{kind=link}

Affle India Ltd. – Cell Advert Participant

Affle was based by Mr. Anuj Khanna Sohum (CEO) in 2005-06. With moto of “Constructed to Final”, Mr. Sohum has efficiently navigated Affle by way of a number of trade and technological adjustments confronted by the dynamic ever evolving ad-tech trade over previous 15+ years. Affle is a worldwide know-how firm with a proprietary client intelligence platform that delivers client engagement, acquisitions and transactions by way of related Cell Promoting. The platform goals to reinforce returns on advertising funding by way of contextual cellular adverts and in addition by lowering digital advert fraud. The corporate now has ~3.2 Bn linked gadgets. Affle 2.0 goals to succeed in greater than 10 Bn linked gadgets together with cellular good telephones, linked TV, good wearables and out-of-home screens to allow built-in omnichannel on-line and offline client journeys.

Merchandise & Companies:

The Firm caters to 2 kinds of Platforms.

- Client Platform – Delivers client suggestions and conversions by way of related cellular promoting for main manufacturers and B2C firms globally. This platform is subdivided into CPCU (Value Per Transformed Consumer) & Non-CPCU (Value per million impressions) fashions.

- Enterprise Platform – It gives end-to-end options to enterprises for enhancing their engagement with cellular customers, resembling creating Apps, enabling offline to on-line commerce for offline companies with e-commerce aspirations and offering enterprise grade knowledge analytics for on-line and offline firms.

Subsidiaries: As on FY23, the corporate had 21 subsidiaries.

Key Rationale:

- Smartphone Period – Share of cellular in India’s digital media spends jumped to 76% in FY21 (vs 45% in FY19), rising at 45% CAGR to US$1.9 bn. Beneficial macro developments like i) enormous base of good telephone customers in India & rising markets with decrease penetration in comparison with developed markets, ii) rising web knowledge consumption and cellular display time pushed by decrease knowledge prices and iii) rising adoption of m-commerce gave important enhance to cellular getting used as a most popular channel for promoting. Affle is properly positioned to trip this development wave with >95% income coming from cellular promoting.

- Enterprise Mannequin – Affle’s Value Per Transformed Consumer (CPCU) is a differentiated enterprise mannequin in an trade which normally operates on Value per Media (CPM) (Media primarily based enterprise mannequin) or Value per Click on (CPC) mannequin. A CPCU mannequin signifies that income is earned when a person is transformed right into a client by clicking on the advert adopted by a obtain or buy or registration; versus CPM / CPC which earn revenues on a “per 1000 views” foundation or merely “click on foundation”. Round 93% of the general income is derived from the CPCU mannequin of the corporate in Q1FY24. The corporate is at the moment specializing in excessive development trade segments throughout E (E-Commerce, Edtech, Leisure), F (Fintech, FMCG, Foodtech), G (Gaming, Authorities, Grocery) and H (Healthtech, Hospitality & Journey). Income contribution from these 4 classes is round 90%+ in Q1FY24.

- Q1FY24 – In Q1FY24, Affle posted a income of Rs.407 crore, registering a development of 14.3% on a QoQ foundation and 17% on a YoY foundation. Its consolidated EBITDA for the quarter grew by 9% QoQ and 15% YoY to Rs.78 crore, led by the sharp restoration within the worldwide enterprise. Nevertheless, the corporate’s EBITDA margins declined by 80bps QoQ to 19.2%. It reported a internet earnings of Rs.66 crore, up 6% QoQ. The CPCU enterprise delivered 68.7mn conversions in Q1FY24 at a CPCU price of Rs.55, totalling to a section topline of Rs.380 crore. The corporate’s India enterprise stood flat and reported a development of 0.4% QoQ. On the Worldwide Enterprise entrance, the corporate reported a wholesome development of twenty-two% QoQ, led by strong system addition.

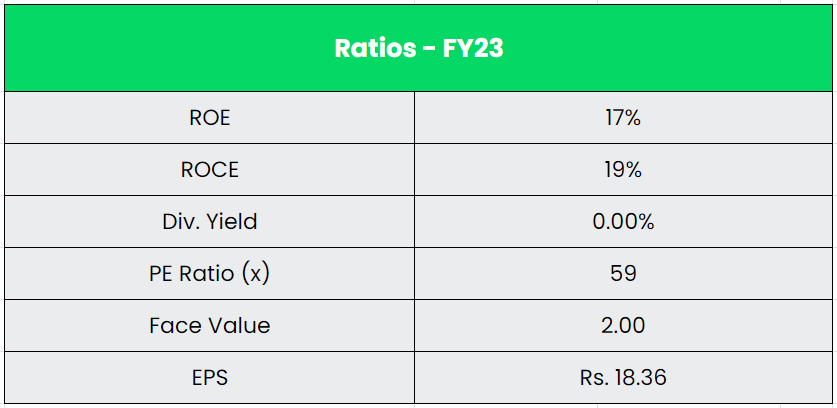

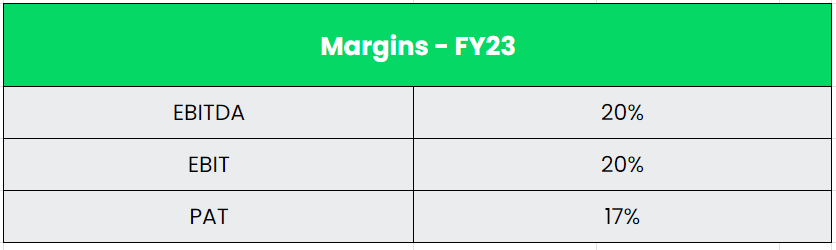

- Monetary Efficiency – The 5 Yr income and revenue CAGR stands at 54% and 54% respectively between FY18-23. The steadiness sheet of the corporate is robust with a debt-to-equity ratio of 0.1x. The Working Money stream of the corporate has grown at a 44% CAGR from Rs.42 crore in FY18 to Rs.260 crore in FY23. The OCF/EBITDA ratio of the corporate stands at 90% in FY23 which signifies a powerful money conversion from EBITDA.

Business:

India is the world’s second-largest telecommunications market with a subscriber base of 1,170.75 million in January 2023 and has registered sturdy development within the final decade. The whole subscriber base, wi-fi subscriptions in addition to wired broadband subscriptions have grown persistently Tele-density stood at 84.51%, as of March 2023, whole broadband subscriptions grew to 846.57 million till March 2023. The aggregated knowledge consumed as on thirty first December 2022 was 14,024,519 GB. As per GSMA, India is on its method to turning into the second-largest smartphone market globally by 2025 with round 1 Bn put in gadgets and is anticipated to have 920 Mn distinctive cellular subscribers by 2025 which can embody 88 Mn 5G connections. It’s also estimated that 5G know-how will contribute roughly $450 Bn to the Indian Financial system within the interval of 2023-2040. International Digital Promoting is driving on a powerful development and it’s anticipated to succeed in $785 bn in 2025 from $381 bn in 2020 at a CAGR of 16%. Digital Advert spends as a % of whole Promoting expense in India is at a mere 29% in 2021 in comparison with China with 82%.

Progress Drivers:

- Solely half the world is on-line with US/UK at ~80% smartphone penetration and Rising Markets trailing with a lot decrease ranges of smartphone penetration.

- In Union Finances 2023-24, the Division of Telecommunications was allotted Rs.97,579.05 crore (US$ 11.92 billion). Of this, US$ 48.88 million (Rs.400 crore) is for Analysis and Improvement, US$ 611.1 million (Rs.5,000 crore) is for Bharatnet.

- India is among the highest shoppers of information per day with roughly 5 hours of every day time spend on smartphones. Energetic web customers in India are anticipated to succeed in 900 Mn by 2025.

Opponents: Vertoz Promoting.

Peer Evaluation:

There is no such thing as a comparable listed peer as a result of they function in numerous geographies or service completely different components of ad-tech worth chain. Vertoz, is the one Advert-tech peer listed in Indian Markets. It provides programmatic promoting platform; nonetheless, it derives 90% of income from worldwide markets and has income dimension of simply ~5-6% of Affle.

Outlook:

Administration continues to focus on upselling and cross-selling of AFFLE’s options, with distinctive advert placement throughout OEM and operator app shops. CPCU fashions present CTV (Join TV) options with family sync capabilities within the US and world rising markets. The corporate has additionally efficiently launched a full-funnel proposition on the iOS App Retailer, turning into a frontrunner on the Apple SKAN (StoreKit Advert Community) ecosystem. Administration indicated that AFFLE is more likely to obtain 20-25% development in India and different rising markets in FY24, and expects comparable momentum in FY25. From a long-term perspective, the corporate expects to see multi-quarter tailwinds in system additions along with larger shopper acquisition, which ought to enhance income potential. The corporate believes it’s well-positioned to counter short-term challenges and has taken decisive actions in areas resembling folks, partnerships, merchandise and platforms, which it believes will yield ends in FY24, marked by undertaking ramp-ups in Q2 and turnaround in Q3FY24.

Valuation:

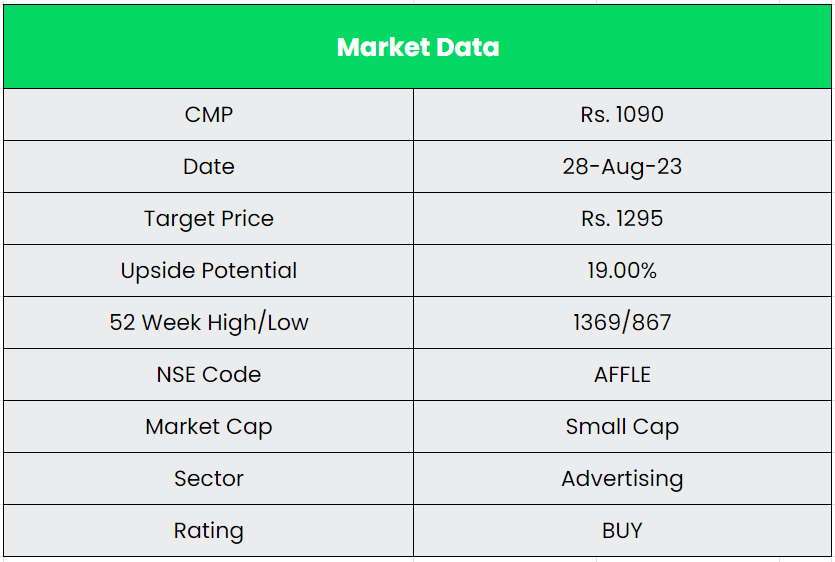

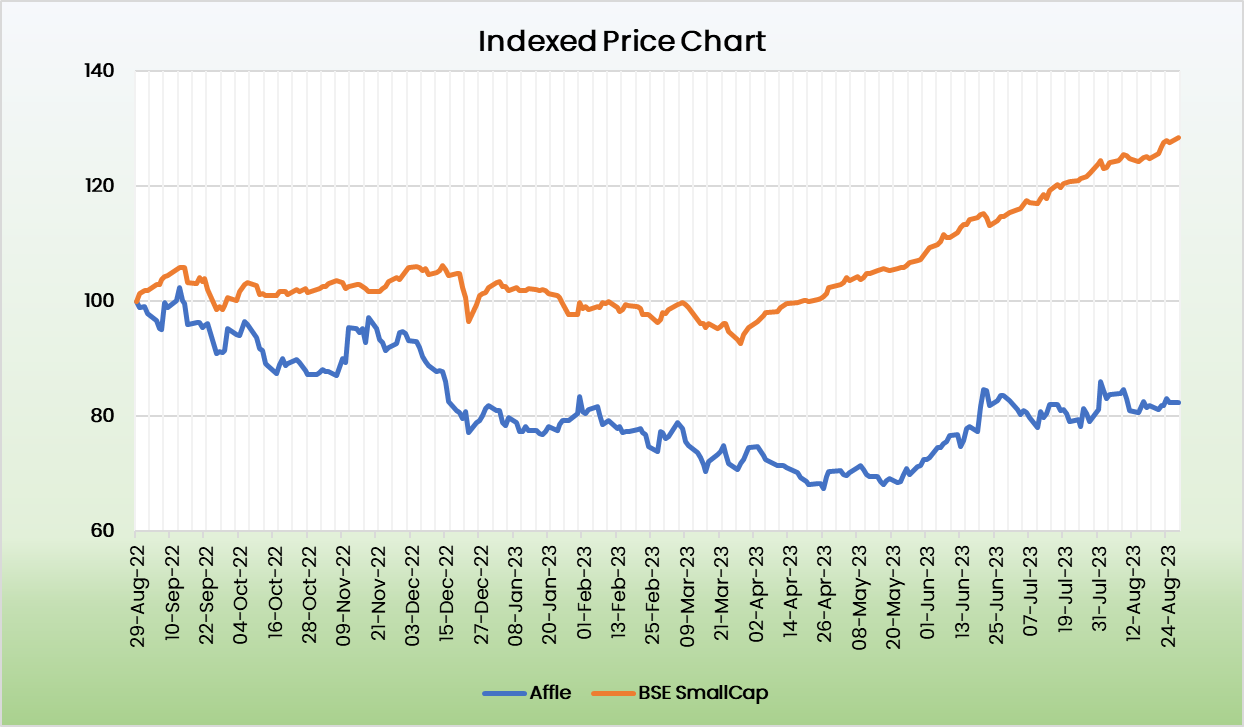

We consider Affle has a singular enterprise mannequin and a powerful technique to penetrate the focused geographies and verticals. Additionally, the corporate has superior penetration within the worldwide enterprise and robust income development potential going forward. We advocate a BUY score within the inventory with the goal worth (TP) of Rs.1295, 47x FY25E EPS.

Dangers:

- Regulatory Danger – The digital promoting enterprise mannequin is very inclined to knowledge privateness rules. Stricter rules or restrictions on entry to such direct or third-party knowledge might enhance the price of compliance, adversely affect stock and knowledge value, and scale back the accuracy and efficacy of current algorithms.

- Aggressive Danger – The marketplace for cellular promoting options is very aggressive with a number of regional and world gamers. Apart from Google and Fb, there are a number of comparatively smaller gamers, resembling InMobi, Criteo, and many others. who compete with Affle throughout numerous geographies.

- Financial Downturn – AdTech is inherently a cyclical enterprise and has a excessive correlation with financial development. Downturns usually result in companies chopping down on their discretionary spend, particularly these associated to promoting.

Different articles you might like

Submit Views:

3,833