{kind=link}

This put up makes use of the New York Fed DSGE mannequin to ask the query: What would have occurred to rates of interest, output, and inflation had the Federal Reserve been following a median inflation focusing on (AIT)-type response operate since 2021:Q2, when inflation started to rise—versus retaining the federal funds fee on the zero decrease certain (ZLB) till March 2022, after which elevating it aggressively thereafter? We present that precise coverage was extra accommodative in 2021 than implied by the AIT response operate after which extra contractionary in 2022 and past. On web, the lagged impact of financial coverage on the extent of GDP, when measured relative to the counterfactual, has been constructive all through the forecast horizon, as a result of preliminary enhance related to retaining the fed funds fee close to zero in 2021.

A Counterfactual: What If the Fed Had Caught to the AIT Rule?

The AIT response operate assumed all through this train is according to the 2020 financial coverage framework assessment. The parameters of the AIT rule—particularly its response to inflation and output “misses,” and its inertia (the coefficient on lagged rates of interest)—had been calibrated as of 2020:Q3 to be able to match the anticipated length of the zero decrease certain (ZLB) given the financial situations in the course of the COVID pandemic (see right here for extra particulars).

Our goal right here is to make use of our DSGE mannequin to simulate how the economic system would have carried out if the financial coverage fee had not deviated from the AIT response operate beginning in 2021:Q2. The train could be described as follows: What would have occurred to the economic system had the FOMC adopted the response operate that rationalized the September 2020 pledge to maintain charges on the ZLB for an prolonged interval given expectations at the moment, and subsequently deviated from the ZLB pledge—in accordance with the AIT rule—when inflation strayed away from this anticipated path beginning in 2021:Q2? The outcomes of this counterfactual experiment must be taken with a grain of salt, after all, as they’re solely nearly as good because the mannequin that produces them.

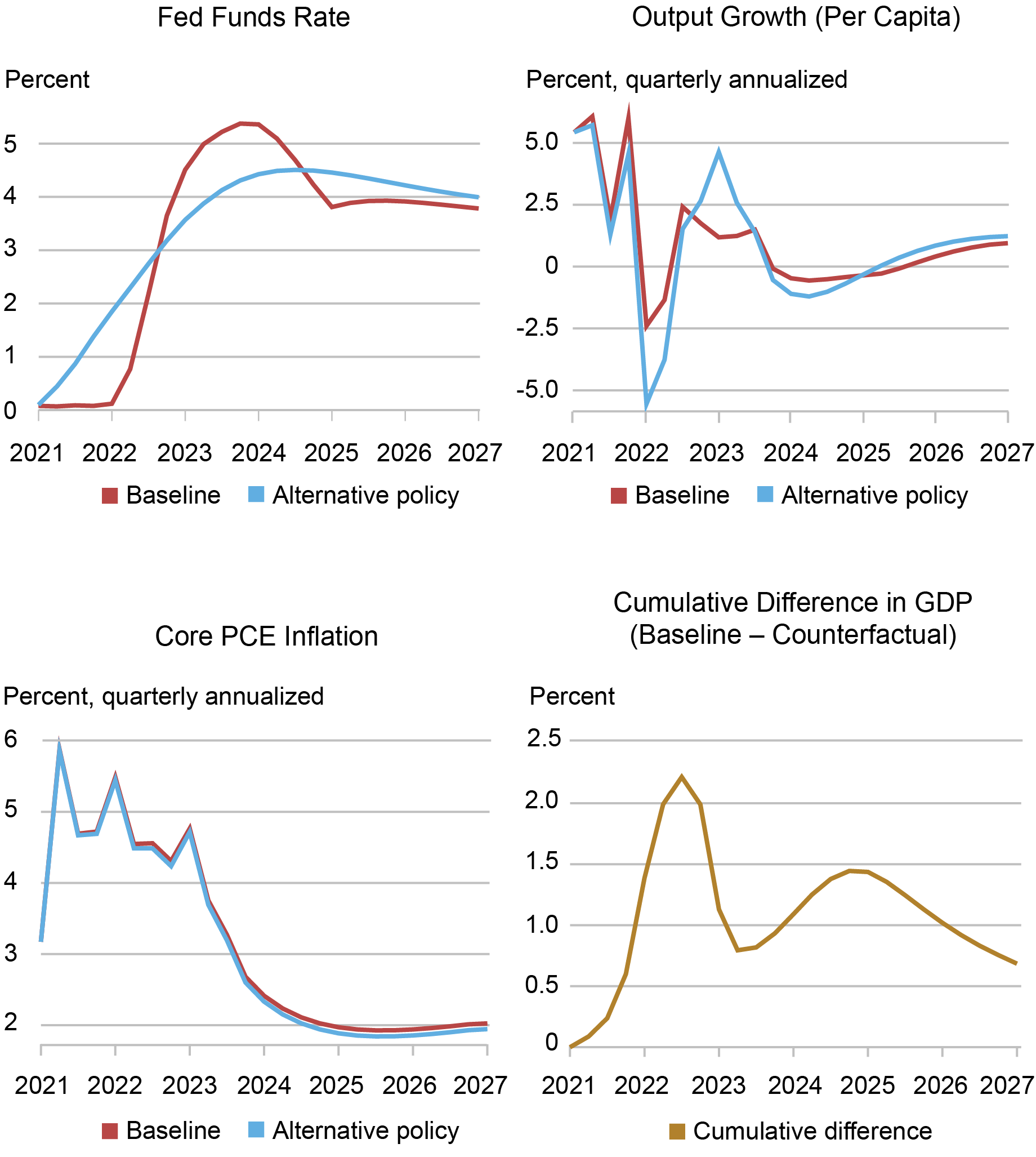

The higher left panel within the chart under exhibits the precise path of the fed funds fee (FFR) and the present baseline forecast after 2023:Q2 (crimson) versus the counterfactual path had the FOMC adopted the AIT rule beginning in 2021:Q2 (blue). The counterfactual path for all of the variables is constructed by subjecting the counterfactual economic system to the identical shocks that, in accordance with the mannequin, have hit the precise economic system, with the one distinction between the 2 economies being the financial coverage pursued by the FOMC. So, as an example, the cost-push shocks which can be the principle trigger for the burst in inflation (backside left panel) in 2021 within the mannequin (see this put up) additionally have an effect on inflation within the counterfactual economic system. Equally, beneath the baseline path, we see progress rebounding within the second half of 2022 and 2023—a rebound that was as a result of robust demand (see this put up), according to the BVAR evaluation in our accompanying put up. These very shocks have an effect on the trail within the counterfactual economic system as nicely.

Counterfactual with AIT Response Perform Beginning in 2021:Q2

Supply: Authors’ calculations.

Had the FOMC adopted the AIT response operate beginning in 2021:Q2, charges would have risen instantly. The counterfactual FFR path then falls under the precise FFR path in the course of final yr, stays decrease than the baseline path by means of mid-2024, after which finally converges from above to the precise forecasted path for rates of interest. Had the FOMC pursued this coverage, per capita output progress (quarterly annualized, higher proper panel) would have been decrease in 2022 and better in 2023. The decrease output progress in 2022 is the results of tightening in 2021, whereas the stronger progress this yr originates from the much less aggressive tempo of tightening in 2022 and 2023.

The underside proper panel exhibits that deviations from the AIT rule have been expansionary on web. The panel exhibits the hole in output ranges that developed beginning in 2021:Q2 between the baseline and the choice path. The counterfactual degree of output is under the precise degree and the hole between the 2 rises to a peak of about 2 p.c in mid-2022, adopted by a narrowing in 2023 brought on by the extra aggressive tempo of tightening beneath precise coverage in that yr. The hole then briefly widens once more in 2024-25 as precise coverage eases sooner than the AIT rule. On web, the lagged impact of financial coverage on financial exercise, when measured relative to a counterfactual the place coverage follows the AIT rule, has been constructive all through the forecast horizon, as a result of preliminary enhance related to retaining the FFR at close to zero in 2021.

The decrease left panel exhibits that inflation charges don’t differ considerably between the 2 coverage guidelines. That is partially as a result of the mannequin has a weak connection between output and inflation due to its flat Phillips curve. Partially it’s because within the New York Fed DSGE forecasts we now have been assuming that brokers within the mannequin have been solely partially conscious of the change within the coverage framework from inflation focusing on to AIT, with a weight that will increase over time. In all different simulations to this point, we now have continued to take care of this assumption: when adopting another coverage, the central financial institution was not affecting the way in which “unaware” brokers kind expectations, implying that the weakening of the economic system proven within the decrease proper panel isn’t internalized by companies when setting costs.

Specializing in the Mountain climbing Interval

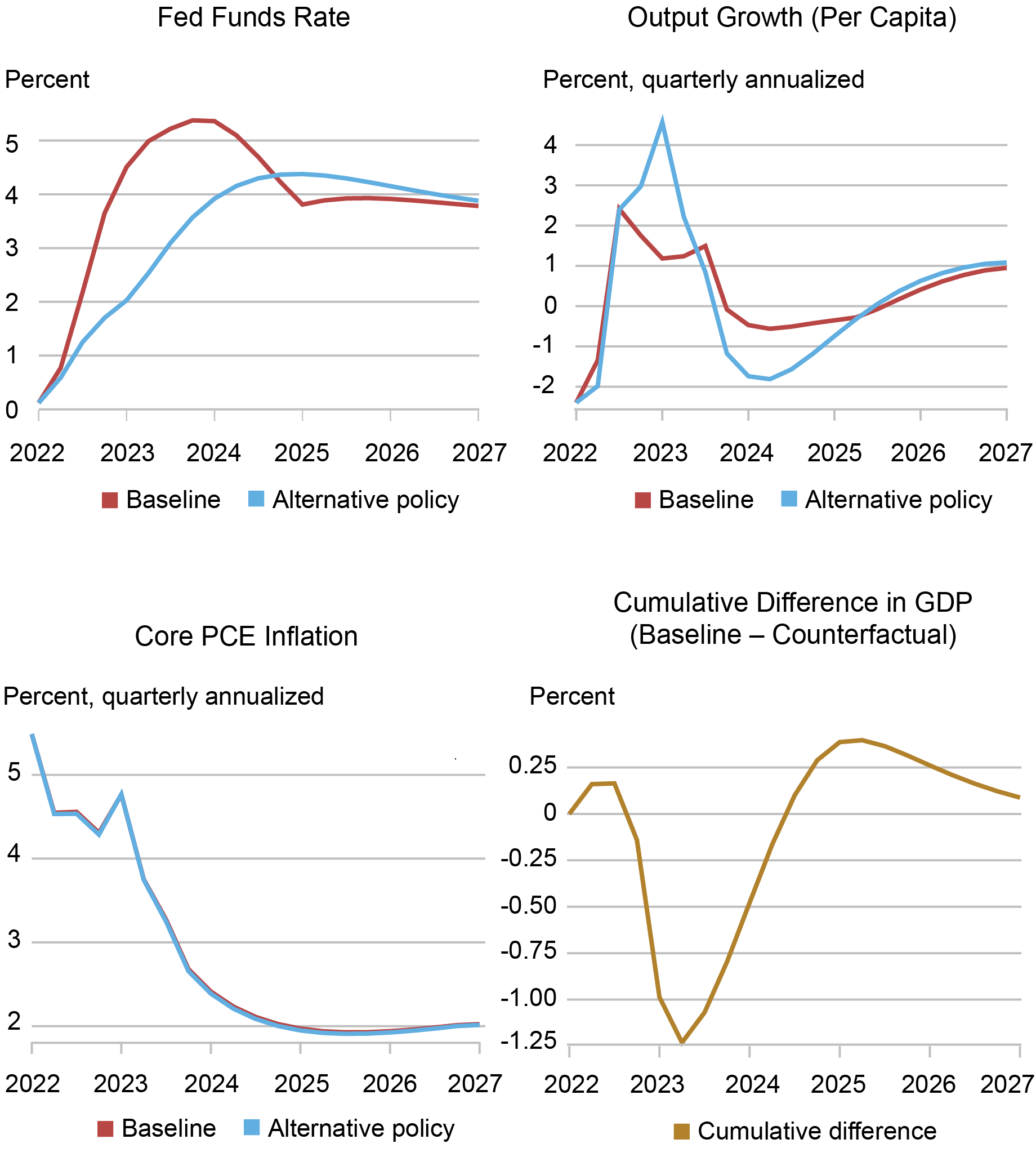

The chart under abstracts from the 2021 ZLB coverage and isolates the impact of the aggressive tightening in 2022 and 2023. That’s, the DSGE mannequin simulation now begins in 2022:Q2. The chart exhibits that the tempo of tightening in 2022 and early 2023 was extra aggressive than implied by the AIT response operate, even contemplating the big constructive common inflation miss accrued within the earlier quarters. The mannequin permits for each contemporaneous in addition to anticipated coverage shocks. The previous are deviations from the AIT response operate that happen within the quarter through which they’re introduced. The latter are shocks to anticipated future charges–in different phrases, ahead steerage shocks. Within the estimation, these anticipated shocks are recognized utilizing FFR expectations obtained in every quarter from the newest Survey of Major Sellers. In response to the mannequin, there have been two giant contractionary shocks of about 100 foundation factors, each contemporaneous, in 2022:This fall and 2023:Q1. Ahead steerage shocks didn’t play a significant function within the climbing interval, apart from a 50-basis level expansionary six-quarter-ahead anticipated shock in 2023:Q2, which explains why the baseline FFR path falls under the AIT-implied path after mid-2024. The truth that most deviations from the response operate are as a result of contemporaneous shocks implies that the aggressive climbing cycle had not been anticipated by the general public, probably limiting its results on the economic system.

Counterfactual with AIT Response Perform Beginning in 2022:Q2

Supply: Authors’ calculations.

The impact of those coverage shocks on financial exercise has been restrictive, with their cumulative impact peaking in mid-2023 with the precise degree of output being about 1.25 p.c under the AIT counterfactual. The hole then narrows sharply from late 2023 and thru 2024 because the AIT coverage pushes charges greater over this era whereas the anticipated baseline path has the coverage fee falling. Be aware that the projected slowdown in progress in late 2023 and 2024 that takes place beneath the baseline projection is not as a result of lagged results of the speed hikes in 2022 and 2023. With out these fee hikes the slowdown can be much more pronounced, just because their peak impact on the degree of exercise has already been reached and so their contribution to progress is definitely constructive, at the least in accordance with the mannequin.

To conclude, on this put up we requested what would have occurred had the Fed adopted an AIT response operate beginning in 2021:Q2. We present that relative to this counterfactual, precise coverage was accommodative in 2021 after which contractionary in 2022 and thereafter, and that the mixed impact on financial exercise of those deviations from the AIT response operate has been expansionary and stays so in accordance with the mannequin.

Richard Okay. Crump is a monetary analysis advisor in Macrofinance Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Marco Del Negro is an financial analysis advisor in Macroeconomic and Financial Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Keshav Dogra is a senior economist and financial analysis advisor in Macroeconomic and Financial Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Pranay Gundam is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Donggyu Lee is a analysis economist in Macroeconomic and Financial Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Ramya Nallamotu is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Brian Pacula is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Methods to cite this put up:

Richard Crump, Marco Del Negro, Keshav Dogra, Pranay Gundam, Donggyu Lee, Ramya Nallamotu, and Brian Pacula, “The New York Fed DSGE Mannequin Perspective on the Lagged Impact of Financial Coverage,” Federal Reserve Financial institution of New York Liberty Avenue Economics, November 21, 2023, https://libertystreeteconomics.newyorkfed.org/2023/11/the-new-york-fed-dsge-model-perspective-on-the-lagged-effect-of-monetary-policy/.

Disclaimer

The views expressed on this put up are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the writer(s).