Merchandise (Largely B2C) segments mitigates the chance of slowdown in anybody phase or trade. Blue Star depends nearly equally on each these segments when it comes to income and profitability. The Unitary Merchandise phase contributed to round 45% of income in FY23, with EBIT margin of round 8% and the contribution of EMP phase was larger at 50% with EBIT margin of ~7%. The corporate can be changing into self-sufficient by commencing new manufacturing amenities in each RACs in addition to industrial refrigeration, which might result in a discount in its dependency on imports and price financial savings, led by backward integration. It’ll additionally assist the corporate to faucet the export markets.

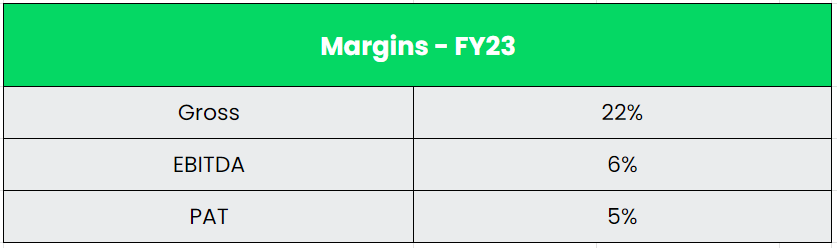

- Q1FY24 – Blue Star’s Q1FY2024 consolidated outcomes have been impacted by muted efficiency of the RAC enterprise. Income got here in at Rs.2,226 crore (up 13% YoY). Gross margin improved to 22.2% (up 110 bps YoY). EBITDA grew by ~18% YoY to Rs.145 crore. EBITDA margin inched up by ~30 bps YoY to six.5%. Web revenue progress was restricted to ~12% YoY to Rs.83 crore as a result of steep enhance within the curiosity price. The orders gained throughout Q1FY24 is Rs.1225 crore as towards Rs.1366 crore on Q1FY23. The overall pending order e book as on Q1FY24 stands at Rs.5106 crore (64% of the FY23 income). Whereas there have been fewer orders from the industrial constructing sector, the corporate witnessed wholesome bookings from factories and knowledge middle sectors.

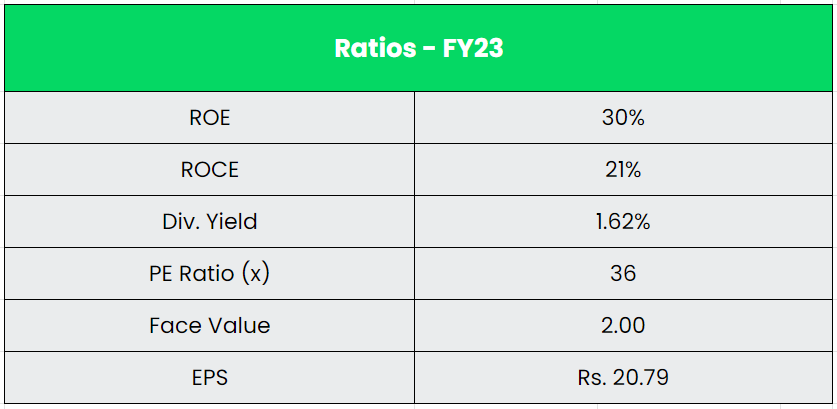

- Monetary Efficiency – The three Yr income and revenue CAGR stands at 14% and 24% respectively between FY20-23. The corporate plans capex of ~Rs.750 crore within the subsequent three years, which is prone to be funded by QIP, topic to board and shareholders’ approvals. The key portion of the capex is prone to be executed in FY2024 and FY2025. Regardless of important investments in manufacturing capability growth, continued concentrate on margin enchancment and dealing capital effectivity enabled enchancment in ROCE.

Trade:

The White Items market is estimated to cross $21 Bn by 2025 increasing at a CAGR of 11%. Home manufacturing contributes almost $4.6 Bn on a mean to this trade. The Indian room air conditioner market is prone to attain USD 5 billion by FY28 with a compound annual progress price (CAGR) of 10%. In keeping with the Energy Trade, the market share of the extra environment friendly, variable velocity (inverter) RACs (room ACs) elevated from 1% in FY16 to 77% in FY23, whereas that of the fastened velocity RAC, decreased from 99% to 23% throughout the identical interval. The general marketplace for room ACs reached 6.6 million models by 2020-21 from 4.7 million models in 2015. The volumes of the RAC trade are anticipated to publish a 15-20% progress in FY2024 following the sturdy progress of 26-28% in FY2023. The cumulative share (by quantity) of 4 and five-star inverter RACs is predicted to extend to 30-40% in FY2025 from 20-23% in FY2022. AC Exports elevated at a CAGR of 9% from $165 Mn in 2018 to $233 Mn in 2022.

Progress Drivers:

- In contrast with a worldwide common of 30%, solely 7% of Indian houses have air conditioners, in keeping with numerous research and estimates. Even when the penetration will increase to 10 or 12% within the subsequent 4 or 5 years, it would translate into thousands and thousands of air conditioners, signifying the large progress potential.

- Consistently rising temperatures and prolonged summers in India has made Air Conditioners a necessity fairly than a luxurious in Indian households.

- Authorities has launched a PLI Scheme for AC producers which provides incentive of round Rs.6238 crore. The production-linked incentive (PLI) scheme to assist scale back imports dependence on elements to 20-30% from the present ranges of 60-70%.

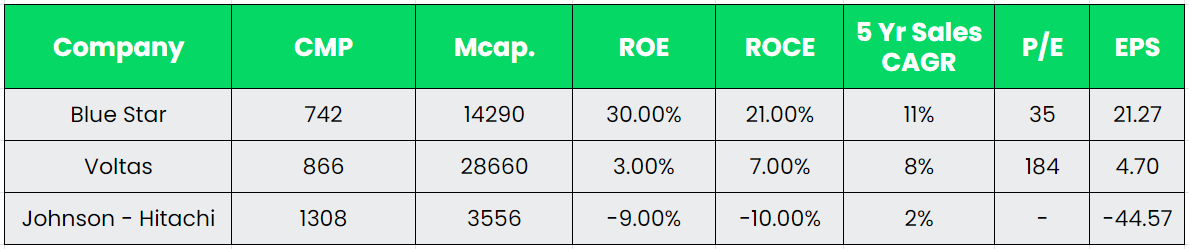

Rivals: Voltas, Johnson Controls – Hitachi.

Peer Evaluation:

Voltas and Johnson – Hitachi are the shut opponents of Blue Star, having A/C enterprise as their principal phase whereas Lloyd’s is one in every of its many enterprise segments by Havells. By way of fundamentals, it’s clear that blue star is having the higher hand in each facet.

Observe – P/E is predicated on TTM EPS.

Outlook:

Blue Star has maintained its management place within the standard and inverted duct air con system, deep freezers, storage water coolers, and modular chilly rooms. It has acquired orders from Foxconn Bangalore, IOCL Baroda, and Mindspace Thane for its lately launched centrifugal chillers. In Q1FY2024, the RAC trade has declined by 10% YoY, whereas the dip within the firm’s enterprise was decrease than that resulting from a big share of institutional gross sales. Administration has revised down its income steering for the RAC enterprise to 10-15% for FY2024, just like the trade’s progress ranges, from its earlier steering of round 15-20% YoY progress. EBIT margin for FY2024 could be within the vary of 8.0-8.5%. Blue Star’s technique is to spend money on and construct each B2B and B2C companies as sturdy engines of progress. Additionally, the Administration’s near-term aim is to cross the full income of greater than Rs.10,000 crore. The corporate’s market share has improved from simply 12.3% in FY19 to 13.5% in FY23 and it goals to develop the identical to fifteen% within the subsequent 2 years.

Valuation:

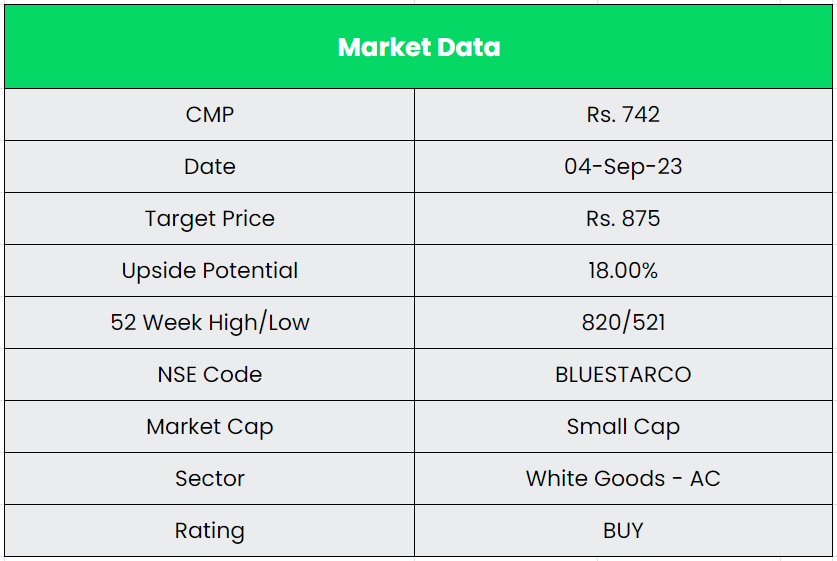

We consider Blue Star will proceed to seize the market share from its opponents by supplier and capability growth. The corporate additionally plans to discover export alternatives in international locations like USA and Europe. We advocate a BUY ranking within the inventory with the goal worth (TP) of Rs.875, 50x FY25E EPS.

Dangers:

- Regulatory Danger – All the companies within the Firm’s Unitary Merchandise phase are seasonal in nature. Unexpected climate patterns equivalent to prolonged winter, nice summer time, lower than regular monsoon, extra monsoon or any type of disruptions through the peak promoting seasons might influence the income progress.

- Aggressive Danger – A number of Indian and international gamers within the air con enterprise are within the means of establishing or increasing their very own manufacturing amenities in India to faucet the underpenetrated market. Such gamers may resort to aggressive pricing to seize market share leaving the corporate weak to important lack of enterprise to the opponents.

- Uncooked Materials Danger – Key elements equivalent to compressors, copper tubes, digital elements, indoor models for cut up air conditioners, and inverter drives, are sourced from distributors in China and another international locations. Any disruption in provide precipitated resulting from geopolitical causes, imposition of non-tariff boundaries might considerably influence the corporate’s manufacturing.

Different articles you could like

Submit Views:

3,765