{kind=link}

As an employer, you may provide numerous advantages to your staff. There are pre-tax and post-tax advantages for workers to get pleasure from. One plan you may provide staff is a well being, or medical, FSA. So, what’s an FSA?

What’s an FSA?

An FSA, also called a versatile spending account (or association), is a tax-free fund that staff can contribute to and use on qualifying prices. There may be an annual IRS contribution restrict on FSAs.

There are a couple of forms of FSAs, together with:

- Well being FSAs: Staff can use funds on qualifying medical and well being care bills (e.g., prescriptions).

- Dependent care FSAs: Staff can use funds for qualifying dependent care companies (e.g., daycare).

FSAs are voluntary advantages you may provide in your small business. Likewise, staff can select to contribute to an FSA plan. It’s essential to set up an FSA at your small business for workers to open accounts. Self-employed people are usually not eligible to have an account, and extremely compensated worker restrictions additionally exist. An FSA is a qualifying profit underneath a Part 125 plan, or cafeteria plan.

Well being FSAs are the commonest sort of versatile spending association. You may provide FSA plans to staff as a standalone profit or along side conventional medical insurance or high-deductible well being plans. However, well being FSAs aren’t the one sort of financial savings accounts staff can use for well being and medical bills. You may additionally contemplate organising an HSA (well being financial savings account).

Well being FSA Q&A

Concerned about providing staff a versatile spending account? Learn on to find out about qualifying bills, 2024 FSA contribution limits, and extra.

What can staff use FSA plans on?

It’s essential to specify qualifying medical bills within the FSA plan you determine. Staff will pay for qualifying medical and dental bills with their FSA funds.

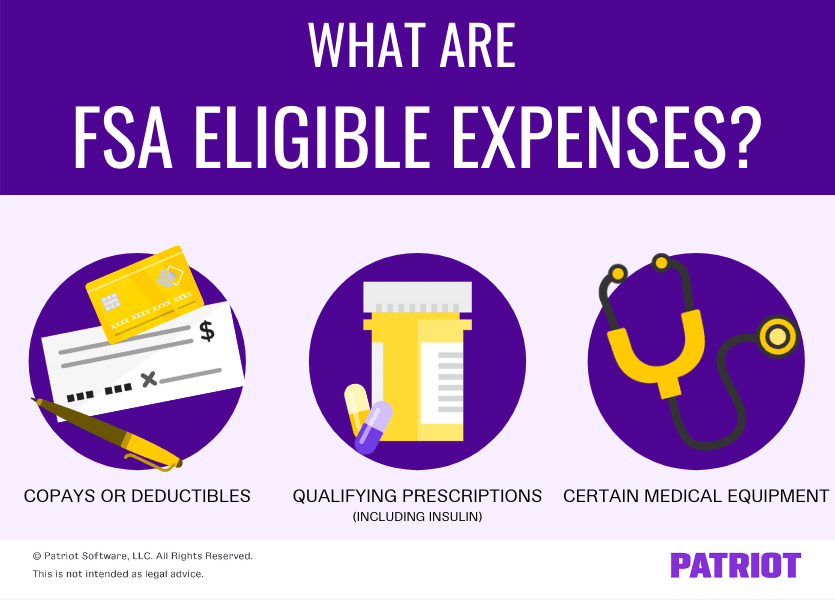

FSA eligible bills embrace the next:

- Copays or deductibles

- Qualifying prescriptions

- Sure medical gear

Totally different procedures or conditions that allow staff use their funds embrace an ambulance, bodily examination, psychologist, or operation.

Medicines or medicine qualify as medical bills in the event that they require a prescription, are over-the-counter medicines which can be prescribed, or are insulin.

FSA-eligible objects additionally embrace issues like bandages, crutches, or synthetic enamel.

The worker, their partner, dependents, or little one underneath the age of 27 can incur medical bills.

For a full listing of qualifying medical bills, seek the advice of the IRS’s Publication 502.

Heads up! Insurance coverage premiums don’t depend as FSA qualifying bills.

Does the employer must contribute?

You may select to contribute to an worker’s FSA plan. Employer contributions are usually not obligatory.

In case you do contribute, don’t embrace employer FSA contributions within the worker’s gross earnings.

FSA contribution limits for 2024

Every year, the contribution restrict for an FSA plan modifications. For 2024, staff can contribute as much as $3,200 per yr to their account, up from the 2023 restrict of $3,050.

Are FSA plans taxable?

Contributions to FSA plans are made on a pre-tax foundation. Pre-tax contributions imply you’re taking cash out of worker wages earlier than withholding taxes. This reduces the worker’s tax legal responsibility.

For instance, an worker earns $1,200 with every paycheck. They contribute $35 to their FSA plan. The worker’s taxable wages are solely $1,165 ($1,200 – $35).

When does an worker decide their contribution quantity?

The worker determines how a lot to contribute to the account in the beginning of the yr. It’s essential to withhold their contribution quantity from their wages every pay interval for his or her FSA plan.

If the worker has a qualifying life occasion (e.g., marriage, divorce, start of a kid), they will change their contribution quantity in the course of the yr. In any other case, they’re usually caught with the quantity they determined in the beginning of the yr.

Make FSA deductions a snap with Patriot Payroll

From correct calculations to computerized tax updates, it’s time to see what Patriot’s award-winning software program can do for your small business.

When does an worker have entry to funds?

The worker has entry to the total quantity they plan on contributing immediately, no matter whether or not or not they’ve contributed that quantity.

For instance, an worker decides to contribute $2,000 to their versatile spending account all year long. It’s February, and the worker wants $500 from their FSA plan. Thus far, you’ve solely withheld $80 from their wages for the account. Nonetheless, the worker has full entry to the $2,000. So, they will take $500 to cowl their expense (hooray!).

How do staff obtain distributions from their account?

Staff can sometimes both use an FSA debit card to pay for qualifying bills or obtain reimbursements for eligible prices.

Can staff carry cash over?

For probably the most half, the cash in an FSA plan is forfeited again to your organization when the yr ends. Nonetheless, there are two optionally available FSA carryover guidelines you may select from to supply staff:

- Grace interval: Your FSA plan can provide a 2.5-month grace interval after the plan yr. The worker can use the funds if they’ve medical bills inside the grace interval. After the two.5 months finish, the worker loses the remaining steadiness, and the FSA forfeiture goes to your small business.

- Carryover: You may embrace a carryover situation that lets staff add as much as $640 of unused funds to the subsequent yr’s plan ($640 is the 2024 restrict; $610 is the 2023 restrict). You determine the carryover restrict. Any quantity over the carryover restrict is forfeited to your small business.

Are there reporting necessities?

Staff don’t have to report FSA contributions or distributions on their tax returns. This differs from an HSA or Archer MSA, which requires the worker to report the contributions on Kind 1040.

For extra info on FSA plans, seek the advice of the IRS’s Publication 969.

Advantages of an FSA

So, what’s the massive deal about establishing a medical FSA plan in your small business? By an FSA, you may:

- Get pleasure from tax financial savings

- Appeal to candidates to use

- Improve job retention

Having an FSA can present a tax profit to each you and your staff. Staff scale back their federal earnings tax and FICA (Social Safety and Medicare) tax legal responsibility. Hooray for them, and hooray for you, too. FICA tax consists of worker and matching employer parts. As a result of an FSA plan reduces the worker’s taxable wages, you and the worker pay much less in FICA taxes. However, remember that worker FSA contributions should be topic to state and native earnings tax withholding, if relevant.

Small enterprise worker advantages are vital to many staff, attracting candidates to a job and bettering retention charges.

Need a greater methodology to maintain observe of payroll particulars on your staff? Patriot’s on-line payroll software program affords a straightforward approach to withhold taxes, advantages, and different deductions from worker wages. And, we provide free setup and help. Get your free trial as we speak!

This text has been up to date from its unique publish date of September 28, 2011.

This isn’t meant as authorized recommendation; for extra info, please click on right here.