{kind=link}

AIA Engineering Ltd – International Options Supplier for Mining Corporations

Integrated in 1991, AIA Engineering Ltd. specialises within the design, improvement, manufacturing, set up, and servicing of excessive chromium put on resistant elements for grinding equipments in cement, mining, quarry and thermal power-generating industries. Headquartered in Ahmedabad, Gujarat, with a legacy of greater than 45 years in India and with its worldwide advertising and marketing arm Vega Industries, the corporate set benchmarks in high quality, companies and innovation, establishing a powerful status as a worldwide answer supplier. AIA and Vega Industries are world leaders in manufacturing put on elements for cement vegetation. As of 31 March 2023, the corporate has 6 vegetation in India, and it’s serving to greater than 120 nations internationally.

Merchandise and Companies

AIA’s product portfolio consists majorly of excessive chrome grinding media, mill liners, vitality environment friendly pulp lifter system predominantly serving mining and cement trade. The corporate additionally provides blow bars, hammer, impellers, anvil, feed disk, body liners and so on for quarries, mixture and recycling trade. On the companies entrance it has capabilities to assists in alloy choice for put on discount, set up assist, liner put on monitoring, alloy optimisation for enhancing steel recoveries, mill audits and so on.

Subsidiaries: As of FY23, the corporate has 11 subsidiaries and one affiliate firm.

Key Rationale

- Enlargement plans – Throughout FY23, AIA commissioned mill liners plant, including an incremental capability of fifty,000 TPA. It added two Hybrid Tasks (2.1 MW Windmill + 1.89 MWp Photo voltaic) at Village Dedan, Gujarat, taking complete Renewable Vitality Capability to 32.28 MW. The corporate expanded capability of fifty,000 MT in castings at Kerala GIDC Facility. It continues to proceed with its brownfield capability enlargement of grinding media capability. With an ongoing capex of Rs.250 crore, that is estimated to be commissioned by the tip of FY2024-25. The corporate is present process a restructuring of its manufacturing operations encompassing a spread of strategic initiatives aimed toward optimising operational effectivity. These initiatives embody some capability de-bottlenecking and restructuring, creation of warehouse house, sample storage amenities and associated infrastructure funding at an estimated value of Rs.200 crore. Firm anticipates attaining 20,000 MT of capability addition in castings due to de-bottlenecking. The corporate acquired 30% stake in a excessive expertise design functionality firm primarily based in Australia, aiming to speed up the penetration within the total mid-liner enterprise.

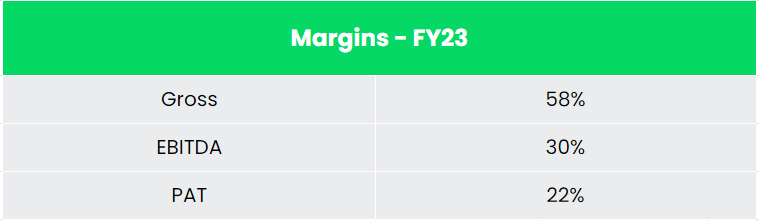

- Q2FY24 – Throughout the quarter, AIA achieved 77,725 metric tonnes gross sales which converts to income of round Rs.1274 crore in comparison with the Rs.1312 crore of Q2FY23. The corporate reported EBITDA of Rs.444 crore marking a rise of 29% YoY in comparison with the Rs.344 crore of Q2FY23. The online revenue elevated by 32% to Rs.323 crore in comparison with the Rs.245 crore of identical interval of the earlier 12 months. The EBITDA and internet revenue margin for the quarter stood at 35% and 25% respectively, advantages from improved product combine and discount in freight prices. Throughout the interval the corporate obtained export advantage of Rs.21 crore which is according to the advantages below RoDTEP and obligation disadvantage. The corporate skilled a slight dip within the gross sales quantity in mining section however was offset by a rise of about 3,300 tonnes within the cement section.

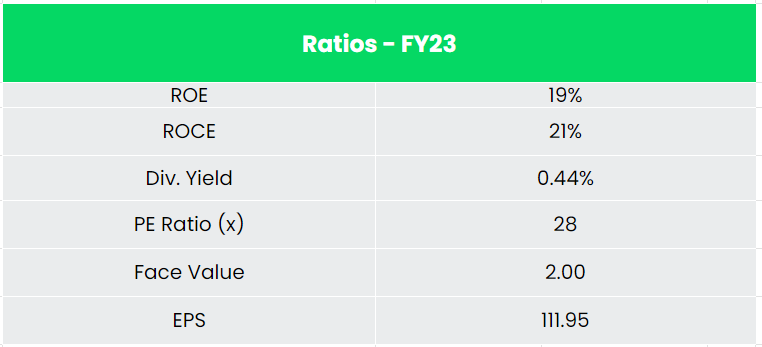

- Monetary efficiency – AIA has generated a income and PAT CAGR of 15% and 19% over the interval of 5 years (FY18-23). Common 5-year ROE & ROCE is round 16% and 20% for FY18-23 interval. The corporate has robust steadiness sheet with a sturdy debt-to-equity ratio of 0.08.

Trade

Minerals are treasured pure sources that function important uncooked supplies for basic industries, so the expansion of the mining trade is important for the general industrial improvement. The huge sources of quite a few metallic and non-metallic minerals that India is endowed with function a basis for the enlargement and development of the nation’s mining trade. India is the second-largest producer of coal on the earth and likewise the fourth-largest iron ore producer on the earth. The index of mineral manufacturing of the mining and quarrying sector for the month of June 2023 at 122.3, was 7.6% greater in comparison with the extent within the month of June 2022. With excessive allocation below the Union Finances 2023-24 for infrastructure, inexpensive housing schemes and highway tasks to gas the economic system, the home cement trade is poised for a quantity surge. As India has a excessive amount and high quality of limestone deposits through-out the nation, the cement trade guarantees enormous potential for development.

Development Drivers

As per the Union Finances 2023-24 Authorities authorized an outlay of US$ 32.57 billion (Rs. 2.7 lakh crore) for the Ministry of Highway Transport and Highways which is more likely to increase demand for cement. Below the housing for all section, in 2023-24 the funds estimate for Pradhan Mantri Awas Yojana is US$ 9.63 billion (Rs. 79,590 crore), a 66% rise than the final 12 months’s funds estimate of US$ 6.43 billion (Rs 48,000 crore) in 2022-23. The nation has allowed 100% FDI by way of automated route in mining sector.

Opponents: BEML Ltd.

Peer Evaluation

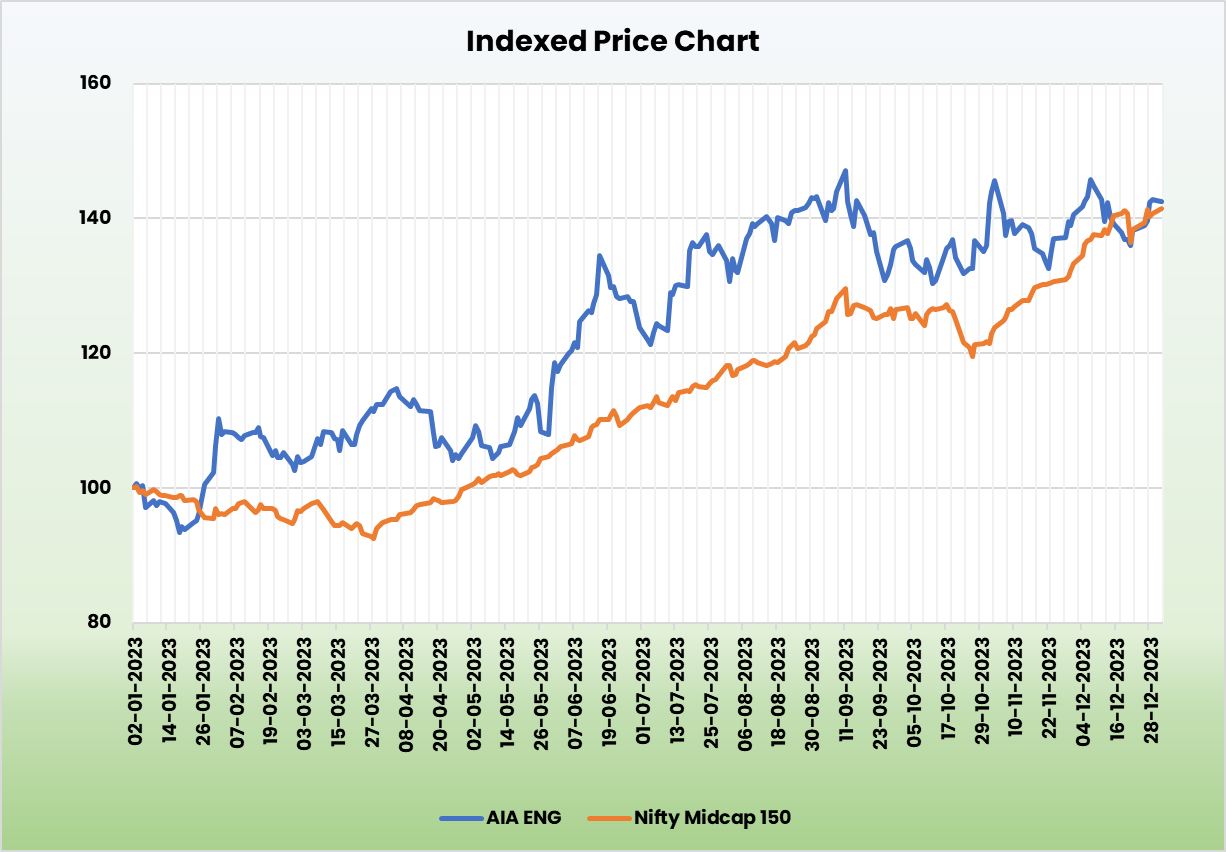

As compared with its listed competitor, with a sturdy development in income, AIA is forward by way of efficiency ratios, indicating the corporate’s monetary stability and its effectivity to generate earnings and returns from the invested capital.

The corporate is working in a comparatively oligopolistic market with non-public firms like Magotteaux Industries Personal Ltd (MIPL) and ME Elecmetal thought of as key rivals globally.

Outlook

The corporate has proposals to spend Rs.500 crore capex between FY24 and finish of March 2025 the place about 200 crore goes in direction of the grinding media enlargement, 200 crore in direction of total restructuring and debottleneck, 50 crore in direction of captive energy and different 50 crore for land and different necessities. 80,000 ton grinding media enlargement is on observe for being commissioned by December 2024. The corporate has given a long-term margin steerage of 23-24%. AIA with its increasing international footprint and lengthy gestation tasks in pipeline is predicted to generate strong revenues in mid and long run.

Valuation

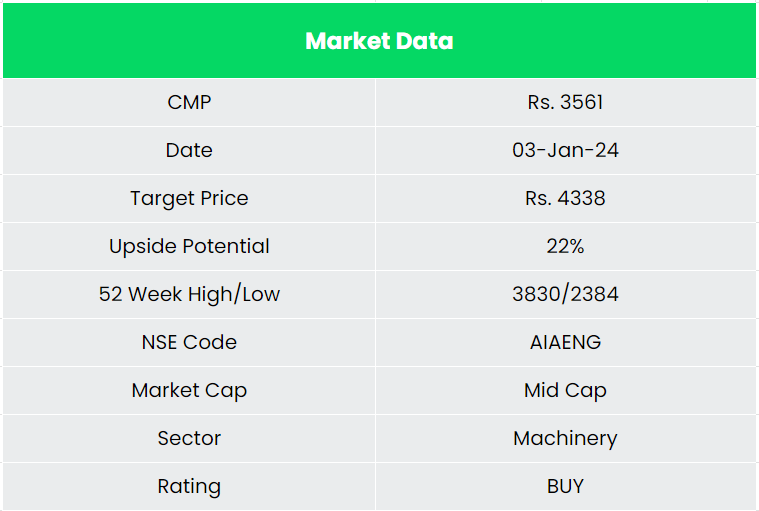

Given the numerous market share of the corporate coupled with robust entry obstacles to new gamers, we imagine that AIA Engineering Ltd has the potential to extend its income and profitability within the coming years. Therefore, we advocate a BUY ranking on the inventory with goal worth (TP) of Rs. 4338 at 22x FY25EPS.

Dangers

- Foreign exchange danger – The corporate has important operations in overseas markets and therefore is uncovered to foreign exchange danger. Any unexpected motion within the foreign exchange market can adversely have an effect on the corporate.

- Delays in finalising mission – Technical evaluations and negotiations with the consumer entities may take longer than anticipated to materialize.

- Allowing dangers – It takes on a median couple of years to safe permits wanted to start operations for mining firms, which could impression the turnover of the businesses related to the metals and mining sector as effectively.

Different articles it’s possible you’ll like

Publish Views:

101