{kind=link}

The Federal Open Market Committee (FOMC) communicates the stance of financial coverage by a goal vary for the federal funds charge, which is the speed set out there for uncollateralized short-term lending and borrowing of central financial institution reserves within the U.S. Because the international monetary disaster, the marketplace for federal funds has modified markedly. On this put up, we take a better have a look at who’s at the moment buying and selling within the federal funds market, in addition to the explanations for his or her participation.

The Fed Funds Market

The federal funds (or fed funds) market allows depository establishments to instantly commerce central financial institution reserves within the U.S. On this market, depository establishments and different monetary entities—primarily government-sponsored enterprises (GSEs)—borrow and lend funds on an uncollateralized foundation, usually with in a single day maturity. The fed funds market is vital for financial coverage implementation and has traditionally performed an vital function within the redistribution of reserves throughout the banking system. Previous to 2008, reserves have been within the tens of billions of {dollars} and the fed funds market was very energetic, with contributors constantly borrowing, lending, and intermediating all through the day to satisfy their statutory reserve necessities. Efficient October 1, 2008, Congress gave the Fed the authority to pay depository establishments curiosity on their reserve balances. As well as, the Fed has expanded its stability sheet to help the U.S. economic system—first in the course of the international monetary disaster and extra not too long ago in the course of the COVID-19 pandemic—resulting in reserves reaching $4 trillion in late 2021, as mentioned on this put up. On this new atmosphere, the necessity to actively borrow within the fed funds market has waned. Each day buying and selling quantity dropped from round $150-$175 billion, or round 2 p.c of economic financial institution belongings, previous to 2008 (as estimated on this put up) to round $60-$80 billion per day within the 2010s, growing to a mean of $110 billion, or 0.5 p.c of financial institution belongings, per day in 2023.

With reserves elevated within the banking system, who’s now borrowing and lending within the fed funds market? And why?

Debtors within the Fed Funds Market

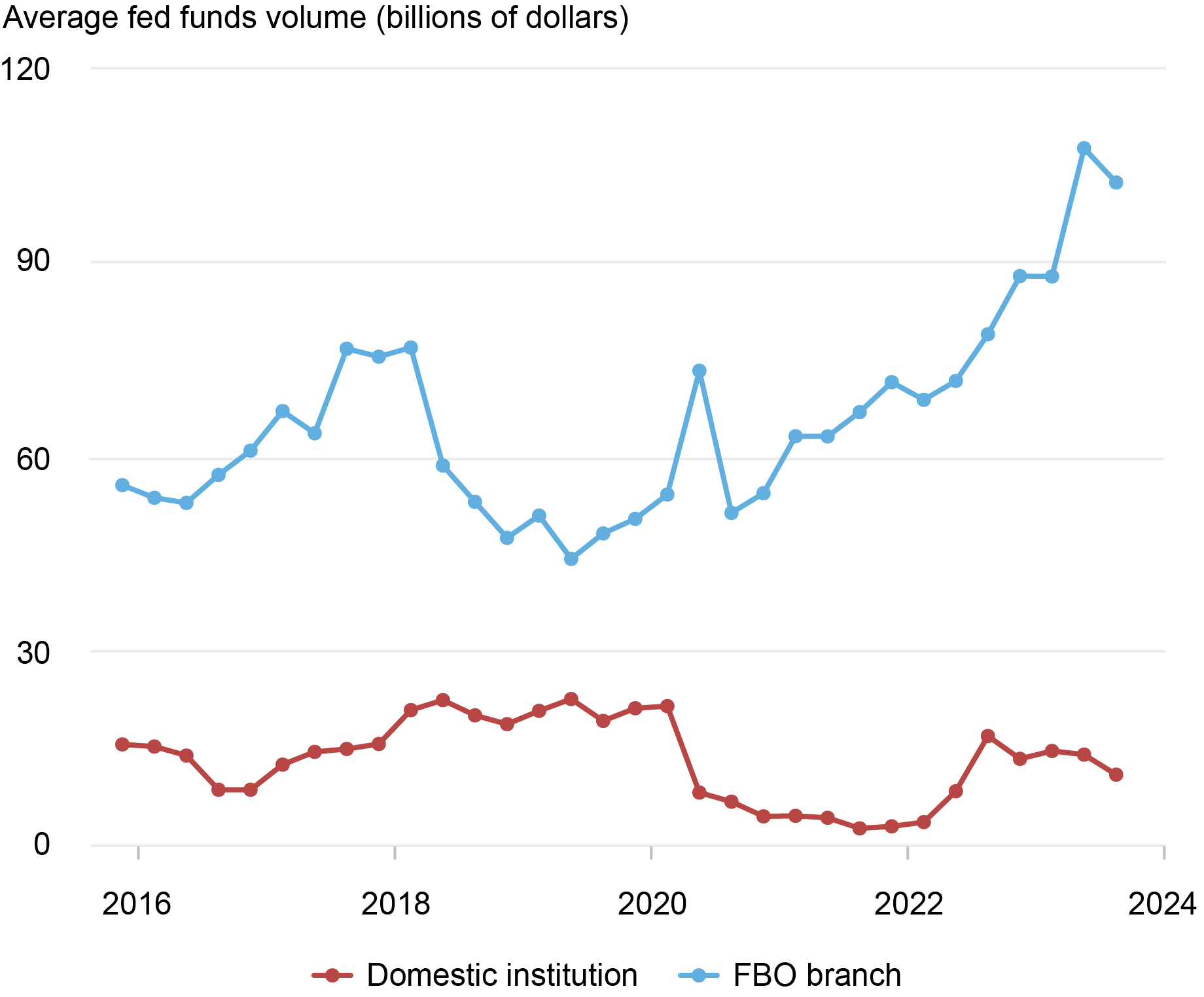

Because the chart beneath exhibits, the principle debtors within the fed funds market are the U.S. branches and companies of overseas banks (FBO branches). Since 2016, FBO branches have borrowed round $45-$110 billion per day, representing between 65 and 95 p.c of the full each day quantity within the fed funds market. FBO branches are the most typical construction of overseas banking within the U.S., and so they typically interact in actions much like these of home banks.

FBO Branches Are the Important Debtors within the Fed Funds Market

Sources: Federal Reserve Kind FR 2420, Report of Chosen Cash Market Charges; authors’ calculations.

Be aware: The chart exhibits quarterly common federal funds quantity by borrower sort from the fourth quarter of 2015 by the third quarter of 2023.

Not like home banks, nonetheless, most FBO branches should not insured by the Federal Deposit Insurance coverage Company (FDIC) after amendments to the Worldwide Banking Act disallowed new branches of FBOs from acquiring deposit insurance coverage. This regulatory distinction has two vital implications for why FBO branches borrow within the fed funds market: First, it limits their entry to deposits—the principle supply of home financial institution funding—making fed funds an vital supply of their short-term funding. Second, since they don’t pay the FDIC evaluation payment, most FBO branches face an efficient price of borrowing fed funds that’s decrease than that of home banks. Decrease funding prices give FBO branches a bonus over their home counterparts in arbitraging fed funds supplied at charges beneath the curiosity on reserve balances (IORB) charge, as they will successfully earn a bigger unfold by borrowing fed funds and depositing the borrowed funds on the Fed. Moreover, variations in regulatory necessities throughout jurisdictions make partaking within the arbitrage commerce more cost effective and fewer capital intensive for FBO branches. Particularly, leverage ratios in overseas jurisdictions are sometimes calculated as a period-end snapshot, versus each day or weekly averages within the U.S., which permits FBO branches extra flexibility to borrow between reporting dates and easily unwind their positions on month-end or quarter-end dates to take care of larger reported leverage ratios.

The chart above exhibits that home banks are additionally debtors within the fed funds market. Borrowing by home banks ranged from $2.5 billion in late 2021 to $25 billion in mid-2019, representing between 5 and 35 p.c, respectively, of the full each day quantity of fed funds traded.

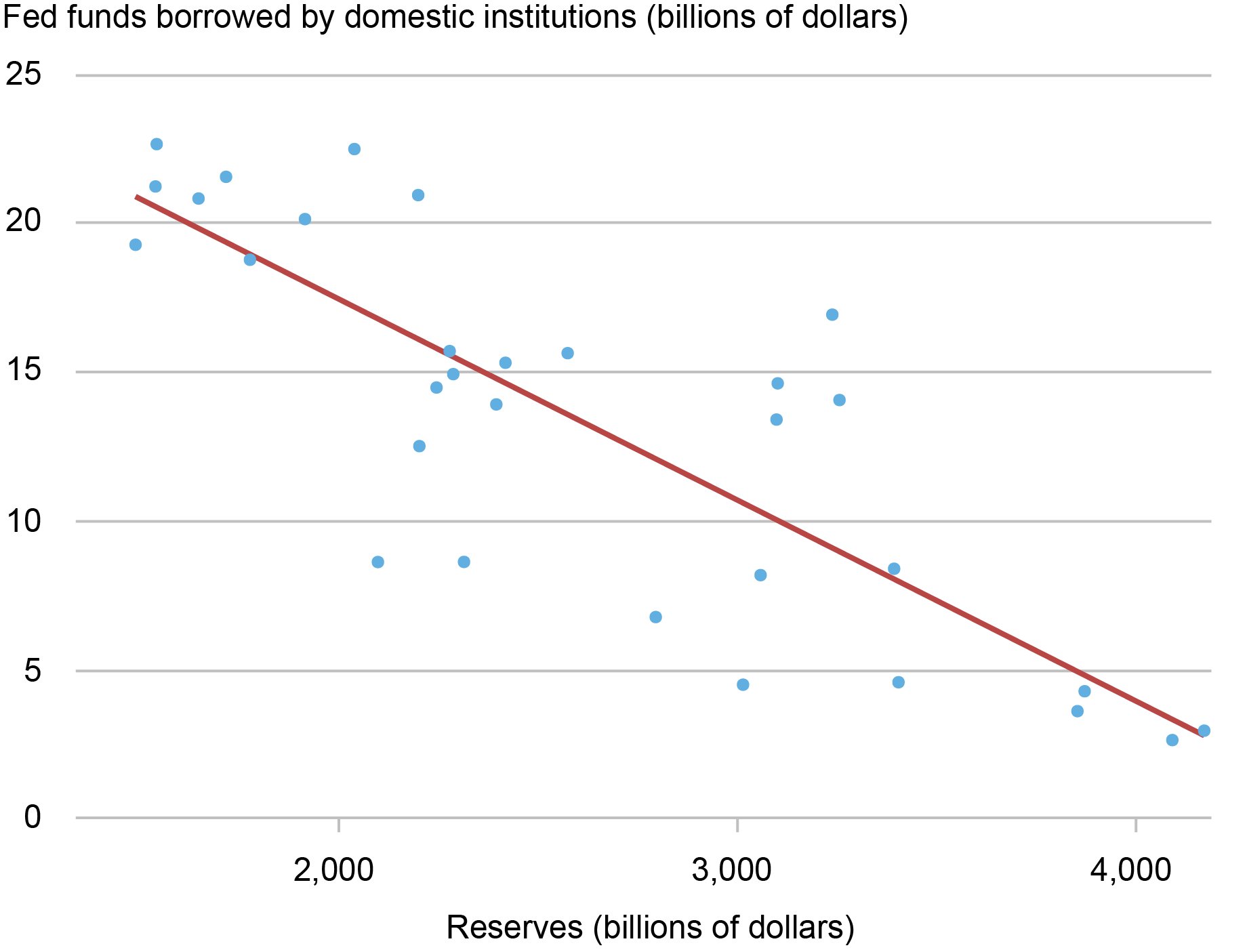

As proven within the subsequent chart, their borrowing will increase when combination reserves decline. This discovering is in line with outcomes from the November 2022 Senior Monetary Officer Survey (SFOS), the place greater than 70 p.c of home banks responded that they have been possible or very prone to borrow in unsecured funding markets—together with the fed funds market—as a technique to construct liquidity if their degree of reserve balances have been to fall beneath a minimal threshold (see this abstract of the SFOS outcomes).

Fed Funds Borrowing Will increase as Mixture Reserves Decline

Sources: Federal Reserve Financial institution of St. Louis, FRED database; authors’ calculations.

Be aware: Reserves figures are quarterly averages.

Who’s Lending within the Fed Funds Market?

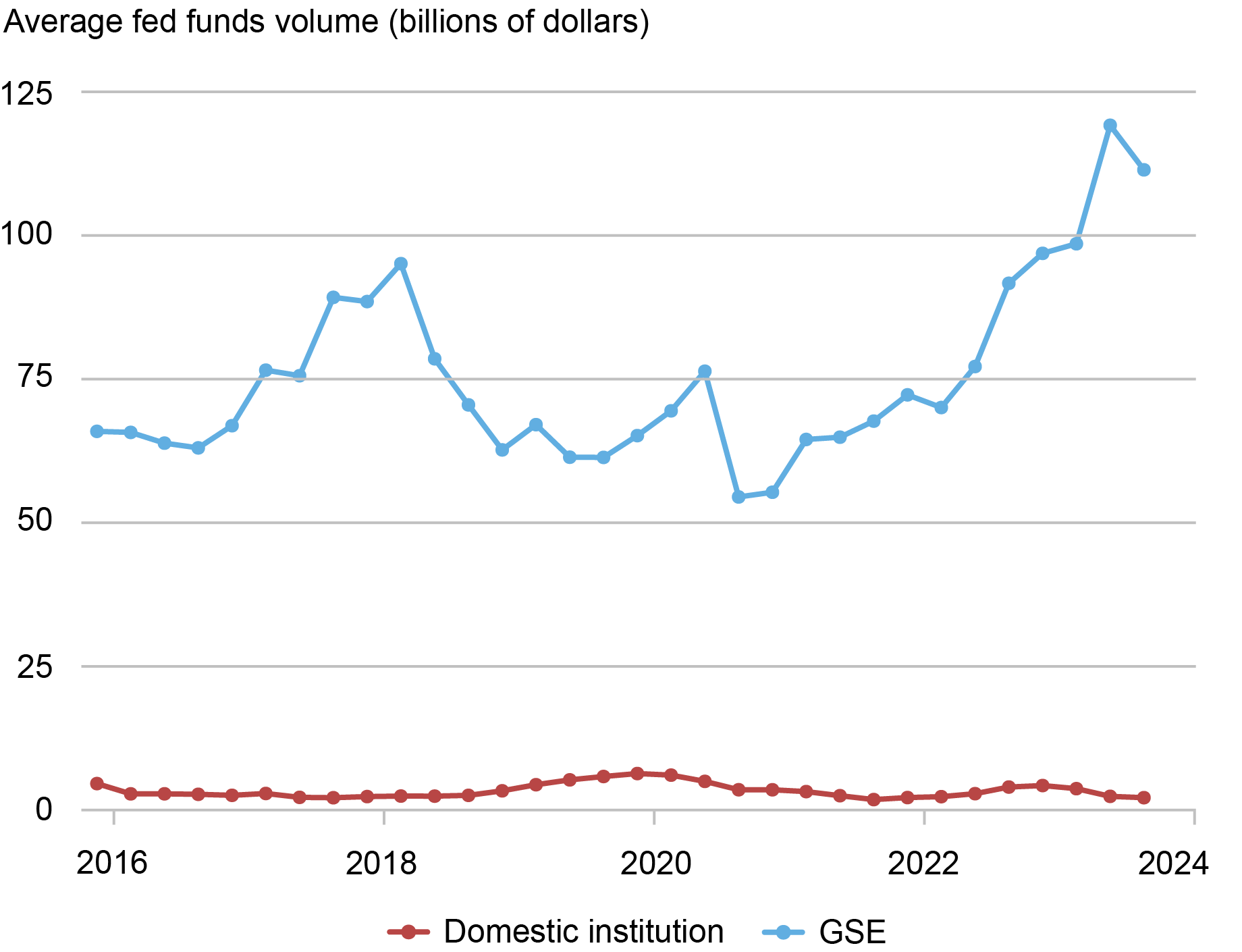

Federal House Mortgage Banks (FHLBs) are the highest lenders within the fed funds market. The FHLBs are GSEs that help mortgage lending and group investments and are organized as cooperatives owned by their members. The eleven FHLBs elevate funds in international markets by the sale of debt securities that they then lend to their members by collateralized loans (referred to as “advances”), which signify round two-thirds of their complete belongings (see the FHLB monetary studies). As the subsequent chart exhibits, GSEs dominate lending within the fed funds market and are liable for greater than 90 p.c of the full each day quantity of fed funds traded.

FHLBs Are the Important Lenders within the Fed Funds Market

Sources: Federal Reserve Kind FR 2420, Report of Chosen Cash Market Charges; authors’ calculations.

Be aware: The chart exhibits quarterly common federal funds quantity by lender sort from the fourth quarter of 2015 by the third quarter of 2023.

Two main elements contribute to FHLBs’ willingness to lend within the fed funds market. First, FHLBs should maintain liquidity portfolios—partly to satisfy minimal regulatory necessities, but in addition to fulfill advances to their members. Fed funds are key devices in such portfolios, together with interest-bearing deposit accounts and different chosen short-term investments reminiscent of reverse repos. Which means that FHLBs flip to the fed funds market to speculate extra money holdings. Second, not like home banks and FBO branches, FHLBs don’t earn curiosity on their balances on the central financial institution, which creates an incentive for them to lend at charges beneath the IORB charge. In flip, this incentive to lend at low charges triggers the arbitrage mechanism between fed funds charges and the IORB charge, making it an everyday phenomenon somewhat than an anomaly.

Two extra factors are noteworthy right here. First, since FHLBs have entry to the in a single day reverse repo (ON RRP) facility that the Fed launched in 2013, they’re unwilling to lend at charges beneath the ON RRP charge. Second, since FHLBs face counterparty credit score limits, the mixture quantity lent to a single counterparty is usually restricted (see right here for particulars on these limits), which favors {that a} nontrivial arbitrage unfold often prevails.

The chart above exhibits that home depository establishments additionally lend within the fed funds market, however at very small volumes. This is because of their means to earn the IORB charge, which disincentivizes them from lending reserves within the fed funds market when the clearing charge is beneath IORB.

Wrapping Up

The fed funds market has modified dramatically since 2008: The Fed expanded its stability sheet to help the U.S. economic system, leading to reserves within the banking system growing considerably, and it additionally started paying curiosity on these reserve balances. Each day quantity within the fed funds market has decreased considerably and market dynamics have developed to seize arbitrage exercise between FHLBs and branches of overseas banks.

Gara Afonso is the top of Banking Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Gonzalo Cisternas is a monetary analysis advisor in Non-Financial institution Monetary Establishment Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Brian Gowen is a capital markets buying and selling principal within the Federal Reserve Financial institution of New York’s Markets Group.

Jason Miu is a capital markets buying and selling affiliate director within the Federal Reserve Financial institution of New York’s Markets Group.

Joshua Youthful is a coverage and market evaluation advisor within the Federal Reserve Financial institution of New York’s Markets Group.

The right way to cite this put up:

Gara Afonso, Gonzalo Cisternas, Brian Gowen, Jason Miu, and Joshua Youthful, “Who’s Borrowing and Lending within the Fed Funds Market Right this moment?,” Federal Reserve Financial institution of New York Liberty Avenue Economics, October 10, 2023, https://libertystreeteconomics.newyorkfed.org/2023/10/whos-borrowing-and-lending-in-the-fed-funds-market-today/.

Disclaimer

The views expressed on this put up are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the writer(s).