{kind=link}

After forty-three months of forbearance, the pause on federal pupil mortgage funds has ended. Initially enacted on the onset of the COVID-19 pandemic in March 2020, the executive forbearance and curiosity waiver lasted till September 1, 2023, and debtors’ month-to-month funds resumed this month. As mentioned in an accompanying submit, the pause on pupil mortgage funds afforded debtors over $260 billion in waived funds all through the pandemic, supporting debtors’ consumption and financial savings over the past three years. On this submit, we analyze responses of pupil mortgage debtors to particular questions within the August 2023 SCE Family Spending Survey designed to gauge the anticipated influence of the cost resumption on future spending progress, the danger of credit score delinquency for debtors, and the economic system at giant. The findings counsel that the cost resumption could have a comparatively small general impact on consumption, on the order of a 0.1 share level discount in combination spending from August ranges, and a (delayed) return of pupil mortgage delinquency charges again to pre-pandemic ranges. Throughout teams, we see little variation in spending responses however discover that low-income debtors, feminine debtors, these with lower than a bachelor’s diploma, and people who weren’t in compensation earlier than the pandemic anticipate the best probability of missed pupil mortgage funds.

The SCE Family Spending Survey is fielded each 4 months as a rotating module of the Survey of Client Expectations (SCE), which itself is a month-to-month, nationally consultant internet-based survey of a rotating panel of family heads performed by the Federal Reserve Financial institution of New York since June 2013. Right here, we give attention to responses by about 1,000 respondents to a particular set of questions added to the August 2023 survey. Of those respondents, 225 reported having excellent pupil loans, of which a subset of 151 respondents indicated that their federal pupil loans had been beforehand “paused” however shall be getting into compensation in October. The remaining group contains these whose funds had been by no means paused or those that are enrolled at school full-time and never resuming compensation. We requested these debtors getting into compensation how they plan to afford their looming month-to-month pupil mortgage funds and the way their chance of lacking pupil and non-student-loan funds will change as a result of cost resumption.

We start by briefly discussing our pattern. An awesome majority of our pattern of pupil mortgage debtors held federal loans (with 74 % reporting they maintain federal loans solely and 20 % reporting they maintain each federal and personal loans). Of the 151 respondents who shall be getting into compensation, 71 % had been making month-to-month funds previous to the cost pause; roughly half of the debtors in compensation had been in a regular (ten-year) compensation plan (36 %) and half had been in an income-driven compensation (IDR) plan (35 %). About 23 % of our pattern getting into compensation had been in deferment or forbearance previous to the pandemic, most below in-school deferment. Round 6 % of debtors weren’t actively making funds regardless of funds being required.

Expectations for Revenue-Pushed Compensation Enrollment

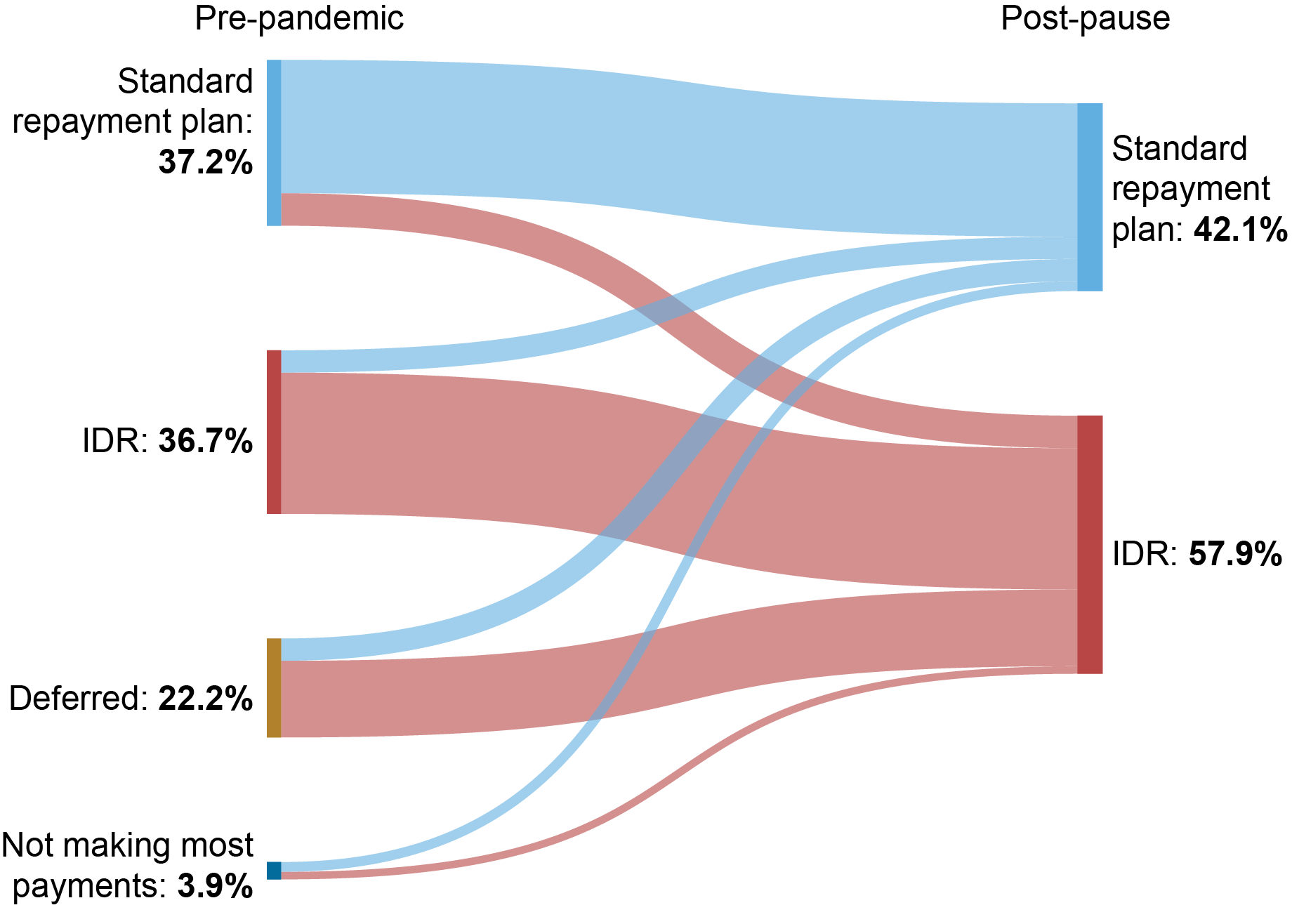

We started by asking debtors if they’d enter the usual ten-year compensation plan (the default possibility) or enroll in an IDR plan. The Biden Administration just lately debuted a brand new IDR plan, the Saving on a Priceless Schooling (SAVE) plan, that lowered funds for low-income debtors and has already enrolled over 4 million debtors (as of September 5). Our survey outcomes counsel that the interesting phrases of the SAVE plan for low-income debtors will seemingly enhance enrollment in IDR plans. Of these debtors who had been beforehand in a regular compensation plan, 20 % anticipate to enroll in an IDR plan, and 84 % of those that had been beforehand in an IDR plan anticipate to stay enrolled in IDR—outcomes that taken collectively would characterize a modest uptick in IDR enrollment among the many extra seasoned debtors. In the meantime, debtors who weren’t in compensation previous to the pandemic overwhelmingly favor IDR over the usual cost, with 78 % of first-time repayers stating an intent to enroll in IDR. As proven by the flows within the chart beneath, we estimate the IDR enrollment amongst these in compensation would enhance from 50 % pre-pandemic to 58 % after funds resume.

The SAVE Plan Will Possible Drive New Curiosity in Revenue-Pushed Compensation (IDR) for Scholar Mortgage Debtors

Notes: To categorise debtors into pre-pandemic teams, we requested respondents “Previous to March 2020, had been you making a lot of the funds on these loans?,” with the next choices: (a) Sure, I used to be in a regular compensation plan; (b) Sure, I used to be in an income-driven compensation plan; (c) No, my funds had been deferred (i.e., in-school deferment, army deferment, and so on.); or (d) No, funds had been required however I used to be not making most funds. To categorise debtors into post-pause teams, we framed our query on this method: “The automated forbearance and curiosity waiver for federal pupil loans will finish after August 2023. In September, curiosity will start to accrue, and funds shall be due beginning in October. What are you planning on doing after pupil mortgage cost resumes? (choose all that apply),” with the next choices: (a) Make the usual month-to-month funds; (b) Enroll in an income-driven compensation plan; (c) Skip some funds; (d) Different (please specify); and (e) Not relevant (I’m at school, and funds is not going to be required). Respondents choosing (e) had been excluded from the pattern. Debtors had been sorted into “normal compensation plan” or IDR utilizing responses to (a) or (b) and open-ended responses from (d).

Expectations for Adjustments to Month-to-month Spending

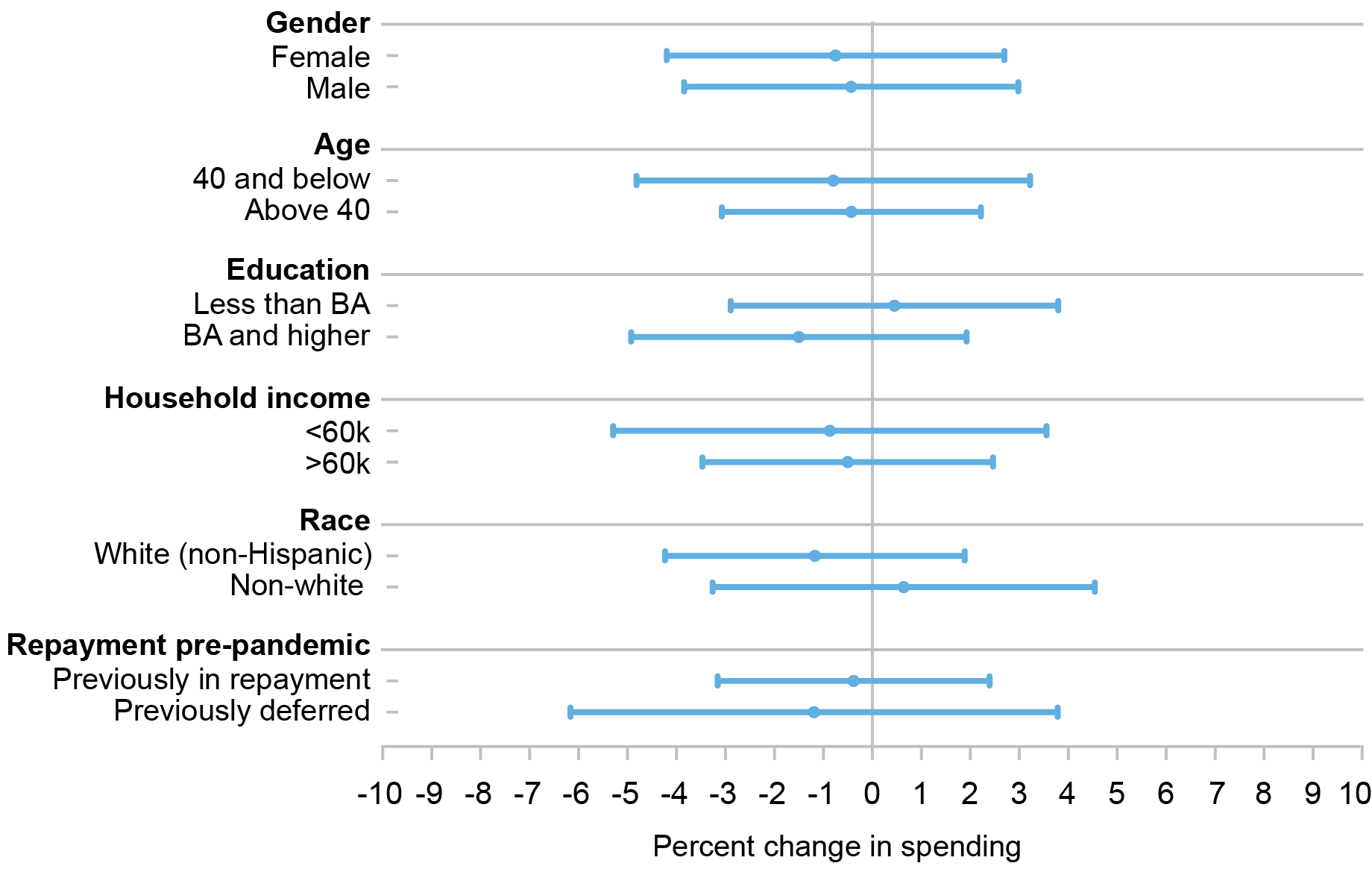

Subsequent, we flip to borrower’s expectations for modifications in month-to-month spending (separate from pupil mortgage funds) as a result of resumption of funds. Extra particularly, we ask debtors, “When pupil mortgage funds resume from October, how do you anticipate that the cost resumption will have an effect on your common month-to-month spending within the three months beginning with October 2023?” On common, debtors anticipate to scale back consumption by round $56 per month from their common month-to-month spending reported in August. If we scale this month-to-month decline as much as the 28 million debtors with federally-managed loans presently in forbearance, this might counsel almost a $1.6 billion decline in month-to-month spending, or 0.1 share level of August 2023 private consumption expenditures (PCE). For context, common month-to-month pupil mortgage funds for federally-managed loans was round $6 billion previous to the pandemic.

Within the chart beneath, we plot the common reported change in anticipated October spending for paused debtors as a share of their August reported common month-to-month spending. Most teams report comparatively small anticipated reductions in spending whereas some teams report larger anticipated future spending regardless of the resumption of funds (survey panelists with out pupil loans additionally report larger future spending). These comparatively modest consumption declines, though not statistically completely different from zero, might be as a result of debtors already started adjusting consumption previous to August or as a result of debtors plan to scale back and/or deplete financial savings to make funds. They’re additionally prone to replicate the big share anticipating to enroll within the extra beneficiant IDR program. Because of our comparatively small pattern measurement, 95 % confidence bands are extensive throughout teams; nevertheless, the purpose estimates with the biggest variations are between these with a minimum of a bachelor’s diploma (who anticipate bigger spending reductions) and people with lower than a bachelor’s diploma, probably reflecting variations in common excellent pupil mortgage balances and cost sizes.

Paused Scholar Mortgage Debtors Solely Count on Modest Consumption Declines from August Spending when Funds Resume

Notes: The chart stories level estimates and 95 % confidence intervals for the anticipated change in spending as a share of common month-to-month spending, break up by numerous teams. To calculate this share, we requested debtors, “When pupil mortgage funds resume from October, how do you anticipate that the cost resumption will have an effect on your common month-to-month spending within the three months beginning with October 2023? Please exclude mortgage funds out of your estimation of spending. Beginning October 2023, I anticipate my common month-to-month spending to (enhance/lower) by [ ].” We then requested debtors for his or her common month-to-month spending on the time of survey: “Roughly, what do you assume was your common month-to-month family spending through the previous three months? I estimate that my common month-to-month family spending was [ ].” We compute the % change in spending for every respondent utilizing a ratio of those two solutions.

Expectations for Lacking Scholar Mortgage Funds

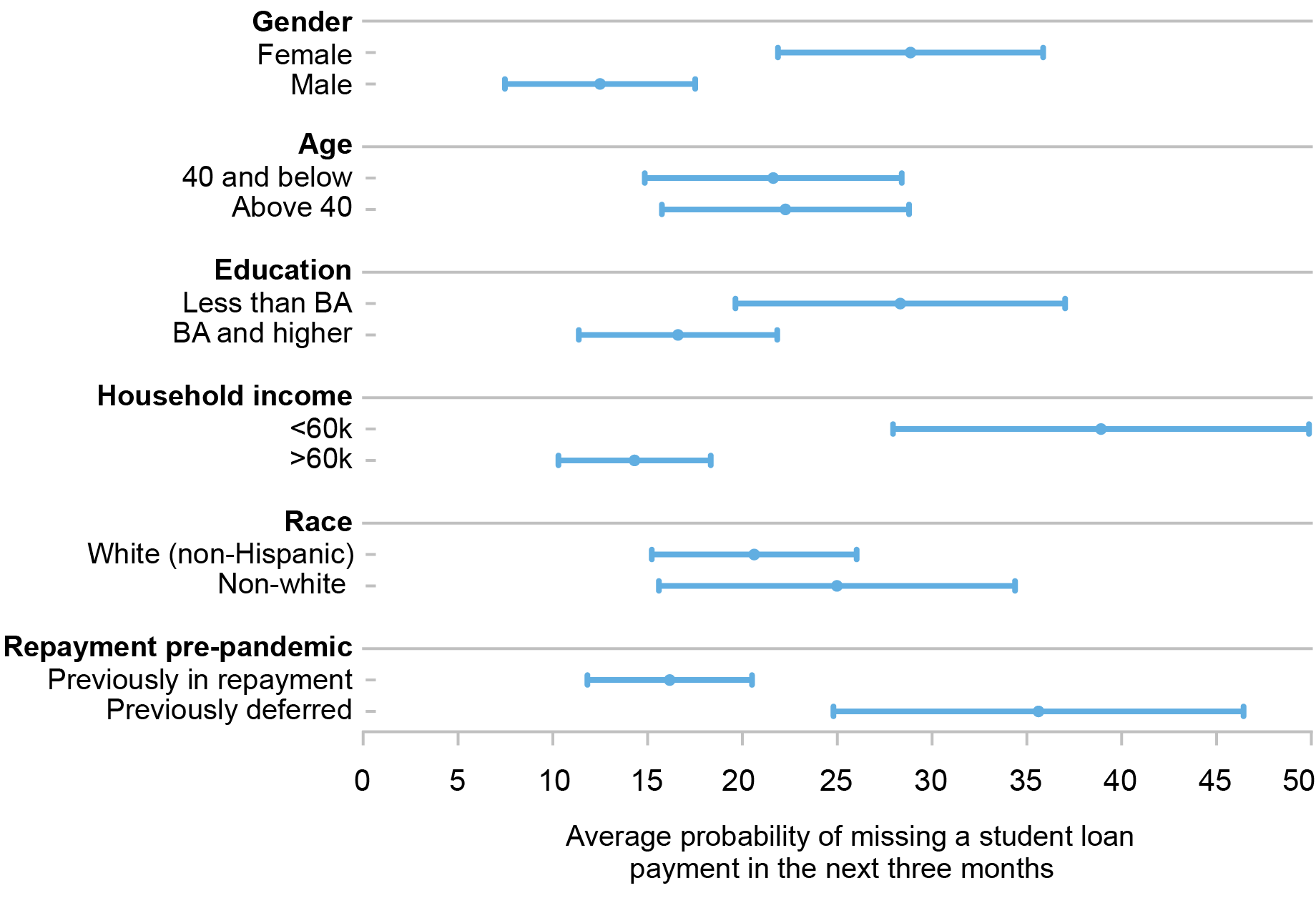

We additionally requested paused pupil mortgage debtors concerning the anticipated chance (“% likelihood”) they’d miss a pupil mortgage cost or a non-student-debt cost within the three months following the cost resumption. Total, paused debtors reported a mean chance of lacking a pupil mortgage debt cost of twenty-two.6 %. Word that this statistic might overstate anticipated hardship and cost problem. Current steering from the U.S. Division of Schooling informs pupil mortgage servicers to not report missed funds to credit score bureaus. As such, debtors could also be extra prone to voluntarily miss funds whereas penalties are much less extreme.

Within the chart beneath, we examine the self-reported chance of lacking a pupil mortgage cost throughout a number of teams, discovering stark and statistically vital variations throughout gender and earnings. Feminine respondents reported greater than twice the chance of lacking a pupil mortgage cost at 28.9 % in comparison with 12.5 % for males. Moreover, debtors with family earnings decrease than $60,000 reported a mean chance of lacking a cost of almost 39 %, in comparison with 14.3 % for these with family earnings above $60,000. Though the estimates are usually not statistically completely different, non-white debtors reported the next common probability of lacking a cost than white non-Hispanic debtors and people with out a school diploma reported the next probability than these with a level. Lastly, we see a big distinction in expectations for missed funds between debtors who had been in compensation previous to the pause and people who are getting into compensation for the primary time, with first-time repayers anticipating greater than twice the probability of missed pupil mortgage funds.

Expectations for Missed Scholar Mortgage Funds Are Excessive, however Much like Pre-Pandemic Ranges

Notes: The chart stories level estimates and 95 % confidence intervals for the anticipated probability a respondent will miss pupil mortgage funds as soon as funds resume, break up by numerous teams. Extra particularly, we ask, “When pupil mortgage funds resume from October, what’s the % likelihood that you’ll miss a minimal cost on any of your pupil mortgage debt, federal and/or non-public, within the three months beginning with October 2023?”

However how do expectations for missed funds examine to cost delinquency earlier than the cost pause? Whereas we shouldn’t have an apples-to-apples, pre-pandemic comparability for expectations of pupil mortgage missed funds, we will examine this chance with the borrower delinquency price from our 2022 Scholar Mortgage Replace, primarily based on credit score report knowledge. As proven within the replace, within the fourth quarter of 2019, roughly 15 % of all pupil mortgage debtors had been both ninety or extra days delinquent or in default. Nevertheless, the denominator on this delinquency price contains debtors not in compensation, a class of debtors we exclude from this SCE survey pattern. Eradicating the 15.4 million debtors reported by the Division of Schooling as not in compensation (that’s, at school, grace, deferment, or forbearance) suggests a pre-pandemic delinquency price of 23 % (for these in compensation)—a price fairly just like the self-reported common chance of lacking a pupil mortgage cost within the SCE survey of twenty-two.6 %.

Expectations for Lacking Non-Scholar-Mortgage Funds

Lastly, we requested pupil mortgage debtors to report the anticipated enhance within the probability of lacking a non-student-debt month-to-month obligation (corresponding to a mortgage, bank card, or auto mortgage cost) on account of pupil mortgage funds restarting. On common, debtors reported a 11.8 % enhance within the probability of lacking a non-student debt cost owing to the scholar debt cost resumption. Debtors throughout teams had been additionally way more related of their expectations of lacking funds for different obligations than for pupil loans, with no proof of statistical distinction between teams. Curiously, feminine respondents reported a decrease chance of lacking a non-student-loan cost than male respondents (though not statistically completely different). That feminine respondents report a far larger probability of lacking pupil mortgage funds than males suggests feminine debtors could also be extra seemingly than male debtors to prioritize their non-student-loan obligations forward of pupil debt in the event that they face difficulties fulfilling all debt obligations.

Conclusion

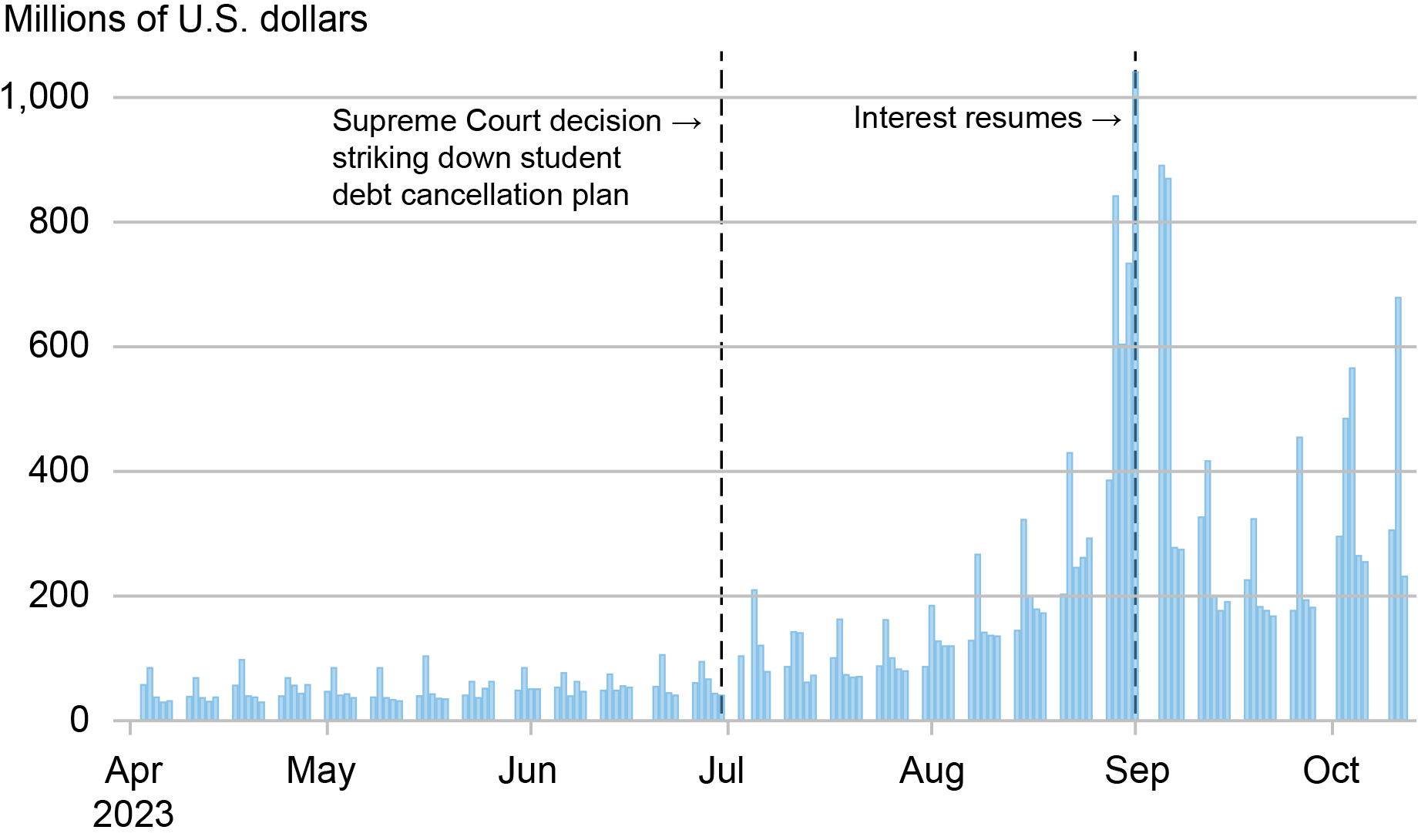

Client spending has been surprisingly robust to date in 2023. Nevertheless, there may be appreciable concern concerning the energy of headwinds stemming from the resumption of pupil mortgage funds, with some financial forecasters predicting it might decrease consumption progress by as a lot as 0.8 share level. There are additionally considerations about rising delinquencies as funds resume, maybe to ranges larger than earlier than the pandemic. Our findings right here primarily based on expectations survey responses counsel solely modest reductions in spending for debtors getting into compensation (of roughly 0.1 share level of August PCE) and probability of missed pupil mortgage funds roughly in keeping with pre-pandemic ranges. One purpose for these comparatively small results is that probably many debtors already made modifications to their financial savings and consumption choices after studying that funds would definitely resume in October. The chart beneath reveals some proof for this speculation. Right here, we plot the every day deposits on the U.S. Treasury by the Division of Schooling, of which the overwhelming majority are federal pupil mortgage funds. We see that deposits elevated after the U.S. Supreme Court docket resolution reversing the broad pupil mortgage forgiveness program and continued to stand up till the top of the zero % curiosity waiver. This sample appears in line with some debtors electing to make bulk funds towards their loans after studying that their loans wouldn’t be forgiven and earlier than curiosity resumed.

Complete Every day Schooling Division Deposits at U.S. Treasury

One other seemingly purpose behind the less-than-dire forecast because the cost pause ends is the energy nonetheless obvious within the well being of the U.S. shopper. A number of coverage modifications by the White Home and Division of Schooling bode properly, too. A big take-up of the brand new SAVE plan would scale back month-to-month funds and waive unpaid curiosity for low-income pupil mortgage debtors, and a one-year “on ramp” for debtors will ignore missed funds for credit score reporting functions. As well as, greater than $127 billion in federal pupil loans throughout over 3.6 million debtors was cancelled or forgiven through the pandemic cost pause. Whereas these components will make the resumption of funds extra easy than in any other case, and reduce the anticipated decline in consumption progress, some pupil mortgage debtors will certainly wrestle managing their debt obligations simply as earlier than the pandemic forbearance. Nonetheless, we anticipate the potential spillover to the broader economic system to be restricted, and we’ll proceed to observe developments within the coming months.

Rajashri Chakrabarti is the pinnacle of Equitable Development Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Daniel Mangrum is a analysis economist in Equitable Development Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Sasha Thomas is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Wilbert van der Klaauw is the financial analysis advisor for Family and Public Coverage Analysis within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Methods to cite this submit:

Raji Chakrabarti, Daniel Mangrum, Sasha Thomas, and Wilbert van der Klaauw, “Borrower Expectations for the Return of Scholar Mortgage Compensation,” Federal Reserve Financial institution of New York Liberty Avenue Economics, October 18, 2023, https://libertystreeteconomics.newyorkfed.org/2023/10/borrower-expectations-for-the-return-of-student-loan-repayment/.

Disclaimer

The views expressed on this submit are these of the creator(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the creator(s).