{kind=link}

Eicher Motors Ltd. – Made Like A Gun

Eicher Motors Restricted (EML), included in 1982, is the listed flagship firm of the Eicher Group in India and a number one participant within the Indian vehicle trade. On a standalone foundation, EML manufactures and markets bikes beneath the long-lasting Royal Enfield model, with its manufacturing services primarily based in Chennai, Tamil Nadu. It additionally has analysis and improvement (R&D) services at two areas—Leicestershire, UK, and Chennai. Moreover, the corporate operates as a holding firm for investments in Volvo-Eicher Industrial Automobiles (VECV) Restricted. A three way partnership of EML (54.4%) and AB Volvo (45.6%), VECV got here into existence with impact from July 1, 2008. The JV is engaged in EML’s truck and bus operations, auto elements enterprise and technical consulting providers enterprise and Volvo Group’s Indian truck gross sales and advertising features, in addition to service and spares community operations for each Volvo vans and buses. In 2020, VECV efficiently built-in Volvo Buses India into VECV, together with the manufacture, meeting, distribution, and sale of Volvo Buses in India.

Merchandise & Providers:

The corporate has numerous merchandise beneath its two enterprise segments.

- Royal Enfield – The Firm has fashions like Bullet 350, Traditional 350, Meteor 350, Himalayan, Scram 411, Hunter 350, Tremendous Meteor 650 and 650 Twins.

- VECV – It consists of Heavy, Gentle & Medium Obligation vans, Buses, particular purposes like ambulances from Eicher and Volvo Manufacturers. It additionally has Engine Enterprise, Engineering part enterprise and Powertrain enterprise.

Subsidiaries: As on FY23, the corporate has 6 subsidiaries, 1 Joint Ventures and 4 step down subsidiaries.

Key Rationale:

- Market Chief – Eicher Motors (EML) is the International chief within the 250cc -750cc mid section bike. It has a market share of ~90% within the Indian Mid dimension section by way of its aspirational fashions beneath the Royal Enfield (RE) model, corresponding to Bullet, Traditional, Interceptor amongst others. The corporate has been gaining market share within the above 125cc section with 32.9% share as on Q1FY24. Total share in Bikes stands at 7.6% as on Q1FY24. Within the Worldwide market, the corporate has a market share of about 8% in Americas, 9% in APAC and 9% in EMEA in the identical mid section with a quantity development of 4.5 occasions from 20,825 in FY19 to 89,226 in FY23. The VECV division has a general CV market share of 17.1% in FY23. The market share throughout segments as of July finish 2023 are 36.9% in L&MCV, 8.5% in HCV, 24.7% in Buses and 94.7% in Volvo vans India (Excessive Finish premium Section). The supplier community of the Royal Enfield (2W Division) have grown 2.5x in 6 years from simply 825 shops in FY18 to 2059 shops in FY23. In that 2059 shops, 1090 belongs to studio shops and 969 belongs to Massive Measurement shops. These shops are unfold throughout ~1750 cities in India.

- Gross sales Development – The general Bikes quantity beneath the Royal Enfield section have crossed the pre-covid ranges at 8.35 lakh models in FY23 from 8.24 lakh models in FY19. The volumes in FY20, 21 and 22 have been impacted attributable to COVID 19 pandemic and provide chain constraints. Royal Enfield is likely one of the few firms within the 2W section which crossed the pre-covid gross sales mark and outperformed the trade development. Gross sales Quantity in Q1FY24 stands at 2.27 lakh models, a development of twenty-two% YoY. VECV has achieved a highest ever first quarter (Q1) gross sales throughout many segments in Q1FY24. Total VECV gross sales additionally achieved the Highest ever first quarter gross sales of 19,571 models in Q1FY24 exceeding earlier file of 17,469 models in Q1FY23.

- Q1FY24 – Eicher Motors reported a powerful income development of 17% YoY Q1FY24 to Rs.3986 crore from Rs.3397 crore for a similar interval final yr. EBITDA had a development of 23% of Rs.1021 crore in Q1FY24 vs. Rs.831 crore for a similar interval final yr. EBITDA Margin has improved by ~120 bps from 24.4% in Q1FY23 to 25.6% in Q1FY24 on account of 1.5% worth hike in sure fashions. PAT confirmed an enormous development of fifty% YoY to Rs.918 crore in Q1FY24 from Rs.611 crore in Q1FY23.

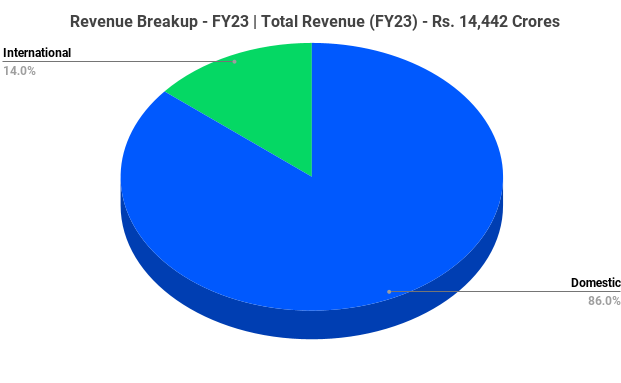

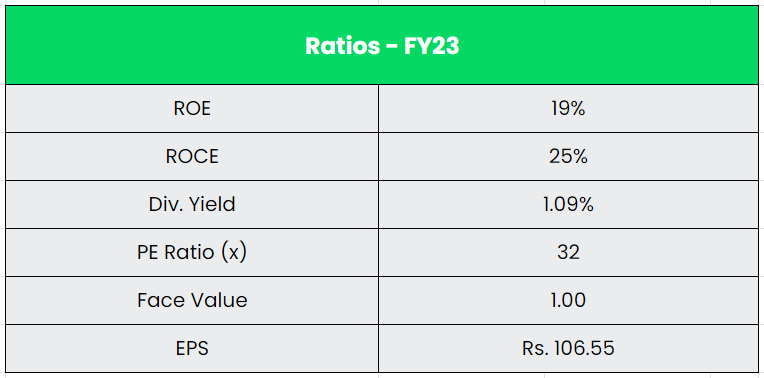

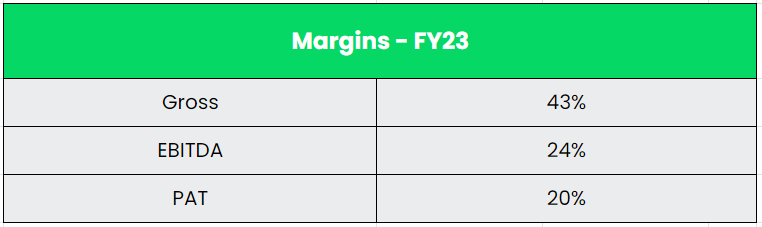

- Monetary Efficiency – The three 12 months income and revenue CAGR stands at 16% and 17% respectively between FY20-23. The share of non-Bike enterprise (Equipment, Apparels, and so forth.) have grown almost 4x between FY17-FY23. The corporate has a powerful steadiness sheet with a debt-to-equity ratio of simply 0.02x which equals to close zero debt. The money and investments within the steadiness sheet totals to ~Rs.13180 crores which is sort of 14% of the Market Capitalisation. This reveals the robust money steadiness of the corporate. The final 5-year collected FCF (Free Money Stream) have crossed over Rs.6000 crores, depicting the money producing potential of the corporate.

Trade:

The Indian automotive trade has seen a wholesome revival in FY22-23, aided by a restoration within the financial actions and restoration in mobility submit COVID impacted interval (FY 2021-22). Nonetheless, the two-wheeler section is but to succeed in the pre-pandemic ranges because the trade navigates by way of excessive inflation, provide chain hurdles, sharp enhance in enter prices, and the rising price of possession attributable to regulatory modifications. In accordance with the Society of Indian Car Producers (SIAM), the two-wheelers section grew by a comparatively reasonable 17% YoY development, after witnessing de-growth for the earlier three consecutive years. The home gross sales of two wheelers in FY 2022-23 have been 15.9 million models as towards 13.5 million models in FY 2021-22. Bike gross sales elevated by 14% YoY to 10.2 million models, whereas scooter gross sales grew over 25% YoY to five.2 million models. The gross sales of Electrical two-wheelers in India grew over two-and-half-fold to 7,28,090 models in FY 2022–23 over the earlier fiscal, aided by subsidies supplied by the federal government(s) and rising penetration of electrical autos throughout segments.

Development Drivers:

- The International Direct Funding (FDI) influx into the Indian automotive trade between April 2000-March 2023 stood at US$ 34.7 billion as per the information launched by the Division for Promotion of Trade and Inside Commerce (DPIIT).

- In accordance with the Financial Survey, by 2031, the working age inhabitants i.e., 20-59 years is poised to extend by 300 bps from 55.8% in 2021 to 58.8% in 2023.

- India to grow to be the youngest nation by 2025 with a mean age of 25 years. With Royal Enfield having a big younger buyer base (31% within the age of 18-25 and 41% within the age of 26-35), they’ve the excessive possibilities of getting benefitted.

Rivals: Hero MotoCorp, TVS Motors, and so forth.

Peer Evaluation:

Among the many above rivals, Eicher motors has higher return ratios and steady income development than the opposite two. The steadiness sheet energy of Eicher is manner higher than Hero and TVS compared. The excessive ROE and Low ROCE of TVS is because of the affect of excessive Debt and low fairness.

Outlook:

Within the Bike section, the corporate has launched “The Hunter 350” mannequin within the August final yr and it has been profitable, with over 200,000 models bought in simply 11 months. The just lately launched above 500cc section “Tremendous Meteor” had a very good response globally. The corporate is planning to launch round 11-12 merchandise within the medium time period which incorporates the very newest Bullet launch and a Himalayan 450 launch within the close to time period. Within the Worldwide entrance, Eicher is planning to open New Retail codecs – Studio shops, Store-in-shop for attire, and bike shows to extend buyer attain. It has 92, 68 and 50 unique shops in Americas, EU&MEA and APAC areas. Additionally it is evaluating alternatives to arrange CKD (Fully Knocked Down) facility in precedence markets in APAC and LATAM areas and just lately opened a CKD facility at Nepal. The corporate additionally making a major progress within the EV area with a devoted 100+ folks. They’re at the moment within the execution section of the challenge.

Valuation:

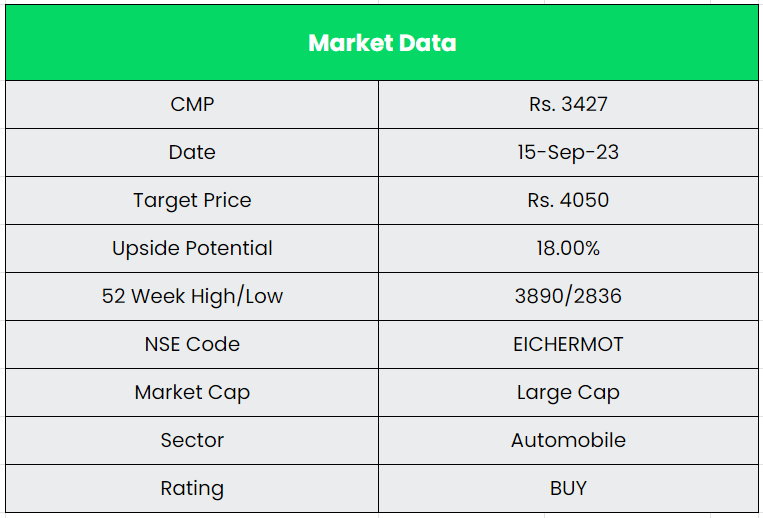

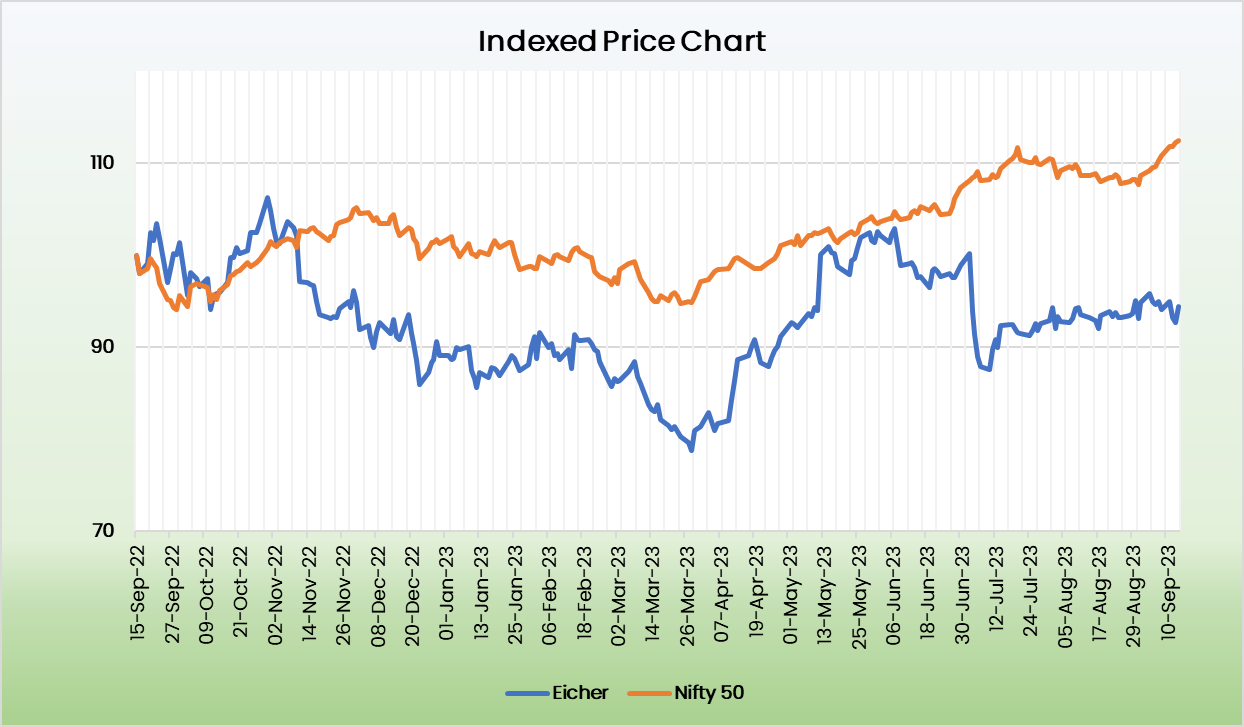

We consider Eicher Motos will proceed to achieve the market share by way of aggressive community enlargement in each the home and Worldwide, A number of launches, Coming into new territories and Infrastructure enhance by Authorities Initiatives. We suggest a BUY score within the inventory with the goal worth (TP) of Rs.4050, 28x FY25E EPS.

Dangers:

- Dependency Danger – The corporate’s development has been pushed by the over 250-cc bike sub section in the previous few years. It has no presence within the excessive quantity (75-110 cc) sub-segments. Even within the over 250-cc sub-segment, its Traditional & Hunter 350 mannequin accounts for many of the gross sales. Robust competitors to its main mannequin might considerably damage its volumes.

- Cyclical Danger – The VECV section of the corporate is extremely prone to the cyclicality of the Industrial Automobile Trade which may affect the gross sales development of the identical section.

- Slowdown Danger – EML has negligible presence within the mid-market 2-wheeler section. A sustained slowdown within the economic system might hamper the discretionary spending and may also lead to downtrading throughout client classes which may affect development of premium bikes in brief to medium time period.

Different articles you might like

Submit Views:

2,991