{kind=link}

Who now remembers Lengthy-Time period Capital Administration, the failure of genius, the value of hubris, and the lesson that the innocents bear the price of their elders’ folly?

Too few, judging from investor habits.

The collapse of LTCM was the primary of three world monetary crises over the previous 25 years that erupted primarily within the developed world, however whose penalties had been primarily borne by rising markets economies and buyers.

Supply: James Watson, English printmaker, 1767, authentic within the Rijksmuseum

The world’s smaller and fewer liquid inventory markets eternally appear without end to current tomorrow’s greatest funding alternatives. As Little Orphan Annie sings, “I like you, tomorrow, You’re at all times a day away.” As they’ve matured, monetary transparency has improved, shareholder rights are more and more revered, and company choices are drifting within the course of rational capital allocation moderately than relational (“who ”) allocation.

It’s a lot the identical ardour (or delusion) that drives buyers in microcap shares all over the place.

We are going to share a fast recap of the Three Nice Storms, then spotlight the destiny of the EM funds that survived all three. There’s truly some excellent news about choosing a fund which may survive the storms forward.

The Three Nice Storms

For many of the 20th century, the world’s smallest and least liquid inventory markets had been tormented by repeated crises. A few of these crises had been of their very own doing, as unreliable authorities buildings and self-serving company ones conspired to undermine belief. Many, nonetheless, weren’t their doing. Markets with very low liquidity -relatively few patrons or sellers, comparatively low buying and selling quantity, comparatively low market capitalization – are hostage to the behaviors of some, massive buyers. If one massive investor in a single small market makes an attempt to withdraw out of the blue, a market panic follows. If a number of massive buyers depart, a complete area is in danger.

So “market runs” had been routine. Three occasions, nonetheless, stand in stark distinction to “regular” panics.

1998: Lengthy Time period Capital Administration collapse 25 years in the past

Lengthy-Time period Capital Administration was a large hedge fund with a stellar file and “A” tier buyers, together with Nobel Prize-winning economists Myron Scholes and Robert Merton, main banks, and sovereign wealth funds.

Lengthy-Time period Capital Administration was a large hedge fund with a stellar file and “A” tier buyers, together with Nobel Prize-winning economists Myron Scholes and Robert Merton, main banks, and sovereign wealth funds.

LTCM had positioned leveraged bets on the Russian forex, but in addition thought they’d adequately hedged these bets. They had been improper. Within the spring and summer season of 1998, the federal government of Boris Yeltsin was in turmoil. President Yeltsin fired his complete cupboard in March and appointed “take cost” guys to key posts. Quick-term authorities rates of interest popped to 150%. On August 17, Russia declared it was devaluing its forex. For good measure, it additionally defaulted on its bonds.

The Dow dropped 13% in two weeks as buyers fled shares, rates of interest fell in response, and LTCM’s extremely leveraged investments crumbled. The fund misplaced 50% in two weeks, threatening to bankrupt the banks, wealth, and pension funds that had invested so closely in it. Bear Stearns demanded $500 million from the fund.

Dangerous issues adopted:

- Rising markets acquired crushed. “[T]he MSCI Rising Markets index shed 56%, as buyers pulled billions of {dollars} out of growing economies. As of early December, buyers eliminated all however $500 million of the $40.8 billion they dedicated in 2007 to the rising markets funds tracked weekly by EPFR World.” (Polya Lesova, “Rising markets: the perfect and the worst of 2008,” MarketWatch, 12/18/2008)

- The federal government stepped in to save lots of LTCM’s buyers. Buffett provided LTCM pennies on the greenback for his or her property. The Fed stepped in to dealer a greater deal partially to save lots of the establishments put in danger by their very own stupidity. The establishments concerned remembered.

2008: The World Monetary Disaster 15 years in the past

The 2008 disaster was years within the making. The shortest model is that the Fed responded to the collapse of the inventory market bubble in 2000 and the assaults of 9/11/2001 by pushing rates of interest down from 6.5% (in 2000) to 1% (in 2003). “Free cash” routinely results in unhealthy choices. Individuals snapped up properties, costs soared, and monetary establishments determined that mortgages – even mortgages held by individuals with no credit score historical past and no dependable revenue – had been nice investments. They only wanted to “securitize” baskets of iffy loans in a means that … by some means, canceled out all of their dangers.

Till they didn’t. In 2007, firms making subprime loans began submitting for chapter. By mid-year, hedge funds that had invested within the loans collapsed. That summer season, the worldwide lending system froze up, and, in September, Lehman Brothers turned the most important chapter in American historical past. Buyers out of the blue found they had been holding trillions in near-worthless subprime mortgages.

The worst disaster in 80 years rapidly erupted. Dangerous issues adopted:

- Rising markets acquired crushed. Through the disaster (Nov 2007 – Feb 2009), the common EM fund misplaced 52% per 12 months with a max drawdown of 62%. Rising Europe and Russia had been reserving losses of 65% per 12 months. Within the following 15 years, the group returned 2.3% with an ordinary deviation of twenty-two.3%.

- The federal government stepped in to save lots of the worldwide monetary system. And in addition the morons behind the mess. The Feds minimize rates of interest to zero, opened emergency lending amenities, and purchased securities on the open market to supply liquidity and foster calm. By the Feds’ personal calculation, “Federal Reserve bought $300 billion of Treasury securities, about $175 billion of company debt obligations, and $1.25 trillion of company mortgage-backed securities.” The establishments concerned remembered.

2020: The World Pandemic, three years in the past

You already know this story.

And its takeaway:

- Rising markets acquired crushed. Because the begin of COVID, the common EM has misplaced 1.3% yearly. The median fund is down by -0.7% and has gifted buyers with a 39% drawdown. Which is “much less crushed” than traditional, however annualized losses even after a ferocious rebound – frontier EM funds are up 13.6% YTD, EM funds up 6.2% YTD by September 2023 – is not excellent news.

- The federal government stepped in to save lots of the monetary system. Placing apart all the heroic work to really management the pandemic, the Feds but once more slashed charges to zero, and the opposite branches added trillions in stimulus (a few of which was even a good suggestion). Each actions are complicit within the subsequent spike in inflation and the subsequent-subsequent rate of interest spike.

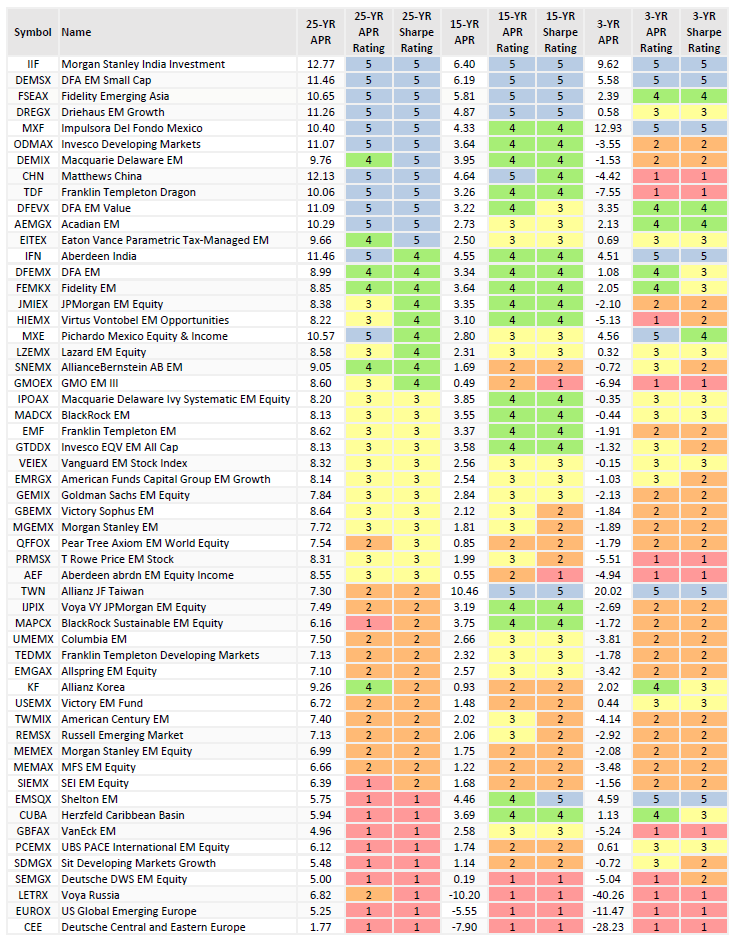

Charting the survivors: EM Fund efficiency by three crises

In assessing the flexibility of funds to climate repeated storms, we began by isolating all EM funds with a file of 25 years or extra. We then checked out three metrics:

- Absolute returns for the reason that inception of every storm. That interprets to their 25-year (LTCM and past), 15-year (GFC and past), and 3-year (Covid and past, we hope) information

- Relative whole returns. Funds with returns within the prime 20% of their peer teams are proven with a blue field, inexperienced is the subsequent 20%, and yellow is the center 20%. Orange and crimson are, nicely, unhealthy.

- Relative risk-adjusted returns. The identical system applies: blue/inexperienced/yellow for the highest three packing containers.

The whole dataset is beneath. We’ll supply two takeaways:

-

-

Robust previous efficiency predicts affordable future efficiency. None of the 1998 standouts sagged in 2008. Few of the 1998 standouts sagged within the Covid period. Two of the highest 20 funds in 1998 are noticeably sub-par now, whereas two extra are beneath common.

The caveat: we will’t management for survivorship bias. If a 1998 champion subsequently burst into flames, we wouldn’t have a file of it.

-

Wretched previous efficiency predicts ongoing distress. Dangerous appears to beget unhealthy. Of the underside 20 funds in 1998, just one has made a leap to the highest tier. Virtually all the others stay mired within the land of orange (beneath common) and crimson (a lot beneath common) whole and risk-adjusted returns.

The one outlier is Shelton Rising Markets (fka Icon Rising Markets). Shelton acquired the flailing Icon fund in June 2020. Two generations of Shelton managers have reworked it right into a four-star (Investor shares) or five-star (Institutional shares) fund. Over the previous three years, it has returned 7.8% yearly whereas its common peer has misplaced cash.

-

About 60 rising markets funds have survived the previous quarter of a century. A handful of funds have carried out solidly by one disaster after the subsequent. They’re:

- Morgan Stanley India

- DFA EM Small Cap

- Constancy Rising Asia

- Driehaus EM Progress

- Impulsora Del Fondo Mexico

- DFA EM Worth

- Acadian EM

- Eaton Vance Parametric Tax-Managed EM

- Aberdeen India

- DFA EM

- Constancy EM

- JPMorgan EM Fairness

- Virtus Vontobel EM Alternatives

- Pichardo Mexico Fairness & Earnings

- Lazard EM Fairness

Of the 15 funds which have remained constantly above common, ten are geographically diversified, and 5 are narrowly targeted, which introduces an entire separate set of dangers.

The whole roster of EM fairness funds with a file of 25+ years

Funds are ranked by relative Sharpe ratio over 25-, 15-, and 3-year durations