{kind=link}

That are the Prime 10 Greatest SIP Mutual Funds To Make investments In India In 2024? Find out how to choose them and easy methods to create a portfolio? Do we have to change funds yearly? Allow us to attempt to reply all these questions on this submit.

If you’re acquainted with my weblog, you then seen that yearly I publish my record of funds. Final 12 months I didn’t publish the info for sure causes. A lot of of weblog readers requested and I used to be unable to publish. Saying sorry to all my weblog readers for this delay from my aspect. It’s all on account of my Payment-Solely Monetary Planning Service work. If you’re all in favour of availing of this Mounted Payment-Solely Monetary Planning Service, then you’ll be able to confer with the Service web page of this weblog (Mounted Payment-Solely Monetary Planning Service).

For that reason, I assumed to publish this routine submit effectively upfront for 2024. Allow us to first recap what I’ve really useful in 2022.

Many issues modified in between just like the taxation of debt mutual funds or the launch of tax-saver index funds. Should you bear in mind, because the SEBI’s Recategorization Of Mutual Funds, I began to suggest Index Funds majorly.

By adopting the Index Funds, you’re really operating away from trying to find the BEST fund and in addition avoiding the danger of a fund supervisor’s underperformance danger. Investing in an Index Fund and anticipating the returns of the Index is the best approach of funding. The one danger you’ll be able to’t keep away from is market danger, which you must handle by correct asset allocation between debt and fairness (I imply on the portfolio degree).

BY adopting index funds you’re certain of index returns. Nonetheless, whenever you select the energetic funds, the danger of underperformance is all the time there. Take a look at the historical past, you seen that no fund supervisor on this earth can generate CONSISTENT superior returns to index. Few years of outperformance could vanish if there’s a extended underperformance of the fund. Above that because of the excessive price, energetic funds are extra weak to generate low returns than index. This may be validated from the historical past additionally.

“If you’re extremely proficient and very fortunate, you’ll beat the market more often than not. Everyone else can be higher off investing in low-cost broad-market index funds.” – Naved Abdali

Present me one fund supervisor within the historical past of funding who accepted the underperformance overtly or accepted that outperformance is due to LUCK. Even whether it is due to luck, they all the time present us as if the results of their SKILL.

It remembers me of my favourite Daniel Kahneman’s quote from the ebook “Considering, Quick and Sluggish” –

“Mutual funds are run by extremely skilled and hardworking professionals who purchase and promote shares to attain the absolute best outcomes for his or her shoppers. However, the proof from greater than fifty years of analysis is conclusive: for a big majority of fund managers, the number of shares is extra like rolling cube than enjoying poker. Extra importantly, the year-to-year correlation between the outcomes of mutual funds may be very small, barely larger than zero. The profitable funds in any given 12 months are largely fortunate; they’ve an excellent roll of cube. There’s basic settlement amongst researchers that just about all inventory pickers, whether or not they understand it or not – and few of them do – are enjoying a sport of likelihood.”

Subsequently, ought to we blindly soar into Index Funds? The reply is NO. As it’s possible you’ll remember, many AMCs are actually launching a whole lot of Index Funds. As a result of they’re making an attempt to comply with the development. Few launched with an concept of low price and few introduced issues by launching smart-beta funds. Nonetheless, in my opinion, proudly owning the entire market (particularly Nifty 100) is much better than these varied smart-beta index funds. I do know that they could cut back the volatility. Nonetheless, it comes with compensation for returns. Therefore, for simplicity, proudly owning the Nifty 100 is much better. Beware…You don’t want all Index Funds. You want 1-2 funds among the many jungle of Index Funds. It jogs my memory of the quote from John Bogle.

“The profitable method for achievement in investing is proudly owning your entire inventory market by means of an index fund, after which doing nothing. Simply keep the course.”

– John C. Bogle, The Little Guide of Frequent Sense Investing.

For 99.99% of the buyers, the first purpose to decide on the fund is previous returns. John Bogle as soon as stated, “Shopping for funds based mostly purely on their previous efficiency is likely one of the stupidest issues an investor can do.“. They by no means search for even constant returns or the danger concerned within the fund. Therefore, find yourself in having an publicity to the class of funds that aren’t appropriate for them.

Why do we now have to take a position?

For a lot of buyers this fundamental first query is unanswerable. They make investments randomly as a result of they’ve a surplus to take a position. They make investments primarily as a result of to generate larger returns than the Financial institution FDs. They make investments primarily as a result of few of their pals or colleagues are investing in mutual funds.

You could INVEST to achieve your monetary targets however to not generate larger returns. If you chase the returns, you find yourself making extra errors. By no means make investments based mostly in your buddy’s advice. Your monetary life is fully completely different than your mates. Your danger profile is fully completely different than your mates.

Sharing as soon as once more the quote of Morgan Housel.

“If I needed to summarize my views on investing, it’s this: Each investor ought to choose a method that has the best odds of efficiently assembly their targets. And I feel for many buyers, dollar-cost averaging right into a low-cost index fund will present the best odds of long-term success.” – Morgan Housel, The Psychology of Cash (Timeless Classes on Wealth, Greed and Happiness).

I’m not saying that every one the funds will underperform the index. There are ALWAYS few funds that can outperform the Index. Nonetheless, the query mark for you and me is which is CONSISTENTLY outperforming funds throughout OUR funding journey.

The associated fee you pay to them is fastened. Nonetheless, the returns are usually not fastened. If a fund supervisor is claiming that his fund is thrashing the index, then you must verify what’s the precise returns after price and the way persistently he can ship returns.

How To Select The Greatest Index Funds?

If you determine to spend money on Index Funds, you must simply think about three features of the funds and they’re as under.

# Expense Ratio:-Decrease the Expense ratio is healthier for me.

# Monitoring Error:-It’s nothing however how a lot the fund deviated by way of returns with respect to the Index it’s benchmarked. Decrease the monitoring error means higher fund efficiency. Few fund homes don’t publish this information regularly. Therefore, you must be cautious with this information. Consult with my submit on this regard “Monitoring Distinction Vs Monitoring Error Of ETF And Index Funds“.

# AUM:- Increased AUM means a greater benefit for the fund supervisor to handle the liquidity points.

Should you go by these standards, then Index NFOs are additionally not thought of. As soon as they’ve first rate AUM with historic monitoring errors, then you’ll be able to take into account them.

Fundamentals of Investing Mantras

Now earlier than leaping to investing, you will need to have an concept of what are the fundamentals of investing. I repeat this train on a yearly foundation in my weblog submit. However nonetheless, discover the identical kind of questions from the readers. Therefore, to provide the readability, I’m writing as soon as once more.

As per me, earlier than leaping into an funding, one should pay attention to how effectively they’re ready for dealing with monetary emergencies. Monetary emergencies could embrace lack of life, assembly with an accident, hospitalization, sudden earnings loss, or job loss.

Therefore, step one is to cowl your self with correct Life Insurance coverage (Time period Life Insurance coverage the place the protection must be at the very least 15-20 occasions your yearly earnings). You could have your personal medical health insurance (quite than counting on employer-provided medical health insurance). Create higher protection with a household floater plan and Tremendous Prime Up Well being Insurance coverage. Ideally round 3-5 Lakh of household floater plan and round Rs.10-25 Lakh of Tremendous Prime Up is a should these days. Purchase round 15 to twenty occasions of your month-to-month wage corpus as unintended insurance coverage. Then lastly create an emergency fund of at the very least 6-24 months of your month-to-month dedication. This can be useful each time your earnings will cease or should you face any unplanned bills.

As soon as these fundamentals are accomplished, then consider investing. In case your fundamentals are usually not accomplished correctly, then no matter funding constructing you’re creating could tumble at any time limit. Allow us to transfer on and perceive the fundamentals of investing.

You Should Have A Correct Monetary Aim

I seen that many buyers merely spend money on mutual funds simply because they’ve some surplus cash. The second purpose could also be somebody guided that mutual funds are greatest in the long term in comparison with Financial institution FDs, PPF, RDs, and even LIC endowment merchandise.

If in case you have readability like why you’re investing, whenever you want the cash, and the way a lot you want cash at the moment, then you’re going to get higher readability in choosing the product. Therefore, first, determine your monetary targets.

You could know the present price of that purpose. Together with that, you will need to additionally know the inflation charge related to that specific purpose. Do not forget that every monetary purpose has its personal inflation charge. For instance, the training or marriage price of your child’s inflation is completely different than the inflation charge of family bills.

By figuring out the present price, time horizon, and inflation charge of that specific purpose, you’ll be able to simply discover out the longer term price of that purpose. This future price of the purpose is your goal quantity.

I’ve written a separate submit on easy methods to set your monetary targets. Learn the identical at “Monetary Objectives – Find out how to set earlier than leaping into investing?”

Asset Allocation Is a MUST

The following step is to determine the asset allocation. Whether or not it’s a short-term purpose or a long-term purpose, the right asset allocation between debt and fairness is a should. I personally counsel the below-shared asset allocation technique. Do not forget that it could differ from particular person to particular person. Nonetheless, the fundamental concept of asset allocation is to guard your cash and easily sail to achieve your monetary targets.

If the purpose is under 5 years-Don’t contact fairness product. Use the debt merchandise of your selection like FDs, RDs, Liquid Funds, Cash Market Funds, or Extremely Brief Time period Funds.

If the purpose is 5 years to 10 years-Allocate debt: fairness within the ratio of 60:40.

If the purpose is greater than 10 years-Allocate debt: fairness within the ratio of 40:60.

Whereas selecting a debt product, guarantee that the maturity interval of the product should match your monetary targets. For instance, PPF is one of the best debt product. Nonetheless, it should match your monetary targets. If the PPF maturity interval is 13 years and your purpose is 10 years, then you’ll fall in need of assembly your monetary targets.

First fill the debt allocation with EPF, PPF, or SSY (based mostly on the maturity and purpose kind). Should you nonetheless have room to spend money on debt, then select the debt funds. Personally, my selection all the time is to fill these great debt merchandise like EPF, PPF, and SSY.

Return Expectation

Subsequent and the most important step is the return expectation from every asset class. For fairness, you’ll be able to anticipate round 10% to 12% return. For debt, you’ll be able to anticipate round 6% to 7% returns.

When your expectations are outlined, then there’s much less likelihood of deviating or taking knee-jerk reactions to the volatility.

Portfolio Return Expectation

When you perceive how a lot is your return expectation from every asset class, then the subsequent step is to determine the return expectation from the portfolio.

Allow us to say you outlined the asset allocation of debt: fairness as 40:60. Return expectation from debt is 6% and fairness is 10%, then the general portfolio return expectation is as under.

(60% x 10%) + (40% x 6%)=8.4%.

How A lot To Make investments?

As soon as the targets are outlined with the goal quantity, asset allocations are accomplished, and return expectation from every asset class is outlined, then the ultimate step is to determine the quantity to take a position every month.

There are two methods to do it. One is a continuing month-to-month funding all through the purpose interval. The second approach is growing some fastened % every year as much as the purpose interval. Resolve which fits you.

I hope the above info gives you readability earlier than leaping into fairness mutual fund merchandise.

How Many Mutual Funds Are Sufficient?

What number of mutual funds do we now have? Is it 1, 3, 5, or greater than 5? The reply is straightforward…you don’t want greater than 3-4 funds to spend money on mutual funds. Whether or not your funding is Rs.1,000 a month or Rs.1 lakh a month. With a most of 3-4 funds, you’ll be able to simply create a diversified fairness portfolio.

Having extra funds doesn’t offer you sufficient diversification. As a substitute, in lots of circumstances, it could create your portfolio overlapping and result in underperformance.

Few select new funds for every purpose. That creates a whole lot of muddle and confusion. As a result of, beginning is straightforward and after few years, it appears to be like like a hilarious activity to handle. Therefore, my suggestion is to have the identical set of funds for all targets. Both you create a unified portfolio or create a separate folio for every purpose and make investments.

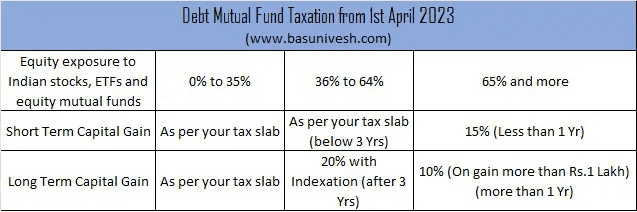

Taxation of Fairness Mutual Funds for FY 2023-24

As I discussed above, there are specific modifications occurred with respect to debt mutual funds taxation. This modification to the Finance Invoice 2023 created three classes of mutual funds for TAXATION.

# Mutual Funds Holding Extra Than 65% Or Extra In Indian Fairness, Indian Fairness ETFs, Or Fairness Funds

On this class, there is no such thing as a change in taxation. They’re taxed like fairness funds. In case your holding interval is lower than a 12 months, then STCG is relevant and taxed at 15%. Nonetheless, in case your holding interval is greater than 1 12 months, then LTCG is relevant and taxed at 10% (over and above the aggregated long-term capital achieve of Rs.1 Lakh). As there is no such thing as a change on this class, I hope it’s clear for you.

You seen that the taxation guidelines for fairness are unchanged. The outdated guidelines will proceed as typical.

# Mutual Funds Holding Much less Than 65% Or Extra Than 35% In Indian Fairness, Indian Fairness ETFs, Or Fairness Funds

Right here additionally there is no such thing as a change. They’re taxed like debt funds (as per the outdated rule). In case your holding interval is lower than three years, then the achieve is taxed as STCG and the speed is as per your tax slab. Nonetheless, if the holding interval is greater than three years, then taxed at 20% with an indexation profit.

# Mutual Funds Holding Much less Than Or Equal To 35% Of Indian Fairness, Indian Fairness ETFs, Or Fairness Funds

Here’s a large change (if the modification handed in parliament). The taxation is as per your tax slab. No query of LTCG or STCG. This taxation rule can be relevant from 1st April 2023.

Investments accomplished earlier than thirty first March 2013 are eligible as per the outdated tax guidelines (with indexation for long-term capital achieve).

Due to this, many are very offended with the federal government (I can perceive buyers’ anger however I hate the anger of the finance business. As a result of it’s primarily as a result of they lose the enterprise).

The identical could be tabulated as under.

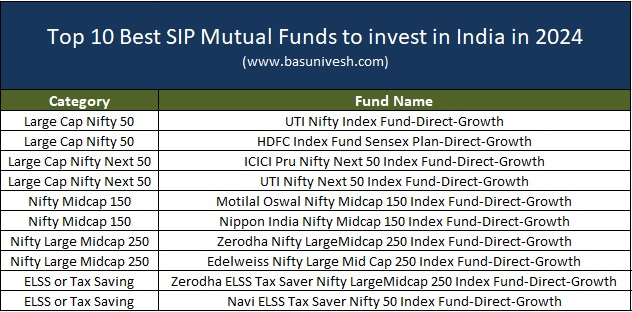

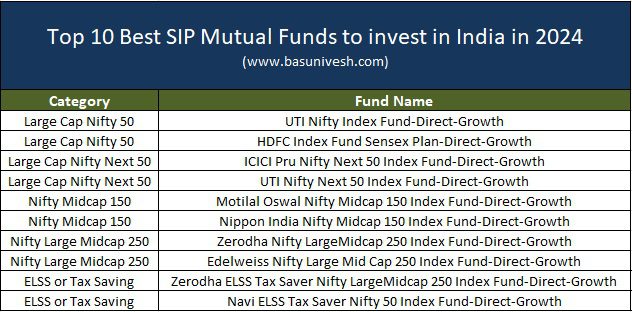

Prime 10 Greatest SIP Mutual Funds To Make investments In India In 2024

I’ve written few posts which as per me are greatest so as to add worth to your funding journey. Therefore, counsel you learn them first (sharing the record under).

I’ve created a separate set of articles to coach the buyers with respect to debt mutual funds. Making an attempt to jot down as many as doable on this class. As a result of what I’ve seen is that many are lagging in understanding the debt funds. You may confer with the identical right here “Debt Mutual Funds Fundamentals“.

Allow us to transfer on to my sharing of the Prime 10 Greatest SIP Mutual Funds To Make investments In India In 2024.

Greatest SIP Mutual Funds To Make investments In India In 2024 -Giant-Cap

Final time I really useful two Giant Cap Index Funds. I’m retaining the identical funds for this 12 months too.

# UTI Nifty Index Fund-Direct-Progress

# HDFC Index Fund Sensex Plan-Direct-Progress

Greatest SIP Mutual Funds To Make investments In India In 2024 -Mid-Cap

Final time, I really useful two Nifty Subsequent 50 Index Funds. This 12 months additionally, I’m retaining the identical funds for my suggestions in Mid Cap Funds. In my article Nifty Subsequent 50 Vs Nifty Midcap 150 – Which is greatest?, I’ve given the explanation why the Nifty Subsequent 50 must be your higher different than the Nifty Mid Cap.

Nifty Subsequent 50 is definitely an essence of each large-cap and mid-cap. Due to this, it acts with the identical volatility as mid-cap. Therefore, I’m suggesting Nifty Subsequent 50 as my mid-cap fund than explicit Mid Cap Lively or Index Funds.

I’m persevering with final 12 months’s selections:-

# ICICI Pru Nifty Subsequent 50 Index Fund-Direct-Progress

# UTI Nifty Subsequent 50 Index Fund-Direct-Progress

Nonetheless, if you’re keen on mid-cap, then you’ll be able to select the under Midcap Index Funds.

# Motilal Oswal Nifty Midcap 150 Index Fund-Direct-Progress

# Nippon India Nifty Midcap 150 Index Fund-Direct-Progress

Greatest SIP Mutual Funds To Make investments In India In 2024 -Giant and Midcap Fund

Two years again after I wrote a submit, I used to be unable to search out this class. Nonetheless, at present, two funds can be found on this class. Whereas reviewing the product Zerodha, I aired my view on this class. You may confer with the identical “Zerodha Nifty LargeMidcap 250 Index Fund – Ought to You Make investments?“.

As that is the mix of the Nifty 100 and Nifty Midcap 150 Index within the ratio of fifty:50. I counsel this must be for individuals who want to maintain in the identical ratio and with a single fund quite than two to a few funds. My suggestions are as under.

# Zerodha Nifty LargeMidcap 250 Index Fund-Direct-Progress

# Edelweiss Nifty Giant Mid Cap 250 Index Fund-Direct-Progress

Greatest SIP Mutual Funds To Make investments In India In 2024 – ELSS Or Tax Saver Funds

As I’ve talked about above, now we now have Index Funds obtainable on this class additionally. Therefore, quite than having energetic funds, I’m suggesting passive funds right here too.

# Zerodha ELSS Tax Saver Nifty LargeMidcap 250 Index Fund-Direct-Progress

The above fund is for individuals who need the mix of the Nifty 100 + Nifty Midcap 150 within the ratio of fifty:50. Nonetheless, in the event that they don’t need publicity to mid-cap, then they will take into account the under fund.

# Navi ELSS Tax Saver Nifty 50 Index Fund-Direct-Progress

What about Small-Cap Funds?

Consult with my earlier submit “Who CAN Make investments In Small Cap Funds?“, the place it’s evident from the previous 20 years of information that by taking larger danger by means of small cap, it’s possible you’ll find yourself with lower than Midcap return. Therefore, I really feel it’s an pointless headache.

Personally, I by no means invested in small-cap funds, and in addition for all my fee-only monetary planning shoppers, I by no means counsel small-cap funds. I could also be conservative. Nonetheless, in the long run, what I need is an honest return with sound sleep at evening. Therefore, staying away from Small Cap Funds (despite the fact that the entire of India is at present behind Small Cap 🙂 ).

So that you seen that this 12 months, I stayed away from Flexi Cap Funds, and Hybrid Funds, and within the case of ELSS, I advised the index funds solely. Nevertheless it doesn’t imply those that invested in Flexi Cap Funds or Hybrid Funds should come out. As a substitute, have a relentless monitor).

Lastly, a listing of my Prime 10 Greatest SIP Mutual Funds to spend money on India in 2024 is under.

What’s my fashion of development Fairness Portfolio?

I’ve listed all of the funds above. Nonetheless, I counsel developing the portfolio as under inside your fairness portfolio.

50% Giant Cap Index+30% Nifty Subsequent 50+20% Midcap

50% Giant Cap Index+30% Nifty Subsequent 50+20% Flexi Cap Funds (You should use my earlier advice of Parag Parikh Flexi Cap Fund). This I’ve talked about earlier as my favourite method.

In any other case, a single NIfty Giant Midcap 250 Index Fund is sufficient for the fairness. Could also be it look concentrated on account of single fund holding. Nonetheless, not directly you might have an publicity equally to giant cap and mid cap.

Conclusion:- These are my choices but it surely doesn’t imply they have to be common choices. Therefore, when you have a special opinion, then you’ll be able to undertake so. You additionally seen that I hardly change my stance till and except there’s a legitimate purpose. Ultimately, investing is a BORING and LONG-TERM journey, proper? Better of LUCK!!

Disclaimer: The Views Expressed Above Ought to Not Be Thought-about Skilled Funding Recommendation, Commercial, Or In any other case. The Article Is Solely For Common Academic Functions. The Readers Are Requested To Think about All The Threat Elements, Together with Their Monetary Situation, Suitability To Threat-Return Profile, And The Like, And Take Skilled Funding Recommendation Earlier than Investing.